At $133, Palantir (NASDAQ:PLTR | PLTR Price Prediction) is starting to look juicy to many analysts. This is especially true paired with social-media chatter about presidential interest and analyst consensus pointing higher. The stock has been a 2026 battlefield, caught between extraordinary business momentum and a valuation that asks you to underwrite years of flawless execution.

Palantir sells Gotham to spies and soldiers, Foundry to large enterprises, and AIP to anyone bolting generative AI onto messy operational data. It is the rare software vendor that grew up inside the intelligence community and then convinced Fortune 500 boards that the same plumbing works for refineries, hospitals, and insurers. The Trump angle, whether from Truth Social commentary or assumptions that a second Trump administration favors politically aligned defense software, has been a recurring tailwind.

Why the bull case still has teeth

The fundamentals are something even the bears don’t take on. You are looking at the company’s “Rule of 40” soaring to 145%, which Palantir’s CEO Alex Karp says it “shattered”. The company simply keeps performing better and better each quarter, continuously staying ahead of analyst estimates.

In Q1, revenue grew 85% year-over-year and 16% quarter-over-quarter. Most companies fail to touch that quarterly growth in two years.

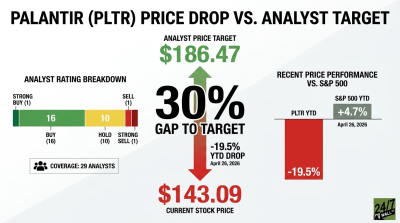

Wall Street has not blinked. The consensus 12-month price target sits at $188, with 13 Buy vs 6 Hold + Sell ratings. AIP is the asset bulls keep pointing to, a deployment engine that has shortened sales cycles inside U.S. commercial and turned customer expansion into a flywheel.

Why the bears think this ends badly

Start with the multiple. Palantir trades at a P/E of 150x and a price-to-sales ratio of 66x. Even on forward earnings, you are paying 95 times. Software comps trade at a fraction of that. Any deceleration, any government contract slip, any AIP cohort underperformance, and the multiple compresses violently.

The insider activity is uglier than the bull narrative admits. Co-founder Peter Thiel disposed of more than 2 million shares in early March at prices between roughly $141 and $147, and Director Alexander Moore sold into both March and April rallies. Stock-based compensation ran $684 million for 2025, a meaningful drag on real per-share economics.

Why patience is the honest answer

The business is too strong to short with conviction and the valuation too rich to chase with conviction. A Hold is what falls out when both sides are loaded with live ammunition.

A pullback toward the 52-week low near $119 alongside a confirmed Q2 beat would make this a credible Buy. A guidance cut, a major commercial logo slip, or evidence that AIP land-and-expand math is softening would push it toward Sell. Track quarterly U.S. commercial growth and remaining deal value. Those two numbers tell you whether the flywheel is real.

What the current price action actually says

Shares are down over 20% since the start of this year, while the S&P 500 is up 8.2%. In fact, PLTR stock is up just 6% in the past year. This is embarrassing as some of the most well-known hardware AI stocks have outperformed it by 10x or more.

The consensus target of $188 implies meaningful upside, though analyst targets are a survey of opinion rather than a forecast. Crowd-sourced prediction markets cluster the May close in the $126 to $144 range, with composite sentiment at 64.08, bullish with medium confidence.

The verdict on Palantir at $133

At $133, Palantir is a Hold. You have a genuinely exceptional business priced like one. The growth is real, the cash flow is real, the AIP narrative is real. The problem is that almost none of the bear scenarios are priced in.

PLTR’s valuation does not leave room for a quarter where U.S. commercial growth decelerates from triple digits to double digits, even though that is mathematically inevitable.

Watch Q2 2026 results. A clean beat plus a raise, with the stock near current levels, changes the math. A miss or any softening in U.S. commercial remaining deal value validates Thiel trimming.

If 2026 prints in line with the company’s own guide, this stock probably reasserts itself. At 66 times sales any disappointment travels at the speed of forced selling. Owning a great business at a punishing price is a coin flip dressed as conviction, and that is exactly the trade Hold lets you avoid.

Contact [email protected] for any questions or corrections.