Almost six months ago, our December 2025 piece Analysts See Triple-Digit Revenue Growth in 2026 for These 3 AI Infrastructure Stocks argued that three names sat in the sweet spot of the AI buildout: Nebius (NASDAQ: NBIS | NBIS Price Prediction) with an annual recurring revenue (ARR) ramp implying up to roughly 1,600% growth, IREN (NASDAQ: IREN) targeting over 500% growth, and CoreWeave (NASDAQ: CRWV) with up to 138% growth. The thesis was that hyperscaler graphics processing unit (GPU) demand was outrunning supply, and these three would convert contracted power into booked revenue faster than their peers.

The mid-year report card shows mixed results. One name blew past the bar, one cleared the growth target despite widening losses, and one missed the headline number while quietly rebuilding the business. We graded each on stock performance and whether the company is executing toward the revenue and ARR run-rate that justified the call.

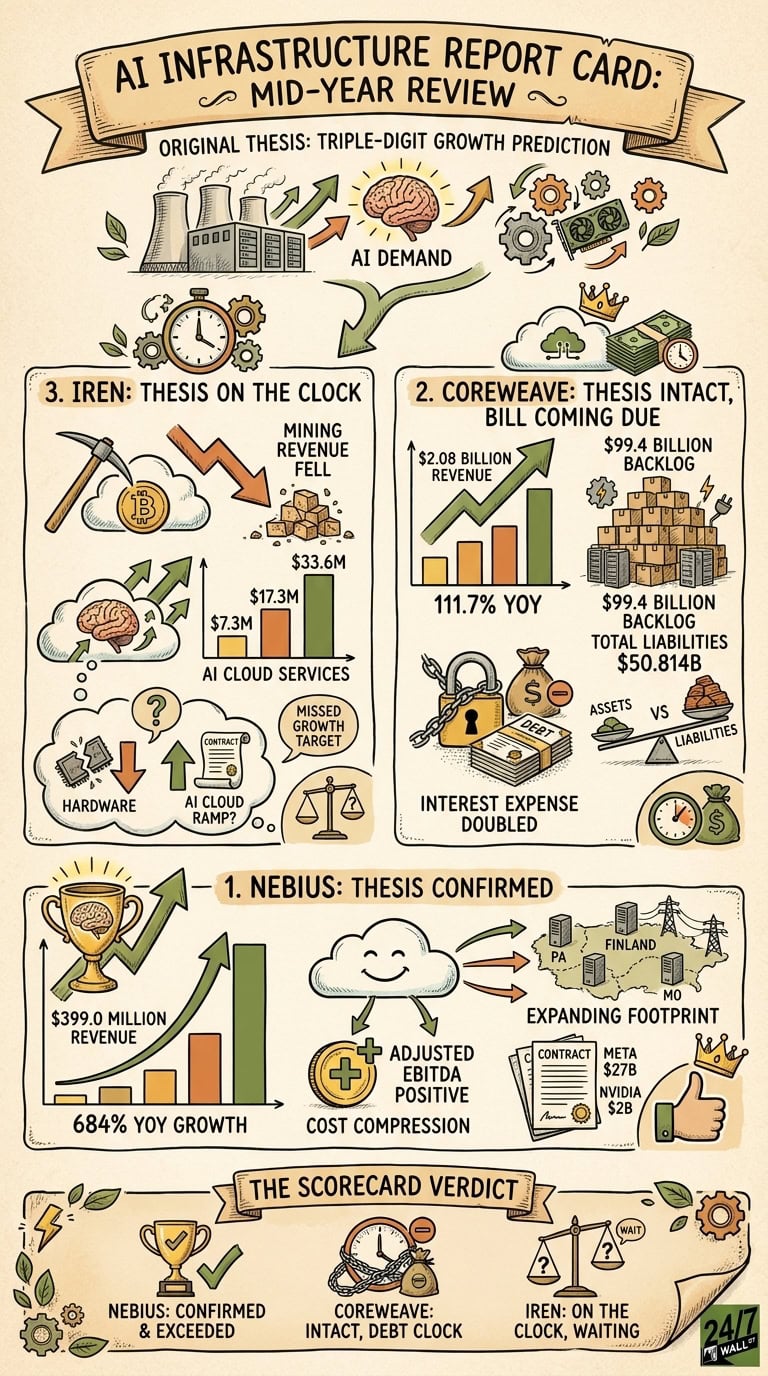

3. IREN: Thesis on the Clock

Data center operator IREN is the most uncomfortable name on the scorecard. Q3 FY2026 revenue came in at $144.80 million, a 2.2% year-over-year decline that missed consensus estimates. The triple-digit growth claim did not hold.

Bitcoin mining revenue fell to $111.20 million as hardware was decommissioned, while AI Cloud Services climbed from $7.30 million to $17.30 million to $33.60 million across three quarters. Management anchors its outlook to a $3.70 billion annualized run-rate by year-end 2026, backed by a $3.40 billion five-year Nvidia AI Cloud contract and a $9.70 billion Microsoft partnership.

Shares trade at $54.02, up 43.0% year to date but down 18.9% in the past week. The 247Factor model flags a base-case target of $113.72 with 110.52% upside, though the 4.23 beta reflects volatility. The execution question is whether AI Cloud revenue can offset the mining cliff fast enough to validate that ARR target.

2. CoreWeave: Thesis Intact, Bill Coming Due

Cloud computing company CoreWeave delivered on the growth promise. Q1 2026 revenue hit $2.08 billion, up 111.7% year over year and 5.8% above the $1.96 billion consensus. Revenue backlog reached $99.4 billion, including a $21 billion Meta commitment, and active power surpassed 1 GW with a path to more than 8 GW by 2030.

Net loss widened to $740 million, interest expense doubled to $536 million, and capex hit $7.695 billion in a single quarter. Total liabilities reached $50.814 billion, against $55.573 billion in assets. Forward EPS came in at −$1.40, so traditional P/E math does not apply.

The stock reflects ambivalence: trading at $98.45, up 37.5% year to date but down 39.3% over the past year. Nearly two-thirds of surveyed analysts recommend buying shares, and they have a $140.18 mean target price. CEO Michael Intrator called it “the strongest bookings quarter in CoreWeave’s history.” The key question is whether operating leverage can outpace interest expense before the next refinancing window.

1. Nebius: Thesis Confirmed

Amsterdam-based Nebius is the clear winner. Q1 2026 revenue reached $399.0 million, up 684% year over year, with the AI Cloud segment producing $389.7 million at 841% year-over-year growth. EPS came in at $2.11, and adjusted EBITDA flipped positive to $129.5 million. Cost of revenue compressed from 49% to 26%.

Management reaffirmed FY2026 revenue guidance of $3.0 billion to $3.4 billion, an ARR target of $7.0 billion to $9.0 billion, and more than 4 GW contracted power by year-end. Remaining performance obligations stand at $33.59 billion, anchored by a $27 billion five-year Meta agreement and a $2 billion Nvidia pre-funded warrant investment.

Shares trade at $220.12, up 163.0% year to date and 318.6% over one year, even after a 15.5% one-week pullback. The 247Factor model carries a $280.62 base-case target with 27.48% upside and 0.9 confidence. CEO Arkady Volozh said: “Our capacity footprint is expanding rapidly, our full-stack cloud platform is world-class from the infrastructure layer all the way up to our inference and agentic capabilities.” The execution question is narrower: can the Pennsylvania, Finland, and Missouri sites energize on schedule to feed the Meta and Microsoft ramps?

The Scorecard Verdict

The original premise required triple-digit revenue growth backed by credible run-rate progress. Nebius cleared both bars, with margin expansion as a bonus. CoreWeave delivered the growth and a $99.4 billion backlog, but the funding stack is the active risk. IREN missed the headline number because mining is being deliberately torn down, leaving the AI Cloud ramp to prove itself by year-end. One thesis is confirmed, one is intact but on a debt clock, and one still needs the second-half earnings report to justify the call.

Contact [email protected] for any questions or corrections.