At $152.17, Palantir (NASDAQ:PLTR | PLTR Price Prediction) looks priced for perfection, even after posting what may be the strongest quarter in enterprise software history. The data analytics firm shattered its Rule of 40 with a score of 145 and grew Q1 2026 revenue 85% year-over-year, yet the stock is down year-to-date while the S&P 500 climbs.

Palantir builds Gotham, Foundry, and AIP, platforms the U.S. military, intelligence community, and commercial customers use to embed AI into operations. It sits at the intersection of two themes investors prize: AI-native enterprise software and U.S. defense modernization. Shares touched $207.52 over the past year before sliding to current levels.

The Bull Case: An n-of-One AI Compounder

Q1 2026 delivered $1.633 billion in revenue, U.S. commercial revenue of $595 million growing 133%, and adjusted free cash flow of $925 million at a 57% margin. Management raised FY 2026 revenue guidance to a $7.656 billion midpoint, a 71% growth rate and the largest raise in company history.

Net dollar retention hit 150%, total customer count grew 31%, and remaining deal value reached $11.8 billion. CEO Alex Karp said the biggest problem is that the company “just cannot meet demand”. At a 60% adjusted operating margin and 11 consecutive quarters of accelerating growth, bulls argue the multiple follows the math.

The Bear Case: A Multiple That Leaves Zero Room for Error

Forward P/E sits near 110, trailing P/E near 183, price/sales near 74, and price/book near 46. Free cash flow yield is just 0.60%. Even meeting the raised $7.65 billion guide prices in flawless execution for years.

Insiders are not buying. In May, Karp, Cohen, and Sankar each disposed of hundreds of thousands of Class A shares in the $132.95 to $136.61 range, with no voluntary purchases near $152. Director Alexander Moore has steadily sold at progressively lower prices since March. Stock-based compensation ran $684 million for FY 2025, and contracts remain subject to termination for convenience. One slipped government deal or a normalized commercial quarter could trigger sharp compression.

The Hold Case: Great Company, Difficult Price

Fundamentals are pristine: 88% adjusted gross margin, $8 billion in cash and treasuries, near-zero debt. Shorting a business with 150% net retention and triple-digit U.S. growth is risky.

Yet buying at 110x forward earnings after a year-to-date drop is not obviously right. Patient investors might wait for U.S. commercial to confirm the 120% guide for another quarter while watching whether shares reset toward the 200-day moving average near $161.67.

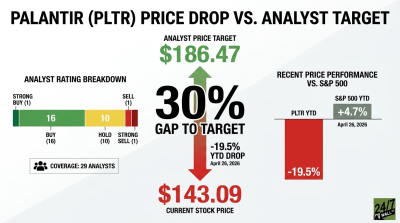

What the Data Says About $152

Palantir trades at $152.17 against an analyst average price target of $183.73, implying roughly 21% upside across 31 covering analysts:

- Strong Buy: 1

- Buy: 18

- Hold: 10

- Sell: 1

- Strong Sell: 1

Year-to-date, PLTR is down 14.39% while the S&P 500 is up 11.39%. Over one year, PLTR returned 15.25% versus 28.15% for the index.

The Takeaway: Why $152 Pays for Perfection

At $152.17, Palantir is priced for flawless execution. The numbers are extraordinary, but the multiple assumes they continue indefinitely. Meeting raised guidance produces modest upside; any slip produces sharp downside. Year-to-date performance shows the market quietly de-rating a name that beat on every line.

Watch U.S. commercial growth, the SBC trajectory, and Q2 revenue against the $1.797 billion to $1.801 billion guide. A miss or government delay could send shares toward the 50-day moving average near $141.89 or lower, toward the $132 cluster Polymarket traders are pricing for June.

Insider behavior reinforces the valuation concern. Senior leadership sold heavily in the $133 to $137 range without a single voluntary purchase near current levels. When senior leadership is selling rather than buying at current levels, it is a signal worth weighing.

The thesis breaks if U.S. commercial reaccelerates to 150%+ and FCF margin holds above 55% through year-end. Until then, Palantir is the best business in software priced for the worst possible entry.

Contact [email protected] for any questions or corrections.