Microsoft (NASDAQ:MSFT | MSFT Price Prediction) offers a rare combination of irreplaceable enterprise software and contracted cloud and AI demand, because its dual engine of irreplaceable enterprise software and a contracted cloud and AI backlog of $627 billion gives it the kind of revenue visibility almost no other company on Earth can match.

For a retirement investor who has been whipsawed by trend chasing, Microsoft is the rare position that asks almost nothing of you. No daily monitoring. No thesis to defend at every earnings release. Just ownership of a business whose products sit inside the operating workflow of nearly every large company on the planet.

Pillar 1: Durability That Approaches Utility Status

Windows and Office commercial products function as corporate utilities. Companies do not casually swap them out. That stickiness shows up in the numbers: Productivity and Business Processes generated $35.013 billion last quarter, up 17%, while Intelligent Cloud delivered $34.681 billion at 30% growth, with Azure up 40%. The legacy franchise pays the bills at 68.82% gross margins. The high-growth engine compounds on top. Add a fortress balance sheet (debt-to-equity of 0.176 and interest coverage of 53.89x) and you have a business built to outlast any single CEO, product cycle, or recession.

Pillar 2: Quiet Income and Relentless Compounding

The headline 0.76% dividend yield understates the picture. Microsoft has raised its quarterly payout almost every year, from $0.08 in 2005 to $0.91 today, and returned $12.7 billion to shareholders in a single quarter through dividends and buybacks. Return on equity sits at 33.28%, meaning every retained dollar is being reinvested at an exceptional rate. Free cash flow of $71.61 billion in FY25 funds the dividend, the buyback, and the AI buildout at the same time.

Pillar 3: Survives Cycles Because Customers Cannot Leave

Microsoft has already navigated the dot-com bust, 2008, and 2020. The reason is structural: $54.5 billion in quarterly Microsoft Cloud revenue is recurring, subscription-based, and tied to mission-critical workloads. The $627 billion contracted backlog gives multi-year visibility independent of macro mood. Over the past decade, the stock has returned 833.28% on a split-adjusted basis. CEO Satya Nadella’s commentary on the latest quarter was direct: “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.”

The Scenario Where It Underperforms

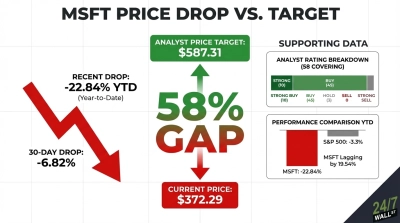

If AI returns disappoint and tech sentiment unwinds, the stock can lag. Capital expenditures hit $30.876 billion last quarter, up 84.39% year over year, and the stock is down 11.24% year to date. A P/E of 31 leaves room for multiple compression. None of that breaks the forever thesis. Office and Windows revenue keeps arriving regardless of AI ROI debates, the dividend keeps rising, and any pullback simply lets the buyback retire shares more cheaply. For a 25-year horizon, a soft year is a feature.

For long-horizon holders, the structural case rests on recurring cloud revenue, a rising dividend, and buybacks that compound through cycles.