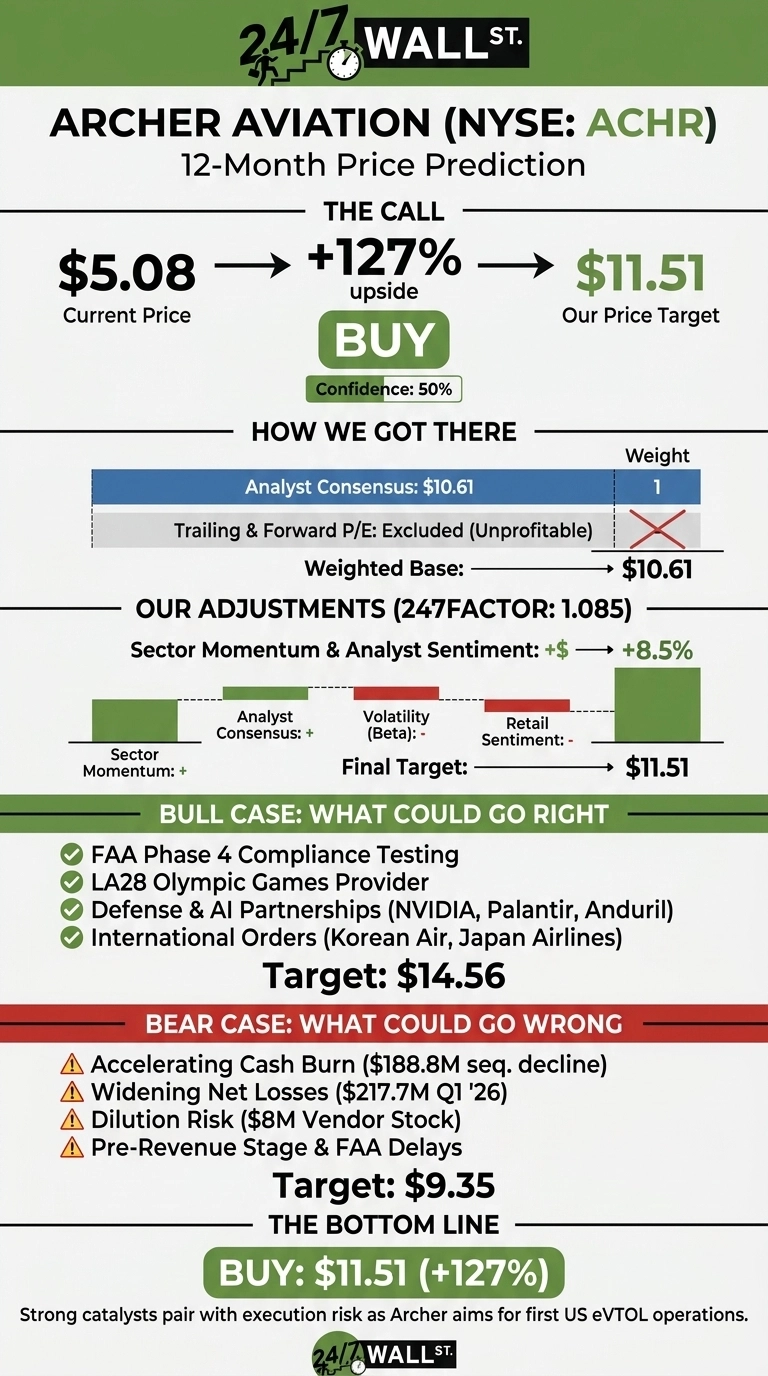

Archer Aviation (NYSE:ACHR | ACHR Price Prediction) has had a rough year. After running up above $14.62 in the last 52 weeks, the eVTOL hopeful now trades at $5.08, down 32.45% year to date.

Our 24/7 Wall St. price target for Archer Aviation is $11.51 over the next 12 months, implying 126.61% upside. The model rates Archer a buy with a moderate 50% confidence level, reflecting strong catalysts paired with real execution risk.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $5.08 |

| 24/7 Wall St. Price Target | $11.51 |

| Upside | 126.61% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Brutal Six Months, But Catalysts Are Lining Up

Archer has lost 22.09% in the past month and 56.69% over the trailing year. Q1 2026, filed May 11, 2026, showed EPS of -$0.28 against a -$0.24 consensus and a net loss of $217.7 million on just $1.60 million of revenue. Cash fell $188.8 million sequentially to $951.1 million.

CEO Adam Goldstein called it “another banner quarter”, pointing to “record FAA certification progress” and a strategy spanning air taxis, defense, and AI software. A June 26, 2026 shareholder vote on Texas reincorporation is the next governance milestone.

The Case for $14 and Higher

The bull case rests on Archer becoming the first US eVTOL operator. They are the first eVTOL company to close Phase 3 of the FAA’s four-phase Type Certification process and the FAA has accepted 100% of 797 Means of Compliance.

Add the LA28 Olympics provider designation, partnerships with Korean Air (up to 100 aircraft), Japan Airlines, and Saudi PIF, plus a defense program with Anduril powered by NVIDIA’s IGX Thor and Palantir’s SMART AI work, and Archer becomes a multi-platform play.

The bull scenario points to $14.56, a 186.57% return. H.C. Wainwright carries a $18 Buy target. ARK holds 4.94% and BlackRock 6.9%, signaling institutional conviction.

What Could Go Wrong

The bear thesis is straightforward: Archer burns cash at scale with almost no revenue. Q1 2026 R&D hit $171.7 million against $1.6 million of sales, and net losses widened 133.08% year over year. An $8 million vendor stock issuance in May highlighted dilution risk, and Goldman Sachs recently moved to Hold. The bear scenario projects $9.35, still above today’s price but well below the base target.

May 2026 insider sales by the CTO, CLO, Interim CFO, and Chief Accounting Officer were tax-driven, tied to RSU vesting. CEO Adam Goldstein received a 788,552 share deferred RSU grant with no sales.

Archer Aviation Price Prediction 2026-2030

The 24/7 Wall St. price target of $11.51 implies 126.61% upside and our model rates Archer a buy at 50% confidence. The key tipping factor is FAA Phase 4 progress paired with the LA28 contract and a defense pipeline the Street is not yet pricing in.

The bull case strengthens if Archer begins commercial US operations in the second half of 2026 as guided. The thesis weakens if Phase 4 slips into 2027 or if another dilutive raise lands before revenue scales.

Here is where our model projects Archer could trade, assuming certification holds and commercial revenue scales as planned.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $11.51 |

| 2027 | $17.50 |

| 2028 | $26.00 |

| 2029 | $36.00 |

| 2030 | $48.30 |

These projections assume Archer executes on FAA certification, scales Midnight production to 50 aircraft annually, and converts conditional international orders into revenue. Certification delays would drive significant downside, while defense award wins could accelerate the bull case.

Contact [email protected] for any questions or corrections.