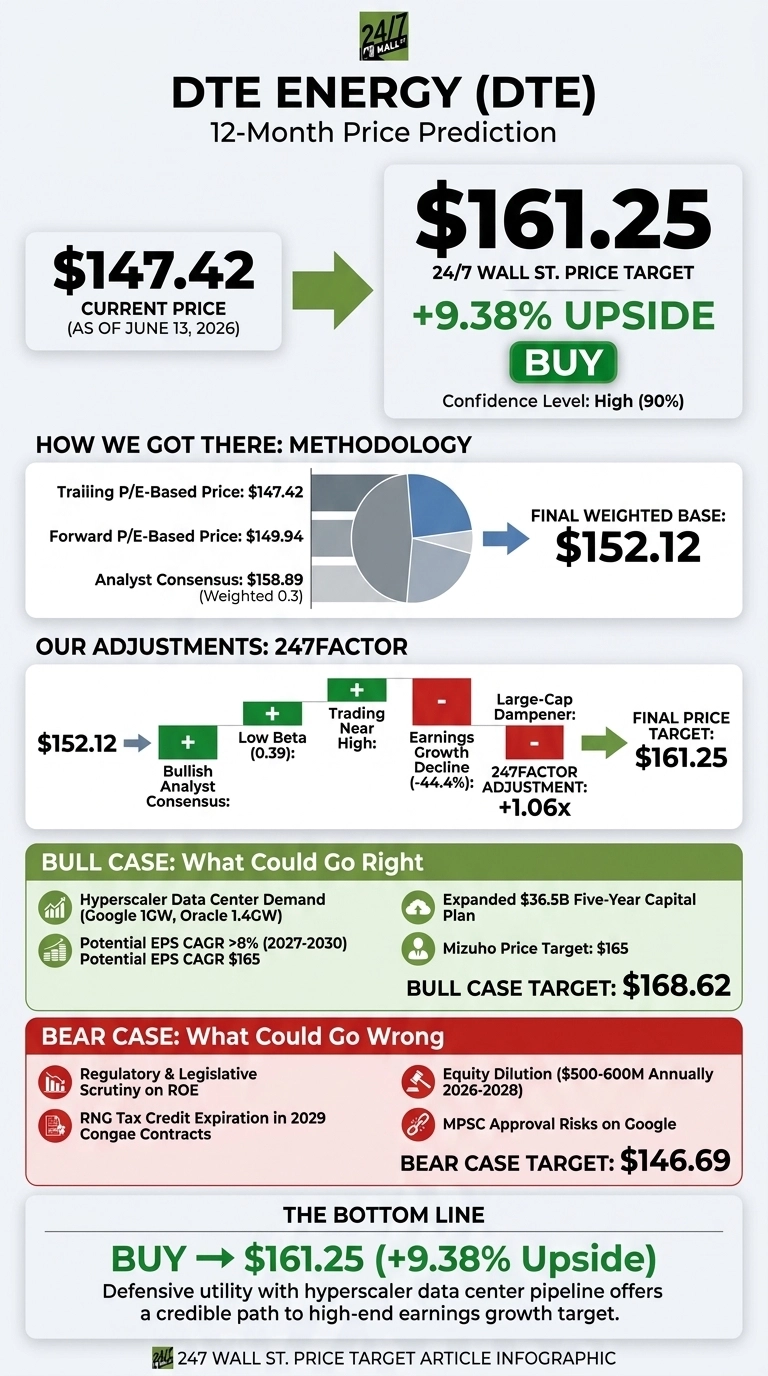

Our 24/7 Wall St. price target for DTE Energy (NYSE:DTE | DTE Price Prediction) is $161.25 over the next 12 months, implying 9.38% upside from the current price of $147.42. I rate DTE a buy with high confidence.

The hyperscaler data center pipeline, expanded capital plan, and constructive Michigan regulatory backdrop give this defensive utility a credible path to compound at the high end of its 6%-8% EPS growth target.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $147.42 |

| 24/7 Wall St. Price Target | $161.25 |

| Upside | 9.38% |

| Recommendation | BUY |

| Confidence Level | 90% |

How DTE Got Back to $147

DTE has had a strong run into mid-2026. The stock is up 15.19% year to date and 12% over the past year, trading just 3% below its 52-week high of $153.72. A $1.6 billion battery storage partnership with LG Energy Solution Vertech announced June 5 helped DTE jump 5.53% on the news, and Wells Fargo raised its price target to $165 from $160 on June 12.

Earnings were a mixed picture. Q1 2026 operating EPS of $1.95 missed the $2.03 consensus by 4.14%, with net income down 44.37% year over year on Energy Trading timing and higher interest expense. But Q4 2025 beat by 8.29%, and full-year 2025 operating EPS of $7.36 exceeded the high end of guidance.

The Case for $168+

The bull case rests on hyperscaler demand. DTE has secured a 19-year, 1.4 GW Oracle power supply agreement in Saline Township and filed contracts for a 1 GW Google data center in Van Buren Township, which could drive $5 billion in incremental capital through 2032.

Another 5 GW of hyperscaler load is in late-stage negotiation, with management noting EPS CAGR could exceed 8% from 2027-2030. The expanded $36.5 billion five-year capital plan and Wells Fargo’s $165 target support our bull-case price of $168.62.

The Risks Worth Watching

Bears point to Michigan legislative scrutiny on ROE caps and executive compensation, MPSC approval risk on the Google contracts, and equity dilution from $500-$600 million in planned annual issuances through 2028. The Q1 EPS miss and a fresh $1 billion debt offering at a 6.20% initial rate raise leverage concerns.

RNG tax credit expiration in 2029 will reduce DTE Vantage earnings to a projected $150-$160 million in 2030. It should be noted, however, that the Q1 weakness reflected timing items in Energy Trading and Corporate, while DTE Electric operating earnings rose $71 million year over year. The bear case price is $146.69.

DTE Energy Price Prediction 2026-2030

The 24/7 Wall St. price target of $161.25 and buy recommendation come with 90% confidence. The key factor tipping the scale is the data center pipeline layered on a regulated Michigan utility with a 3.09% dividend yield and beta below 0.4.

The setup favors investors seeking defensive exposure to the AI power buildout. The thesis weakens materially if Michigan legislators successfully cap utility ROE or MPSC delays the Google contracts.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $161.25 |

| 2030 | $206.88 |

These projections assume DTE executes on its 6%-8% EPS growth target and brings the Google and Oracle data center loads online. Significant upside could come from incremental hyperscaler agreements, while downside risk centers on adverse rate case outcomes or capital project delays.

Contact [email protected] for any questions or corrections.