Toyota’s (NYSE:TM | TM Price Prediction) American depositary receipts have taken a beating in 2026, sliding 18.27% year to date as U.S. tariffs gut North American profitability and global volumes soften. Yet the setup remains compelling.

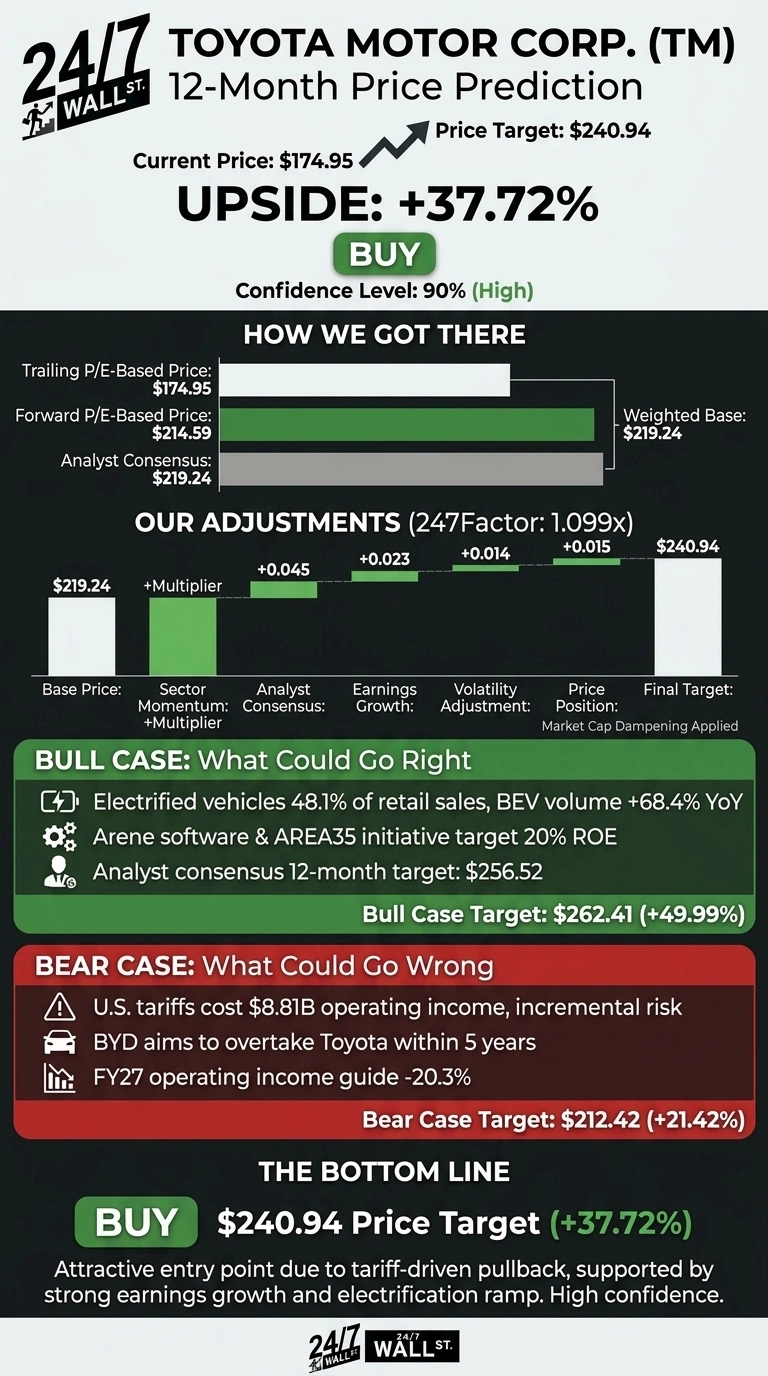

The stock trades at $174.95, and the 24/7 Wall St. price target points to $240.94 over the next 12 months. That signals meaningful upside for the world’s largest automaker, and the model rates shares a buy with high conviction.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $174.95 |

| 24/7 Wall St. Price Target | $240.94 |

| Upside | 37.72% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Tariff-Driven Reset Has Created an Entry Point

Toyota shares peaked at $245.51 in February 2026 and have unwound to current levels, leaving the stock down 6.39% over the past month and 2.43% over the past year.

The pullback stems from a brutal FY2026 result reported on May 8, 2026: full-year revenue of $323.62B, operating income down 21.5% to $24.05B, and a $8.81B direct hit from U.S. tariffs. North America swung to a $1.23B operating loss.

Global vehicle sales fell 3.1% year over year in April, Middle East exports collapsed 91.7%, and SoftBank surpassed Toyota as Japan’s largest company by market cap for the first time in 20 years. Weekly RSI sits at 33.35, an oversold reading that historically marks reversal zones.

The Case for $262 and Higher

The bull-case scenario lands at $262.41, a 49.99% return. Electrified vehicles account for 48.1% of retail sales, BEV volume jumped 68.4% to 243K units in FY26, and Toyota guides FY27 BEV sales to 598K units, up 146.1%.

The Arene software platform, AREA35 production initiative, and a value-chain push targeting JPY 2.1T by 2030 build a credible 20% ROE roadmap.

Analyst targets back this optimism. Freedom Capital upgraded Toyota to Buy with a $230 target, citing hybrid demand approaching 5M units. The consensus 12-month target of $256.52 reflects 2 Strong Buy, 1 Buy, and 1 Hold rating. A $23.35B Toyota Industries take-private settled in May 2026 tightens governance and removes a long-standing cross-holding overhang.

The Risks Worth Watching

The bear scenario pencils to $212.42, a positive return but well shy of the base case. FY27 guidance calls for operating income to fall 20.3% to roughly $19.16B, including a 400B yen incremental tariff and Middle East drag. BYD’s chairman has publicly targeted overtaking Toyota within five years, and China profitability remains under pressure.

Bulls argue the FY27 guide bakes in conservative 150 yen/USD FX and front-loads tariff risk. Operating cash flow of $34.94B and an $80.83B cash pile leave room to absorb the cycle. At a 10 P/E and 0.92 price-to-book, the downside is already priced in.

Toyota Price Prediction 2026-2030

The 24/7 Wall St. price target of $240.94 represents 37.72% upside, and I’m leaning into the buy rating with 90% confidence. The tipping factor is valuation: an oversold mega-cap trading near 9x earnings with positive free cash flow, a 3.58% dividend yield, and a credible electrification ramp.

The setup looks favorable on a 12 to 18 month horizon. I’d stay on the sidelines if you expect U.S. tariffs to escalate further or if FY27 guidance gets cut at the half-year mark.

Looking ahead, here is where our model projects Toyota could trade, assuming current growth trajectories and tariff conditions normalize.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $240.94 |

| 2027 | $300.92 |

| 2028 | $351.27 |

| 2029 | $394.12 |

| 2030 | $429.30 |

These projections assume Toyota executes on its hybrid and BEV roadmap and that U.S. tariff pressure eases by FY28. Material upside or downside could come from a BYD-driven share shift, a sharper yen reversal, or breakthrough adoption of the Arene software stack.

Contact [email protected] for any questions or corrections.