NVIDIA (NASDAQ: NVDA | NVDA Price Prediction) has produced one of the most extraordinary wealth-creation runs in stock market history. Ten years ago, it was a respected gaming chip company. Today it is the backbone of global AI infrastructure, and the numbers reflect that transformation in a way that is almost hard to process.

From Gaming GPUs to the Engine of AI

In early 2016, NVIDIA was known primarily for graphics cards powering video games and workstations. The AI revolution was nascent. Then researchers discovered that NVIDIA’s GPU architecture was uniquely suited for the parallel processing demands of machine learning, and everything changed.

CEO Jensen Huang bet the company’s roadmap on accelerated computing, building the CUDA software ecosystem that now creates enormous switching costs for AI developers. By 2023, the H100 chip had become the most coveted piece of hardware in the world. The Blackwell architecture followed, and in Q3 FY2026, Huang described demand plainly: “Blackwell sales are off the charts, and cloud GPUs are sold out.”

Data Center revenue hit $51.2 billion in Q3 FY2026, up 66% year-over-year, representing 90% of total company revenue. This is not a gaming company anymore.

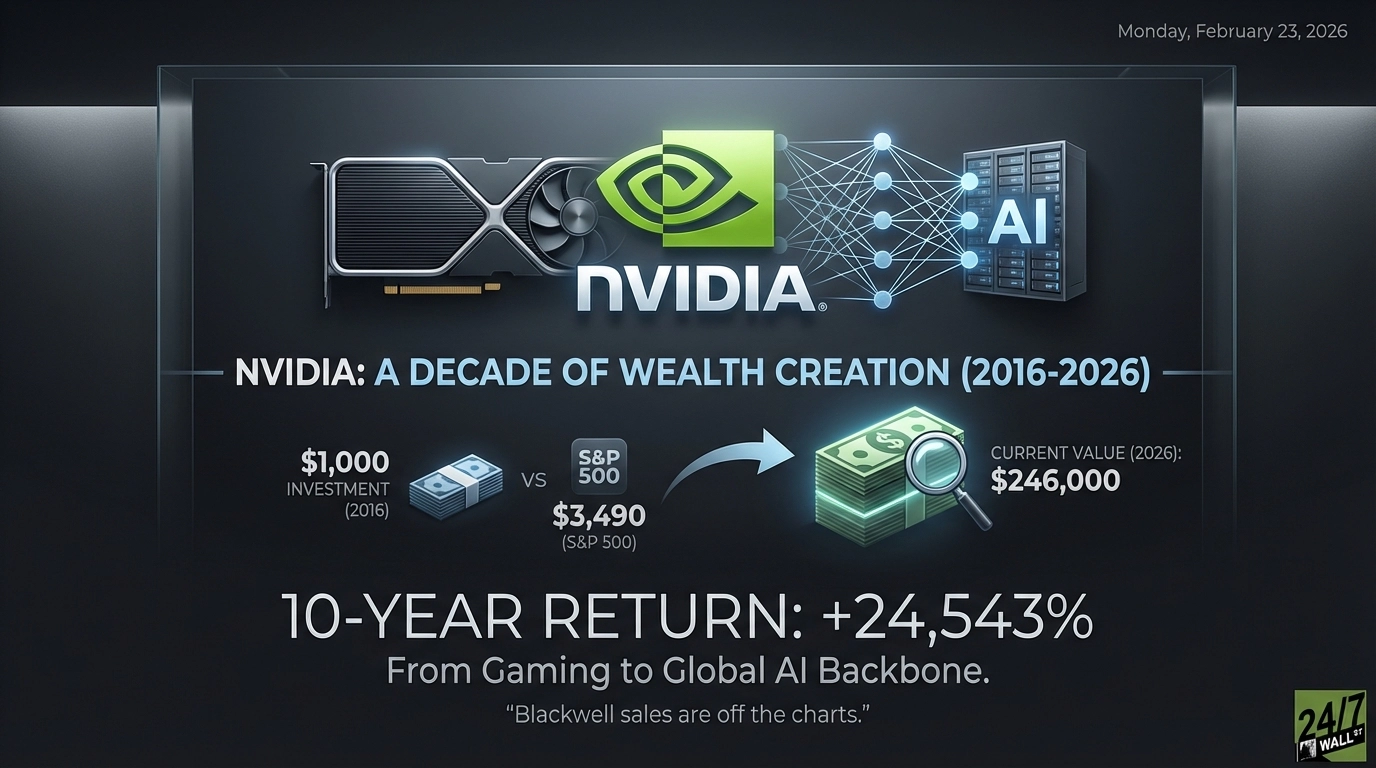

$246,000 From a $1,000 Bet Made in 2016

- 1-Year Return (Feb 2025 to Feb 2026)

- Initial Investment: $1,000

- Current Value: $1,417

- Total Return: +41.7%

- S&P 500 (same period): $1,135 (+13.5%)

- 5-Year Return (Feb 2021 to Feb 2026)

- Initial Investment: $1,000

- Current Value: $13,172

- Total Return: +1,217%

- Annualized Return: ~67%

- S&P 500 (same period): $1,738 (+73.8%)

- 10-Year Return (Feb 2016 to Feb 2026)

- Initial Investment: $1,000

- Current Value: $246,429

- Total Return: +24,543%

- Annualized Return: ~73%

- S&P 500 (same period): $3,490 (+249%)

The 10-year figure is not a typo. A $1,000 position in early 2016 would be worth roughly $246,000 today, compounding at approximately 73% annually. The S&P 500 returned 249% over the same decade, turning $1,000 into about $3,490. NVIDIA beat that by a factor of roughly 70. Holding through it required real conviction: the stock dropped more than 60% in 2018 and again in 2022, and early 2025 saw a sharp pullback to around $104 before recovering. Timing mattered less than staying put.

Cautiously Bullish, With Eyes Open

The fundamentals support a constructive view. Q4 FY2026 guidance calls for $65 billion in revenue, and 94% of analysts carry a buy rating with a consensus target of $253.88. The CUDA moat is real, and hyperscalers are still racing to build capacity.

The risks are real too. Export restrictions have already shut out China, with H20 sales described as insignificant in Q3. Custom silicon from Google, Amazon, and others is advancing. At a trailing P/E near 47, there is little margin for error if growth decelerates.

NVIDIA remains the most defensible position in AI infrastructure for now, but the 246x decade is almost certainly behind it. The next chapter will be measured in doubles, not multiples of hundreds.

Contact [email protected] for any questions or corrections.