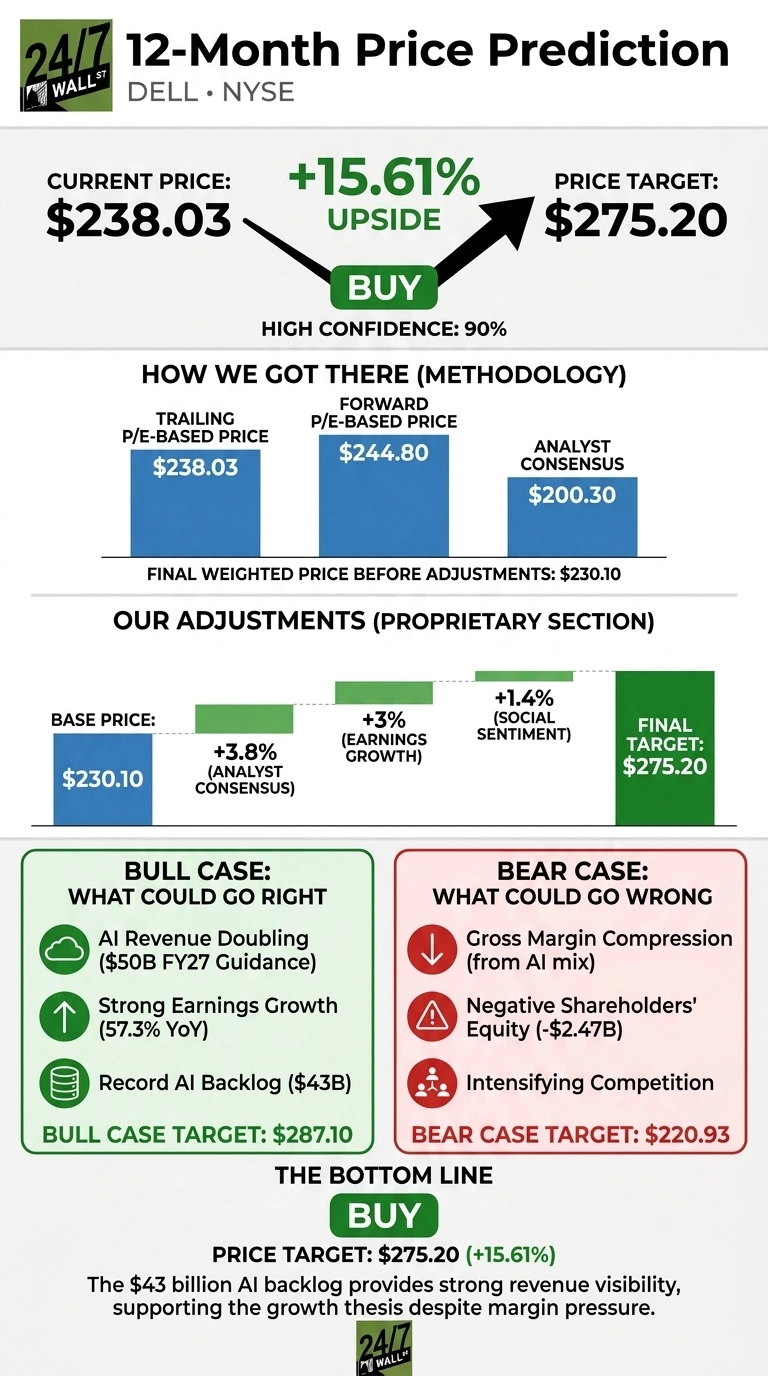

Dell Technologies (NYSE:DELL | DELL Price Prediction) has gone from a value name to an AI infrastructure powerhouse, and our proprietary model still sees more room to run. The 24/7 Wall St. price target for Dell is $275.20 over the next 12 months, implying upside of 15.61% from the current $238.03. The recommendation is buy, with a high confidence reading of 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $238.03 |

| 24/7 Wall St. Price Target | $275.20 |

| Upside | 15.61% |

| Recommendation | BUY |

| Confidence Level | 90% |

An AI-Fueled Rerating Has Already Begun

Dell is up 90.55% year to date and 111.69% over the past year, with a one-month gain of 21.46%. Shares sit 24% below the 52-week high of $263.99, after a Q4 FY26 earnings report that reset the narrative.

Revenue hit $33.379 billion (up 40.21% YoY), non-GAAP EPS came in at $3.89 versus the $3.51 estimate, and AI-optimized server revenue surged 342% YoY to $8.952 billion. Dell exited FY26 with a record $43 billion AI backlog after booking $64 billion in AI orders for the year.

Why Bulls See $287 and Beyond

The bull case rests on AI infrastructure demand outpacing Dell’s already raised guidance. Management guided FY27 revenue to a midpoint of $140 billion (up 23%), with AI server revenue roughly doubling to $50 billion and non-GAAP EPS of $12.90.

Q1 FY27 alone is pegged at $2.90 EPS, up 87% YoY. Free cash flow of $8.55 billion, a 20% dividend hike, and a $10 billion buyback expansion underline the capital return story. Our bull scenario lands at $287.10 over 12 months.

The Risks Worth Watching

The bear case starts with margins. FY26 gross margin compressed to 20% from 21.4%, dragged by lower-margin AI server mix. Shareholders’ equity is negative at -$2.470 billion, supplier concentration on AI silicon is real, and competition from HPE and Supermicro is intensifying.

Bulls would counter that the negative equity reflects aggressive buybacks (about 54 million shares repurchased in FY26) and that operating income still grew 30.66%. Our bear scenario takes shares to $220.93, a modest 7.18% drawdown.

Dell Price Prediction 2026-2030

I land on buy with our 24/7 Wall St. price target of $275.20 and a 90% confidence reading. The tipping factor is the $43 billion AI backlog, which gives Dell visibility most hardware peers lack.

The setup looks constructive if Q1 FY27 confirms the 51% revenue ramp management guided. I’d stay on the sidelines if gross margin slips below 19% on a sustained basis, signaling AI mix is destroying more value than it creates.

Looking further out, here is where our model projects Dell could trade, assuming current AI server momentum and margin stabilization hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $275 |

| 2027 | $305 |

| 2028 | $335 |

| 2029 | $360 |

| 2030 | $380 |

These projections assume Dell sustains AI server share gains and stabilizes gross margin in the 20% to 21% range. Significant upside or downside could result from sovereign AI demand, NVIDIA roadmap timing, or a hyperscaler capex pullback.

Contact [email protected] for any questions or corrections.