York Water (Nasdaq: YORW) declared a quarterly dividend of $0.228 per share in November 2025, marking a 4.0% increase from the prior year and extending a payment streak that stretches back over a decade. The annual dividend now stands at $0.89 per share, yielding 2.63%. For income investors evaluating this 209-year-old regulated water utility, the central question is whether the dividend can withstand mounting capital demands and rising debt service costs.

| Metric | Value |

|---|---|

| Annual Dividend | $0.89 per share |

| Dividend Yield | 2.63% |

| Consecutive Years of Increases | 13+ years |

| Most Recent Increase | 4.0% (November 2025) |

| 5-Year Dividend CAGR | 4.2% |

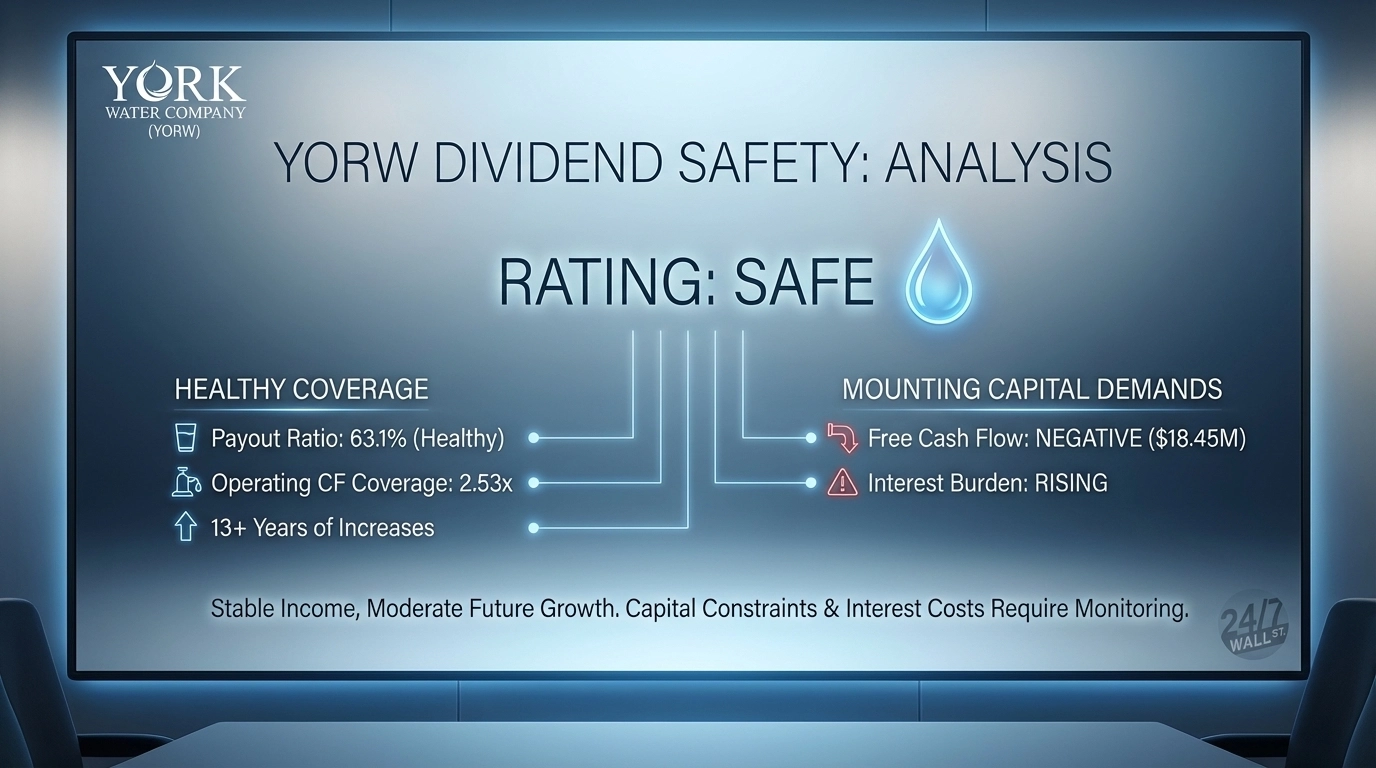

Payout Ratios Show Comfortable Coverage

York Water paid $12.09 million in dividends during 2024 against net income of $20.33 million, producing an earnings payout ratio of 59.5%. Based on trailing twelve-month EPS of $1.39, the current payout ratio sits at 63.1%. Both figures remain well below the 70% threshold that typically signals stress.

Operating cash flow generated $30.56 million during 2024 while paying $12.09 million in dividends, delivering 2.53x coverage. This coverage ratio has remained stable between 2.0x and 2.8x over the past five years.

| Metric | TTM/2024 Value | Assessment |

|---|---|---|

| Earnings Payout Ratio | 63.1% | Healthy |

| Operating CF Coverage | 2.53x | Strong |

| Free Cash Flow | ($18.45M) | Negative |

The complication surfaces when examining free cash flow. Capital expenditures totaled $49.01 million in 2024, far exceeding operating cash flow and producing negative free cash flow of $18.45 million. This gap has persisted for years as the company invests heavily in infrastructure replacement and expansion.

Debt Load Requires Monitoring

York Water finances its capital program through debt and equity. Total debt reached $227.32 million as of Q3 2025, producing a debt-to-equity ratio of 0.95. Interest expense surged 74% over the past three years, climbing from $5.11 million in 2022 to $8.90 million in 2024.

Interest now consumes 43.8% of operating income, up from 20.9% in 2022. This rising burden reflects both increased borrowing and higher rates. With EBITDA of $42.50 million, net debt-to-EBITDA sits around 5.3x, elevated for a utility but manageable given the regulated business model.

Management Signals Commitment

CEO Joseph Thomas Hand demonstrated confidence through four stock purchases between October and December 2025, acquiring 680 shares at prices ranging from $28.83 to $32.11. On October 16, seven executives participated in coordinated purchases at $28.83, including the COO, CFO, and four vice presidents.

CFO JT Hand attributed recent revenue growth to “growth in the customer base and revenues from the Distribution System Improvement Charge (DSIC).” The DSIC mechanism allows the company to recover infrastructure costs between rate cases, providing protection for capital spending.

Safe for Now, but Growth Will Moderate

Dividend Safety Rating: Safe

Operating cash flow covers the dividend by 2.5x, the payout ratio remains below 65%, and 13 years of consecutive increases demonstrate commitment. The regulated utility model provides predictable revenue and rate-setting protection. This dividend is safe based on current fundamentals.

The concern centers on sustainability of 4% annual growth. Rising interest costs, negative free cash flow, and margin compression from 45.4% in 2020 to 37.4% in 2024 suggest limited room for acceleration. York Water works for stable income prioritizing safety over growth, but capital constraints will likely moderate future raises to the 3% range.

Contact [email protected] for any questions or corrections.