Income investors who own American Water Works (NYSE:AWK | AWK Price Prediction) just received a meaningful raise. The board lifted the quarterly dividend about 8% to $0.8950 per share, the latest in an 18-year unbroken streak of quarterly payouts from the largest publicly traded U.S. regulated water utility. With AWK shares down roughly 9% over the past year, the question for current and prospective holders is whether this dividend remains rock solid, or whether the company’s enormous infrastructure build is starting to crowd it out.

How the Cash Actually Gets to Shareholders

AWK is a regulated monopoly. State public utility commissions set the rates customers pay, and those rates are designed to give the company a return on the capital it invests in pipes, treatment plants, and meters. That is the income engine. When AWK invests more in infrastructure and wins constructive rate cases, allowed revenues rise, earnings grow, and the dividend follows.

The mechanics show up clearly in the numbers. AWK delivered full-year 2025 adjusted EPS of $5.64, up from $5.18 in 2024, on revenue of $5.14 billion. Management has reaffirmed 2026 adjusted EPS guidance of $6.02 to $6.12 and a long-term 7% to 9% growth target for both EPS and the dividend through 2030 and beyond.

The Coverage Picture

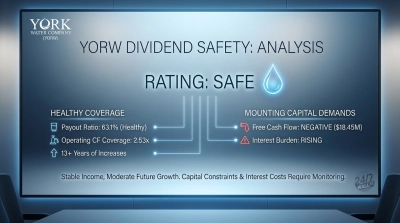

Against the midpoint of guidance, the annualized $3.58 dividend lands in the high-50s as a payout ratio. For a regulated utility, that leaves real cushion: earnings can dip modestly without threatening the payout, and there is headroom to keep raising it at the targeted pace.

Operating cash flow tells the same story. AWK generated $2.06 billion in operating cash flow in 2025 against $633 million in dividends paid, coverage of roughly 3x. That is the comforting number.

The Number That Should Get Your Attention

Free cash flow is negative, and has been for years. 2025 capital expenditures hit $3.13 billion, well above operating cash flow. Every recent year shows the same pattern. This is normal for a capital-intensive water utility, but it means the dividend is effectively funded by external capital alongside operations.

The buildout ahead is even larger. AWK plans $19 billion to $20 billion in capital investment from 2026 to 2030, with roughly $12.5 billion of debt and $2.5 billion of equity issuance in the financing mix. The company just issued $700 million of 5.2% senior notes due 2036, and interest expense rose $12 million year-over-year in Q1 2026. Rising rate-base growth has to outrun rising financing and depreciation costs, which is the central tension for income investors.

Regulatory Tailwinds Holding Up

So far, rate cases are landing constructively. AWK has 5 jurisdictions in active rate cases requesting $518 million in annualized revenue, and CFO David Bowler noted that S&P and Moody’s "note our trend of credit supportive regulatory outcomes". The pending all-stock merger with Essential Utilities, expected to close in Q1 2027, adds scale but also regulatory execution risk across seven required state approvals.

Total Return Reality Check

At about $124, AWK yields about 2.7% and trades at 22x trailing earnings. The stock is down roughly 14% over five years, so the income has not bailed out total returns. Investors are paying for predictability, not capital appreciation.

The Verdict

The dividend is safe. Cash coverage is comfortable, the payout ratio leaves breathing room, regulators continue to authorize rate hikes, and CEO John Griffith committed plainly: "Our Board and management team highly value our dividend." Strong total returns are a different question. AWK works for investors who want a reliably growing income stream from a defensive business and can tolerate a stock that has lagged. Investors chasing yield or expecting price appreciation alongside the income will likely find a poor fit here.

Contact [email protected] for any questions or corrections.