American Water Works (NYSE:AWK | AWK Price Prediction) just raised its quarterly dividend by 8% to $0.895 per share, the latest step in a decade of uninterrupted increases at the country’s largest publicly traded regulated water utility. Income investors hold AWK for one reason: a payout backed by water bills that customers across 14 states have to pay no matter what the economy does. With the stock down 8% over the past year and a giant merger with Essential Utilities pending, the question is whether AWK’s dividend trajectory is as durable as the pipes it owns. The short answer, after working through the numbers, is yes.

How the dividend gets funded

AWK is a pure-play regulated water and wastewater utility serving residential, commercial, and military customers. Earnings come from a rate base of physical infrastructure (pipes, treatment plants, meters) on which state regulators allow a return. Every dollar of approved capital spending becomes future revenue once rate cases close. That model is what makes dividends here different from, say, an industrial cyclical: the cash flow underwriting the payout is set by regulatory order.

The company is currently working five general rate cases requesting $518 million in annualized revenue, with new rates in Pennsylvania and New Jersey expected to take effect in the second half of 2026. That is the engine behind management’s affirmed 7% to 9% long-term EPS and dividend growth targets.

What the coverage numbers actually say

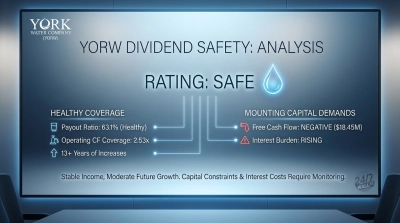

Management guides to $6.02 to $6.12 in adjusted EPS for 2026 against an annualized dividend run rate near $3.58. That works out to a payout ratio in the high 50% range, which leaves real cushion. For a regulated utility, that is a healthy zone: enough to fund growing dividends, not so high that a single bad rate case threatens the payout.

Cash flow tells the same story from a different angle. AWK paid $633 million in dividends in 2025 against $2.059 billion in operating cash flow, meaning roughly 31% of operating cash went to shareholders. The catch is capital intensity. CapEx ran $3.126 billion in 2025, well above operating cash flow, so AWK funds the gap with debt and equity. That is normal for a regulated water utility, but it means dividend safety hinges on continued capital markets access and supportive rate orders, not on self-funded free cash flow.

Balance sheet and rate trajectory

Debt-to-capital sat at 58% at the end of Q1 2026, and AWK issued $700 million of 5.200% senior notes in April. That issuance went off when the 10-year Treasury was near 4.31%; the benchmark has since climbed to 4.56%, which raises the cost of the next round of borrowing planned for late 2026. Interest expense rose $12 million year over year in Q1, the single biggest reason net income slipped 4% even as operating income grew 5%. Investment-grade ratings from S&P and Moody’s remain intact.

Total return reality check

A safe dividend does not automatically make a good investment. Shares trade near $126, down 13% over five years on a price basis, as rising rates compressed utility multiples. The yield sits around 2.7%, low for an income vehicle, so treat this as a dividend-growth name rather than an income vehicle. Analysts carry a $136 consensus target.

The verdict

The dividend is safe. Coverage is comfortable, the regulated model converts CapEx into revenue, and the Essential Utilities merger (approved by shareholders February 10, 2026, targeting a Q1 2027 close) expands the rate base further. The real risk is that rising financing costs and PFAS-related capex compress dividend growth toward the low end of the 7% to 9% band. AWK suits investors who want a slowly compounding income stream tied to essential infrastructure, not a high current yield.

Contact [email protected] for any questions or corrections.