Defense contractors have spent the past year doing exactly what they are designed to do: Deliver predictable cash flow, lean on multi-year backlogs and reprice higher as geopolitical risk refuses to fade. With $52.9 billion earmarked for critical munitions in the FY 2027 Department of War budget request and defense ranked the standout ETF theme of 2025, the sector backdrop heading into mid-2026 favors scale, contract visibility, and production capacity.

Below are three names worth a closer look this month, each with a tool-verified data point grounding the thesis.

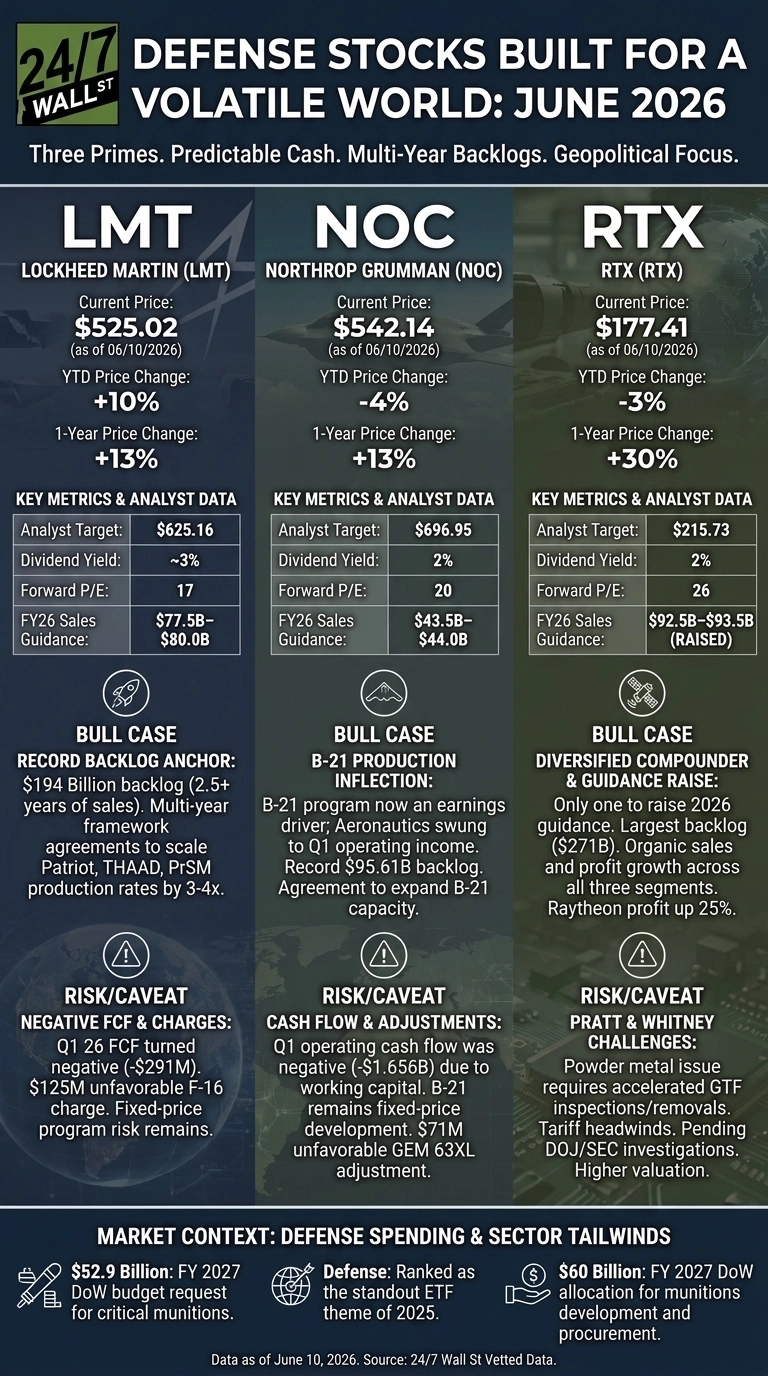

Lockheed Martin: The Backlog Anchor

Lockheed Martin (NYSE:LMT | LMT Price Prediction) trades at $525.02 as of June 10, with shares up 10% year to date and 13% over the past year. The forward P/E sits at 17, the dividend yield at roughly 3% and the analyst target price stands at $625.16.

The bull case rests on a record $194 billion backlog representing more than 2.5 years of sales and the recently signed multi-year framework agreements with the Department of War for Patriot, THAAD, and PrSM. CEO Jim Taiclet said the deals will “increase production rates of these critical systems by three to four times current rates,” locking in demand against a budget environment that wants more munitions, faster. FY2026 guidance was reaffirmed at $77.5 billion to $80.0 billion in sales and diluted EPS of $29.35 to $30.25, with operating profit expected to grow approximately 25% year over year.

The caveat is real. Q1 2026 EPS of $6.44 missed the $6.70 consensus, free cash flow turned negative at -$291 million, and a $125 million unfavorable F-16 charge reminded investors that fixed-price program risk has not gone away. The backlog buys patience; execution still needs to improve.

Northrop Grumman: The B-21 Inflection

Northrop Grumman (NYSE:NOC) trades at $542.14, down 4% year to date but still up 13% over 12 months. Trailing P/E sits at 17, forward P/E at 20, and dividend yield at 2%. The analyst target of $696.95 implies meaningful upside, with four Strong Buys and 10 Buys against nine holds. Sentiment screens bullish at a composite score of 64.72.

The thesis is straightforward: B-21 has flipped from drag to driver. Aeronautics Systems swung from a $183 million operating loss in Q1 2025 to $305 million in operating income in Q1 2026, tied to the absence of a prior-year $477 million B-21 loss provision. Backlog hit a record $95.61 billion, CEO Kathy Warden cited an “unprecedented global demand environment”, and the company secured a U.S. Air Force agreement to expand B-21 production capacity. FY2026 guidance calls for sales of $43.5 billion to $44.0 billion and MTM-adjusted EPS of $27.40 to $27.90.

The risk: Q1 operating cash flow came in at -$1.656 billion on working capital timing, and the B-21 remains a fixed-price development program. A $71 million unfavorable EAC adjustment on GEM 63XL is a reminder that any single program can bite.

RTX: The Diversified Compounder

RTX (NYSE:RTX) — parent company of Raytheon, Pratt & Whitney and Collins Aerospace — trades at $177.41. Shares are down 3% year to date but have gained 30% over the past year. Forward P/E is 26, dividend yield is 2%, and the analyst target is $215.73.

RTX is the only one of the three to raise 2026 guidance this cycle. Q1 adjusted EPS of $1.78 beat the $1.52 consensus by 17%, marking the fourth consecutive quarterly beat. Management lifted full-year sales guidance to $92.5 billion to $93.5 billion and adjusted EPS to $6.70 to $6.90. The backlog of $271 billion, split $162 billion commercial and $109 billion defense, is the largest of the three primes and the most diversified. CEO Chris Calio pointed to “organic sales and adjusted operating profit growth across all three segments,” with Raytheon adjusted operating profit up 25% on Patriot, GEM-T and naval munitions demand and Pratt commercial aftermarket up 19%.

The caveat involves the Pratt & Whitney powder metal matter requiring accelerated GTF fleet inspections and removals, ongoing tariff headwinds at Collins and Pratt, and pending DOJ deferred prosecution agreements and SEC investigations. The valuation also leaves less margin for error than the other two.

What to Watch Next

Three contracts, three risk profiles, one shared tailwind. Lockheed offers the highest backlog-to-sales ratio and the cleanest yield. Northrop carries the most operational leverage as B-21 scales. RTX provides the broadest diversification and the only raised 2026 outlook.

With $60 billion allocated to munitions development and procurement in the FY 2027 request and framework agreements rewiring how Washington buys weapons, June sets up as a month where execution, not orders, will separate the leaders.