Adobe (NASDAQ:ADBE | ADBE Price Prediction) just delivered a record quarter, raised its full-year outlook, and watched its stock fall anyway. That gap between fundamentals and price action frames our thesis.

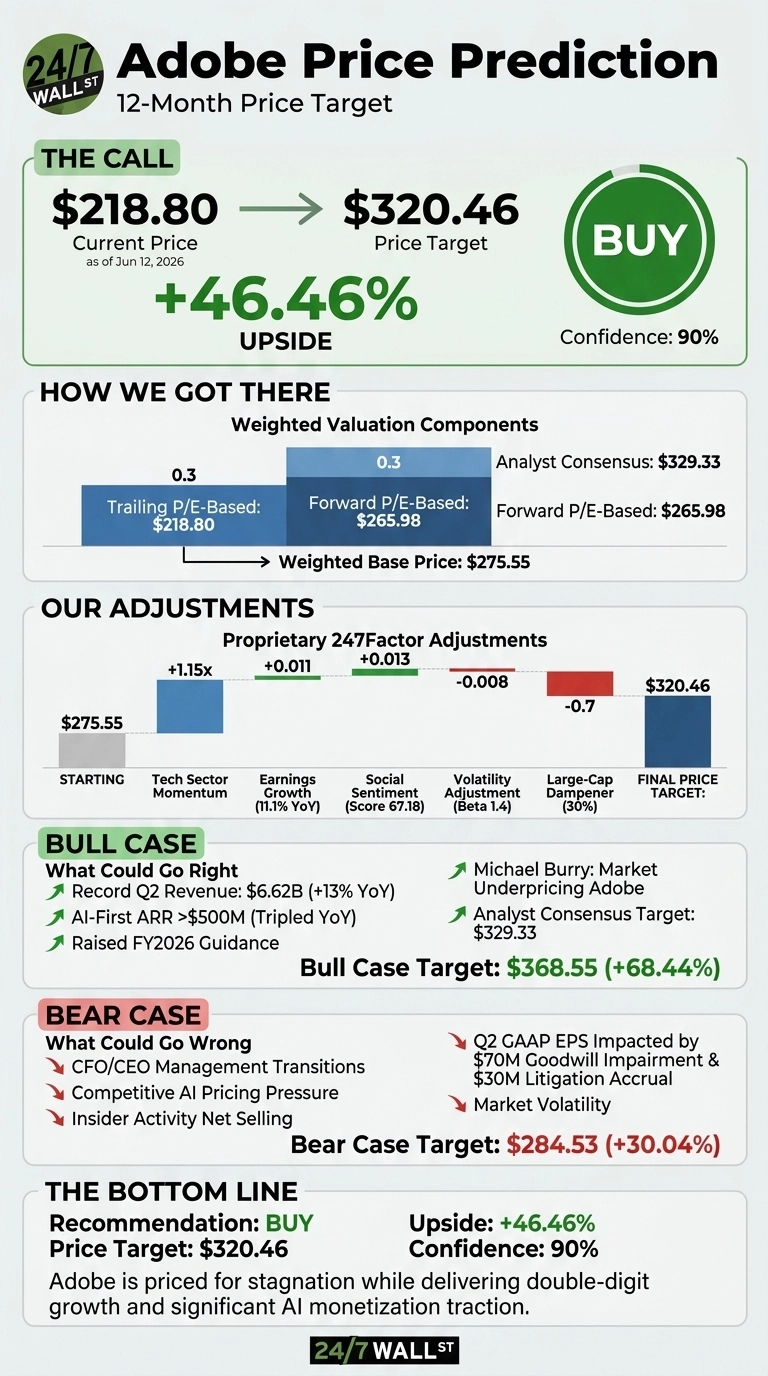

The stock trades at $218.80 after a 15.33% one-week drop and a 37.48% year-to-date decline. Our 24/7 Wall St. price target for Adobe is $320.46, implying 46.46% upside over the next 12 months. Our model rates Adobe buy with 90% confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $218.80 |

| 24/7 Wall St. Price Target | $320.46 |

| Upside | 46.46% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Record Quarter Met With a Selloff

Adobe reported Q2 FY2026 on June 11, 2026, with record revenue of $6.62 billion, up 13% year over year, and non-GAAP EPS of $5.96, the fifth consecutive beat. AI-first ARR tripled year over year and exceeded $500 million, while total Adobe ARR hit $27.10 billion.

Management raised the full-year FY2026 revenue range to $26.50 billion to $26.60 billion and non-GAAP EPS to $24.35 to $24.45.

The stock still fell 6.25% on June 11. The market focused on the abrupt departure of CFO Dan Durn, announced just months after CEO Shantanu Narayen disclosed his own transition. Add a sector-wide software selloff (Autodesk dropped 5.4% the same day) and you get a stock 19% below its 52-week high of $405.00.

The Case for $368 and Higher

Our bull scenario points to $368.55, a 68.44% return. The driver is AI monetization. CEO Shantanu Narayen said, “Adobe delivered record revenue of $6.62 billion in Q2 reflecting strong AI-driven demand across our customer groups and we are raising our full-year fiscal 2026 revenue and non-GAAP EPS targets on the strength of that performance.”

The Business Professionals & Consumers segment accelerated 16% YoY, Semrush is contributing roughly $480 million in ARR, and operating cash flow hit $2.17 billion in the quarter. Investor Michael Burry has argued the market is underpricing Adobe, citing AI asset potential. Of 39 analysts, 15 rate Adobe a Buy or Strong Buy, with a consensus target of $329.33.

What Could Go Wrong

Our bear scenario still lands at $284.53, a 30% return, but the risks deserve respect. CFO Dan Durn exits June 15, 2026, stacking a finance transition onto a CEO transition. Generative AI competitors are pressuring pricing power, and GAAP EPS of $4.25 absorbed a $70 million goodwill impairment on the Publishing & Advertising unit plus a $30 million litigation accrual.

Bulls would counter that both charges are non-cash or non-recurring and that Adobe repurchased 8.5 million shares for $2.111 billion in Q2 alone. Insider activity skews net selling, a yellow flag worth monitoring.

Adobe Price Prediction 2026-2030

The 24/7 Wall St. price target of $320.46 reflects a buy with 90% confidence. Adobe trades at a forward multiple of 10x with a PEG ratio of 0.675, valuations more typical of a no-growth utility than a software franchise growing subscriptions 14% YoY.

The thesis strengthens if the interim CFO communicates continuity at the next earnings call. It weakens if AI-first ARR growth meaningfully decelerates from its current tripling pace. The valuation does the heavy lifting in our thesis.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $320.46 |

| 2027 | $395.00 |

| 2028 | $472.00 |

| 2029 | $548.00 |

| 2030 | $627.81 |

These projections assume Adobe continues converting its AI investments into paid ARR at the current trajectory and that subscription growth holds near the 10.2% ARR growth management has guided. Significant upside could come from Semrush integration accelerating Digital Experience growth, while downside risk centers on competitive AI disruption.

Contact [email protected] for any questions or corrections.