NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) and AMD (NASDAQ:AMD) both reported earnings in May, and the contrast says everything about today’s AI hardware market.

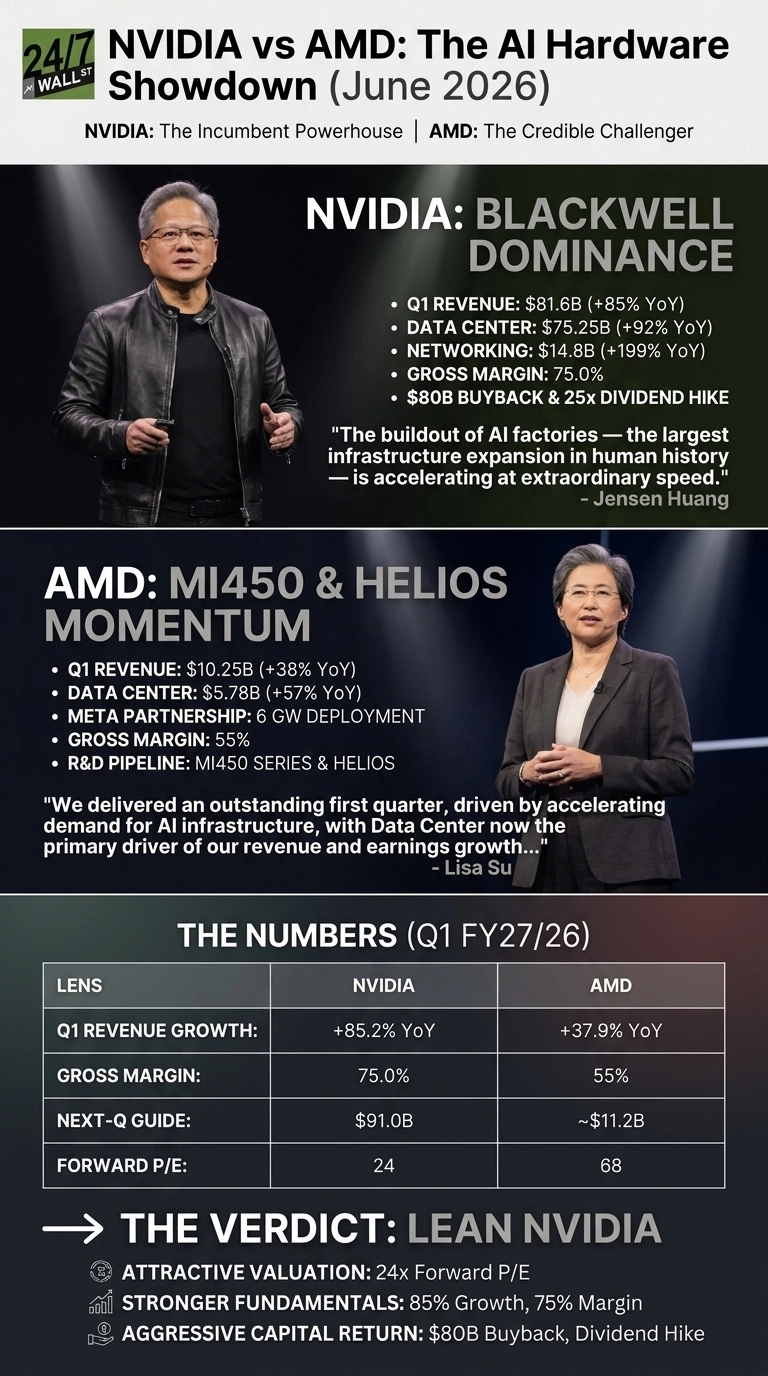

NVIDIA posted a $81.6 billion quarter built on Blackwell dominance. AMD posted $10.25 billion, with the Meta partnership reshaping its data center story. One is the incumbent. The other is the credible challenger finally getting customer commitments at scale.

Blackwell Carries NVIDIA. Meta and MI450 Carry AMD.

NVIDIA’s Data Center segment hit $75.25 billion, up 92% year over year, with networking alone at $14.8 billion (+199%). That networking line is bigger than AMD’s entire data center business. Jensen Huang framed it bluntly: “The buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.”

AMD’s quarter was smaller but accelerating. Data Center revenue reached $5.78 billion (+57%), and Lisa Su told investors “Customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations.”

The 6 GW Meta deployment, starting with a custom MI450 design, gives AMD something it has lacked: a flagship hyperscaler willing to bet on its accelerator roadmap.

One Sells the Whole Factory. The Other Sells the Best Alternative.

NVIDIA’s platform sweep keeps widening. Vera Rubin pairs a custom CPU with Rubin GPUs, Dynamo 1.0 reportedly lifts Blackwell inference up to 7x, and partnerships with Marvell, Corning, Lumentum, and Coherent lock in the optics layer.

AMD’s counter is ROCm maturity, HBM4 collaboration with Samsung for the MI455X, and 6th Gen EPYC (Venice/Verano) with Meta as lead customer. Different shapes of moat.

| Lens | NVIDIA | AMD |

| Q1 Revenue Growth | +85.2% YoY | +37.9% YoY |

| Non-GAAP Gross Margin | 75.0% | 55% |

| Next-Q Guide | $91.0B | ~$11.2B |

| Forward P/E | 24 | 68 |

The valuation gap matters. AMD trades at a trailing P/E of 159 after a 128% YTD run. NVIDIA, despite reporting a $58 billion net income quarter, carries a forward multiple of 24. Cheaper than its smaller rival.

What Decides the Second Half

I will watch three things. First, whether MI450 customer forecasts translate into firm orders that show up in AMD’s Q3 earnings report.

Second, NVIDIA’s China exposure, since Q2 guidance excludes any Data Center compute revenue from China, leaving upside if policy shifts.

Third, supply. NVIDIA already locked in $119 billion of supply commitments, while AMD is still negotiating HBM4 capacity with Samsung.

Why I Lean NVIDIA Heading Into Summer

On a risk-adjusted basis, NVIDIA screens more favorably on the current data. The valuation spread is notable: AMD trades at 68x forward earnings while growing 38%, versus NVIDIA at 24x growing 85% with 75% gross margins, alongside a $80 billion fresh buyback and a 25x dividend hike.

NVIDIA shares have also cooled, down 8.2% since the May 20 report, while AMD rose 37.5%. The AMD case rests on Helios reshaping the competitive map; the NVIDIA case rests on scale, cash generation, and a cleaner near-term setup.

Contact [email protected] for any questions or corrections.