Passive income is the closest thing investors get to a paycheck that arrives whether the market is open, closed, or in freefall. Wages depend on showing up. Rental income depends on tenants paying.

Dividends from a blue-chip beverage company that has raised its payout every year since the Reagan administration depend on roughly eight billion people continuing to drink Coke products, which is about as durable a thesis as exists in public markets.

That durability is exactly why income investors keep coming back to Coca-Cola (NYSE:KO | KO Price Prediction). It offers something a mortgage REIT or a leveraged BDC structurally cannot: a payout that has gone up for 63 consecutive years, backed by one of the most diversified brand portfolios on Earth. For investors building a quarterly cash-flow stream they can actually rely on, that consistency is the entire point.

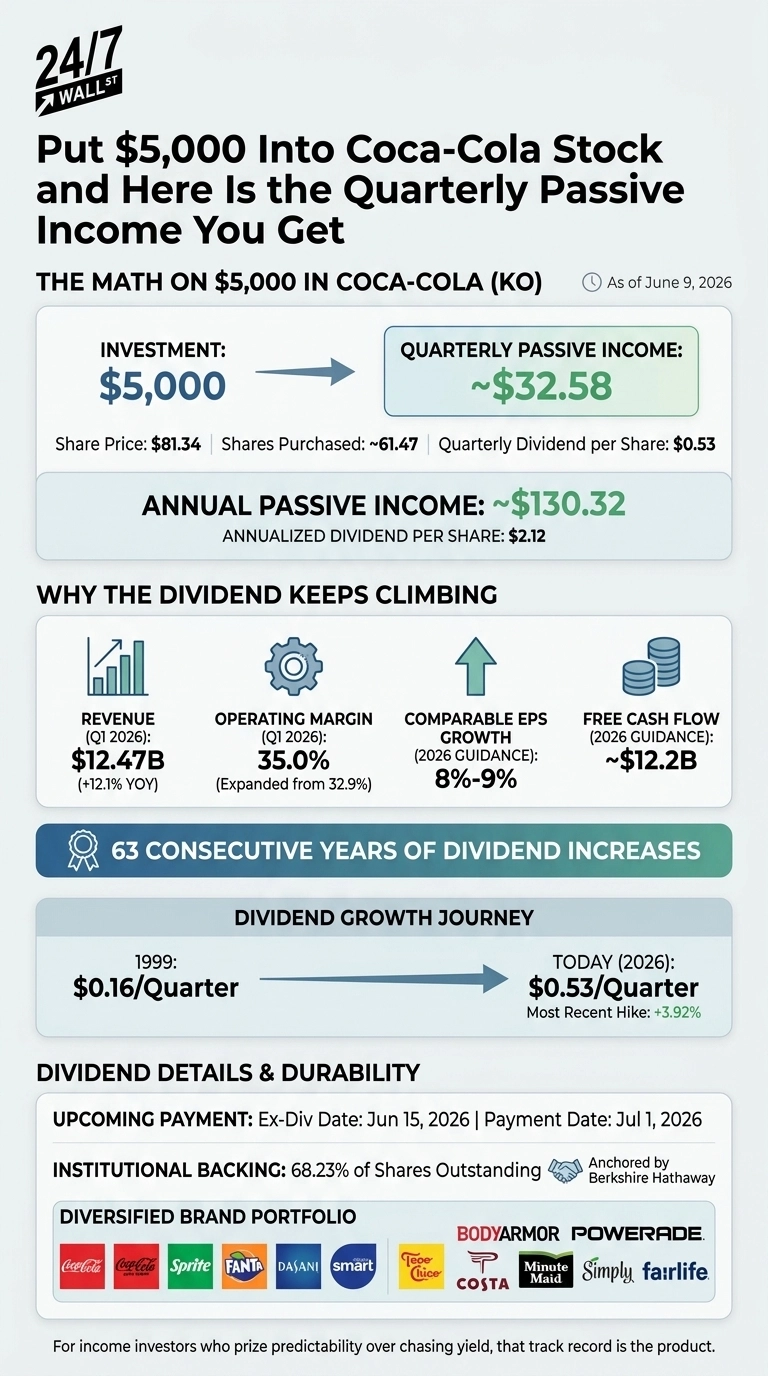

The Math on $5,000 in Coca-Cola

Coca-Cola closed at $81.34 on June 9, 2026, after rising 17.15% year to date and 16.64% over the trailing year. The company most recently declared a $0.53 quarterly dividend, with an ex-dividend date of June 15, 2026 and a payment date of July 1, 2026. That works out to $2.12 per share on an annualized basis, a forward yield of roughly 2.61%.

- Investment: $5,000

- Share price: $81.34

- Shares purchased: 61.47

- Quarterly dividend per share: $0.53

- Quarterly passive income: $32.58

- Annual passive income: $130.32

Every three months, that $5,000 stake quietly pushes about $32.58 back into the brokerage account. Reinvested at current prices, those checks compound at a rate dictated by Coke’s ability to keep raising the payout.

Why the Dividend Keeps Climbing

Coca-Cola is a concentrate-and-syrup business that licenses bottling and distribution to a global franchise network. The capital-light model is what makes the dividend so resilient.

The portfolio spans Coca-Cola, Coca-Cola Zero Sugar, Sprite, Fanta, Dasani, smartwater, Topo Chico, BODYARMOR, Powerade, Costa, Minute Maid, Simply, and fairlife, which gives the company pricing power across categories and geographies.

Q1 2026 results illustrate the underlying engine. Revenue came in at $12.47 billion, up 12.1% year over year, with EPS of $0.86 against an $0.81 consensus.

Operating margin expanded to 35% from 32.9%, and Coca-Cola Zero Sugar volume rose 13%. Management is guiding to 4% to 5% organic revenue growth, comparable EPS growth of 8% to 9%, and free cash flow of roughly $12.2 billion for the full year.

For context, Coca-Cola paid $8.8 billion in dividends during 2025 and repurchased $477 million of stock in Q1 2026, with roughly $5.2 billion remaining on the buyback authorization. That cushion is why the payout has compounded from $0.16 per quarter in 1999 to $0.53 today, with the most recent hike coming in at 3.92%.

Institutional Backing and the Forward View

Institutional ownership sits at 68.23% of shares outstanding, anchored by Berkshire Hathaway, which has held its stake for more than three decades. Wall Street’s average target price is $86.06, with 19 buy or strong buy ratings versus four holds and one strong sell. The next earnings report is scheduled for July 28, 2026, with consensus EPS of $0.93.

$32.58 every 90 days from a $5,000 stake is a tangible reminder of what a real dividend franchise looks like. Scale that position to $50,000 or $500,000, layer in reinvestment, and the compounding curve does the heavy lifting.

The yield is modest, the growth is steady, and the payout has survived two world recessions, a pandemic, and 11 U.S. presidents. For income investors who prize predictability over chasing yield, that track record is the product.