NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) just delivered one of the most consequential quarters in semiconductor history, and the stock is responding. After a 66.34% one-year run and a fresh post-earnings bid, investors want to know how much room is left.

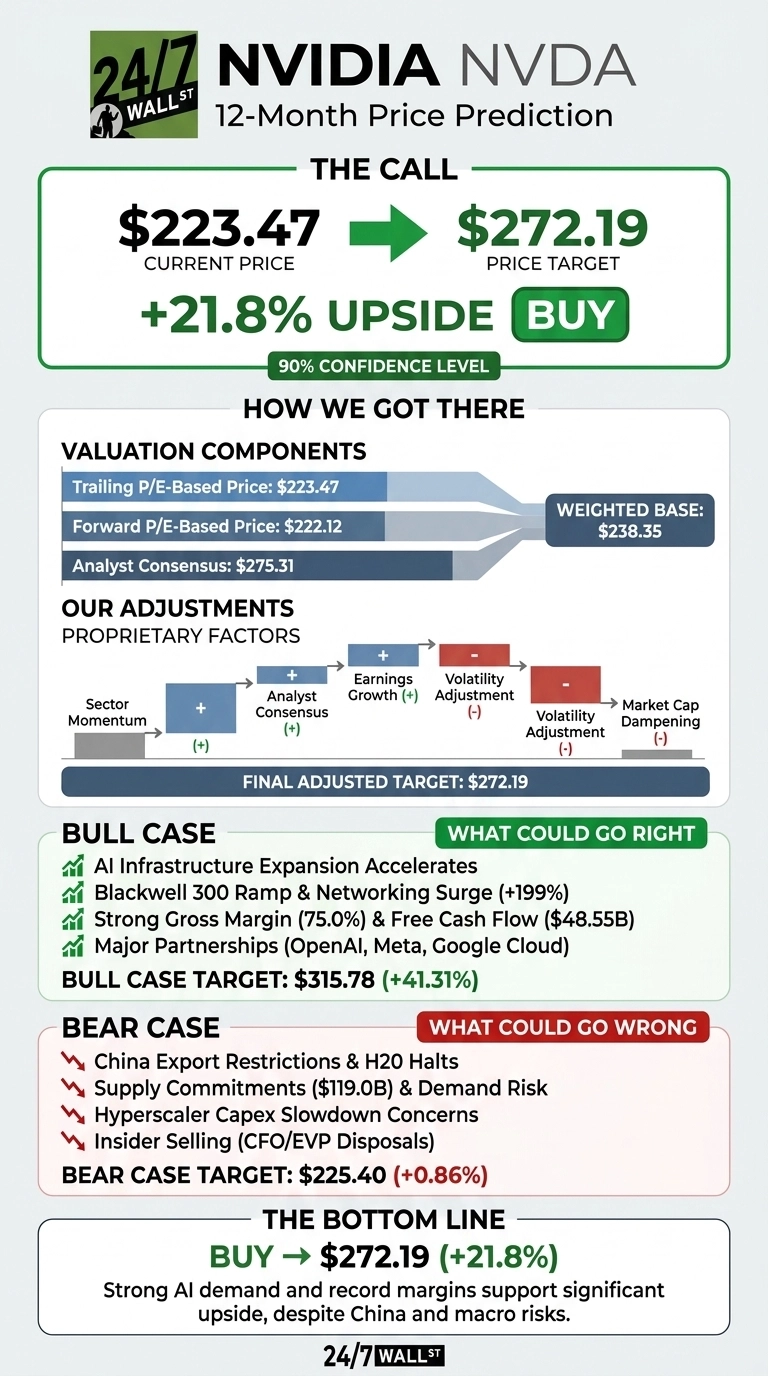

Our 24/7 Wall St. price target for NVIDIA is $272.19, implying 21.8% upside from $223.47. We rate the shares a buy with 90% confidence, the highest tier in our framework.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $223.47 |

| 24/7 Wall St. Price Target | $272.19 |

| Upside | 21.8% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Blowout Quarter Resets the Story

NVIDIA closed at $223.47 on May 20, up 10.6% over the past month and 19.83% year to date. The stock sits roughly 16% below its 52-week high of $236.54 and well off the $129.13 low.

The Q1 FY27 report on May 20, 2026 was the catalyst. Revenue hit $81.615 billion, up 85.23% year over year and beating estimates by 3.16%. Non-GAAP EPS of $1.87 topped the $1.7738 consensus.

Data Center revenue reached $75.246 billion (+92% YoY), networking exploded 199%, and management guided Q2 to $91 billion. The board also approved a new $80 billion buyback and raised the dividend to $0.25 per share.

The Case for $315 and Higher

Bulls see this as the early innings of what Jensen Huang calls “the largest infrastructure expansion in human history.” Blackwell 300 is ramping, the Vera Rubin platform was unveiled, and partnerships with OpenAI (10GW), Anthropic (1GW), Meta, and Google Cloud lock in multi-year demand. Networking grew 199%, gross margin sits at 75%, and free cash flow hit $48.554 billion in a single quarter.

Our bull case scenario sees NVDA reaching $315.78 over twelve months, a 41.31% return. With 48 Buy and 10 Strong Buy ratings against just 2 Holds and 1 Sell, Wall Street agrees. Analysts updated their price target following the strong results.

Benchmark analyst Cody Acree raised the firm’s price target on Nvidia to $335 from $250 and keeps a Buy rating on the shares. Further, Evercore ISI analyst Mark Lipacis raised the firm’s price target on Nvidia to $413 from $352 and keeps an Outperform rating on the shares following the company’s earnings report.

JPMorgan analyst Harlan Sur raised the firm’s price target on Nvidia to $280 from $265 and keeps an Overweight rating on the shares.

The Risks Worth Watching

China remains the elephant in the room. Q2 guidance assumes zero Data Center compute revenue from China, and the H20 ban already triggered a $4.5 billion write-down last year. Supply commitments of $119 billion create real demand risk if hyperscaler capex slows. Retail chatter has flagged a 30% drop in B200 rental prices and rising rate-hike odds as warning signs.

Insider activity skews toward selling, with CFO Colette Kress and EVP Ajay Puri disposing of large blocks in March around the $172 to $183 range. That said, the bulk of those sales reflect routine 10b5-1 plans rather than fundamental concern, and the company is offsetting any dilution through its $80 billion repurchase. Our bear case still gets to $225.40, essentially flat. The downside math is contained.

Our Take

The 24/7 Wall St. price target of $272.19 reflects a buy at 90% confidence. The scale-tipping factor is the combination of 85% revenue growth, 75% gross margin, and 27x forward earnings, a reasonable multiple for this growth profile.

The thesis strengthens if hyperscaler capex commentary stays firm through Q2. It weakens if China restrictions widen to Blackwell or if Vera Rubin slips materially.

NVIDIA Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $272.19 |

| 2027 | $276.09 |

| 2028 | $308.49 |

| 2029 | $335.15 |

| 2030 | $375.62 |

These projections assume NVIDIA executes on the Blackwell-to-Rubin product cadence and hyperscaler AI capex continues compounding. Significant upside could come from China re-opening or sovereign AI scaling faster than modeled. Downside risk is concentrated in customer concentration and a potential AI capex digestion year.

Contact [email protected] for any questions or corrections.