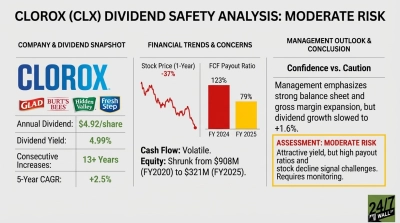

Few consumer staples have been treated as roughly by the higher-for-longer rate regime as Clorox (NYSE:CLX | CLX Price Prediction). The stock sits down 18.6% over the past year, pushing the yield to a level rarely seen for a household-name aristocrat. With Goldman Sachs (NYSE:GS) projecting the Fed to cut another 50 basis points to 3-3.25% in 2026, income investors are starting to look back. The question I want to answer is simple: can Clorox actually afford this payout?

A 5.2% Yield Backed by a Multi-Decade Streak

| Metric | Value |

|---|---|

| Annual Dividend | $4.96 |

| Dividend Yield | 5.21% |

| Consecutive Years of Increases | 51 years |

| Most Recent Increase | $1.22 to $1.24 quarterly (Q3 2025) |

| Dividend King Status | Yes |

Payout Ratios Are Stretched, but Cash Flow Still Covers

Clorox paid roughly $600 million in dividends against $761 million in FY2025 free cash flow. Trailing EPS of $6.15 against the $4.96 dividend produces an earnings payout ratio in the low 80s, which is elevated for a staples name.

| Metric | TTM Value | Assessment |

|---|---|---|

| Earnings Payout Ratio | ~81% | Elevated |

| FCF Payout Ratio | ~79% | Elevated |

| Operating Cash Flow Coverage | 1.64x | Adequate |

The wrinkle: FY2026 adjusted EPS guidance of $5.45 to $5.65 implies the earnings payout climbs near 90% before the ERP transition normalizes. FCF is the better lens here, and it still works.

Thin Equity, but a $1.2 Billion Cash Cushion

| Metric | Value | Assessment |

|---|---|---|

| EBITDA (TTM) | $1.274B | Stable |

| EV/EBITDA | 11.2x | Reasonable |

| Cash on Hand | $1.187B | Solid Buffer |

| Shareholders’ Equity | $92M | Thin (buyback-driven) |

The negative book value is optical, the byproduct of decades of buybacks. The cash position, up 425% year-over-year, is the real story and gives management room to absorb GOJO integration costs.

Half a Century of Raises, Now Slowing

| Year | Annual Dividend |

|---|---|

| 2026 | $4.96 |

| 2025 | $4.88 |

| 2024 | $4.84 |

| 2023 | $4.72 |

| 2022 | $4.64 |

The 5-year dividend CAGR works out to roughly 2.2%, modest but unbroken.

Rendle Stays Measured

CEO Linda Rendle told investors on the Q3 FY26 call: “Looking ahead, we recognize there is more work to do in what continues to be a challenging consumer and cost environment.” That tone is measured and capital-allocation focused. Capital allocation language remains anchored to the dividend.

The Verdict: Safe, With a Watch on FY2026 Earnings

Dividend Safety Rating: Safe. FCF covers the payout with room, the cash buffer is real, and the streak is intact. The dividend thesis holds together if FY2026 organic sales stabilize and ERP normalization plays out as guided. The setup deteriorates if the earnings payout pushes past 95% on further guidance cuts. For now, the yield is doing its job.