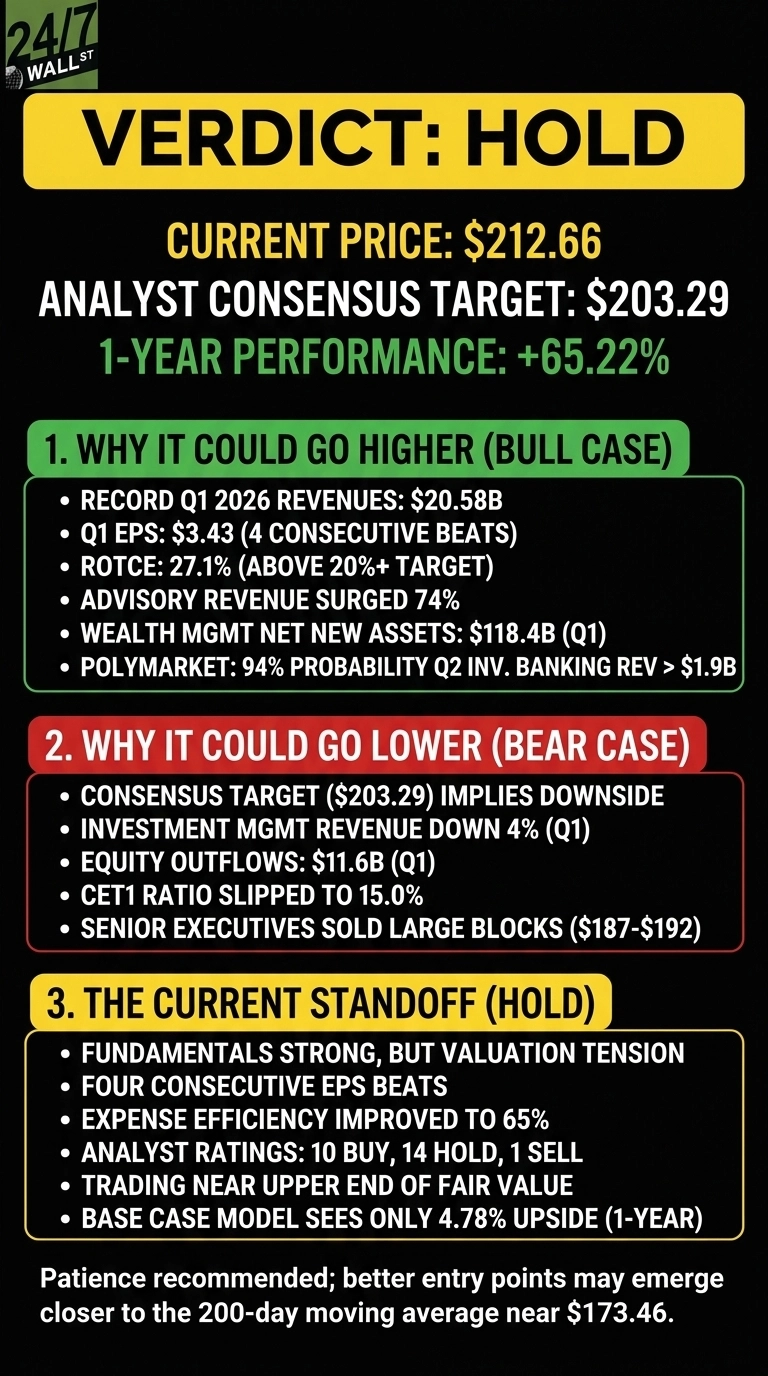

At $212.66, Morgan Stanley (NYSE:MS | MS Price Prediction) is a Hold. The stock sits roughly 7% below its 52-week high of $219.16 after a powerful rally, leaving valuation, sentiment, and forward returns in tension.

Morgan Stanley runs one of the world’s largest integrated investment banks across three engines: Institutional Securities (trading, advisory, underwriting), Wealth Management (anchored by E*TRADE), and Investment Management (Parametric and Eaton Vance). Total client assets across Wealth and Investment Management reached $9.3 trillion at year-end 2025.

Shares are up 65.22% over the past year and 21.08% year to date, propelled by a reopened capital markets cycle and record wealth flows.

Why the Capital Markets Cycle Could Push Shares Higher

In Q1 2026, Morgan Stanley posted record revenues of $20.58 billion, EPS of $3.43, and a ROTCE of 27.1%, well above the firm’s 20%+ target. Advisory revenue surged 74% and equity trading rose 25%.

Wealth Management pulled in $118.4 billion of net new assets in Q1 alone. On forward earnings of $11.82, MS trades near 18x, hardly demanding given 31.9% YoY earnings growth. On Polymarket, traders assign 94% probability of Q2 investment banking revenue exceeding $1.9B.

Why the Risk/Reward Has Already Tilted

The Wall Street consensus target sits at $203.29, implying downside from current levels. Investment Management revenue fell 4% in Q1 with $11.6 billion of equity outflows, and the CET1 ratio slipped to 15% from 15.9%.

Senior executives sold into the rally. Co-Presidents Saperstein and Simkowitz and the Chief Legal Officer disposed of large blocks in April at $187 to $192. Capital markets revenue is cyclical; a soft M&A quarter could compress the multiple quickly. The bear-case 1-year model targets $189.93.

Why Patience Beats Conviction Right Now

Hold reflects a genuine standoff. Fundamentals are firing with four consecutive EPS beats and expense efficiency improving to 65%. Yet the stock has absorbed much of that good news, and analysts remain cautious with 14 Holds against 10 Buys and 1 Sell.

A clean Q2 with sustained M&A momentum and strong wealth inflows could force estimates higher. A capital-markets stumble or credit blowup in commercial real estate would do the opposite.

What the Numbers Reveal

At $212.66, Morgan Stanley trades at a trailing P/E of 19 with a market cap of $328.4 billion. The consensus analyst target of $203.29 implies downside, drawn from 25 analysts split 10 Buy, 14 Hold, 1 Sell.

The performance gap versus the market is striking. MS is up 21.08% YTD against the S&P 500’s 8.19%, and 65.22% over one year versus 22.68% for the index. The dividend yields roughly 1.94%.

Why Hold Is the Right Call at This Price

At $212.66, Morgan Stanley is a Hold. The fundamental story is excellent, but the price reflects it. A 65% one-year gain has pulled MS through the consensus target and into the upper end of fair value, where the model sees only 4.78% upside over the next year.

The trigger for an upgrade to Buy is straightforward: another quarter like Q1 2026, ROTCE holding above 25%, and M&A backlog reaccelerating advisory beyond 74% Q1 growth rate. The trigger for a Sell is a capital-markets air pocket, a credit event in commercial real estate, or wealth net new asset inflows falling below $80 billion per quarter.

Current holders may find the dividend and upcoming earnings reports the key items to monitor. Better risk/reward for new positions would likely emerge closer to the 200-day moving average near $173.46. Owning quality at full price is acceptable; chasing it after a 65% run carries elevated downside risk.

Contact [email protected] for any questions or corrections.