Oracle (NYSE:ORCL | ORCL Price Prediction) has whipsawed investors over the past year, rising from below $160 to a peak above $300 last October before retreating. With the stock consolidating around $186 and a $553 billion AI backlog on the books, the risk/reward has shifted to the long side.

Our 24/7 Wall St. Price Target for Oracle

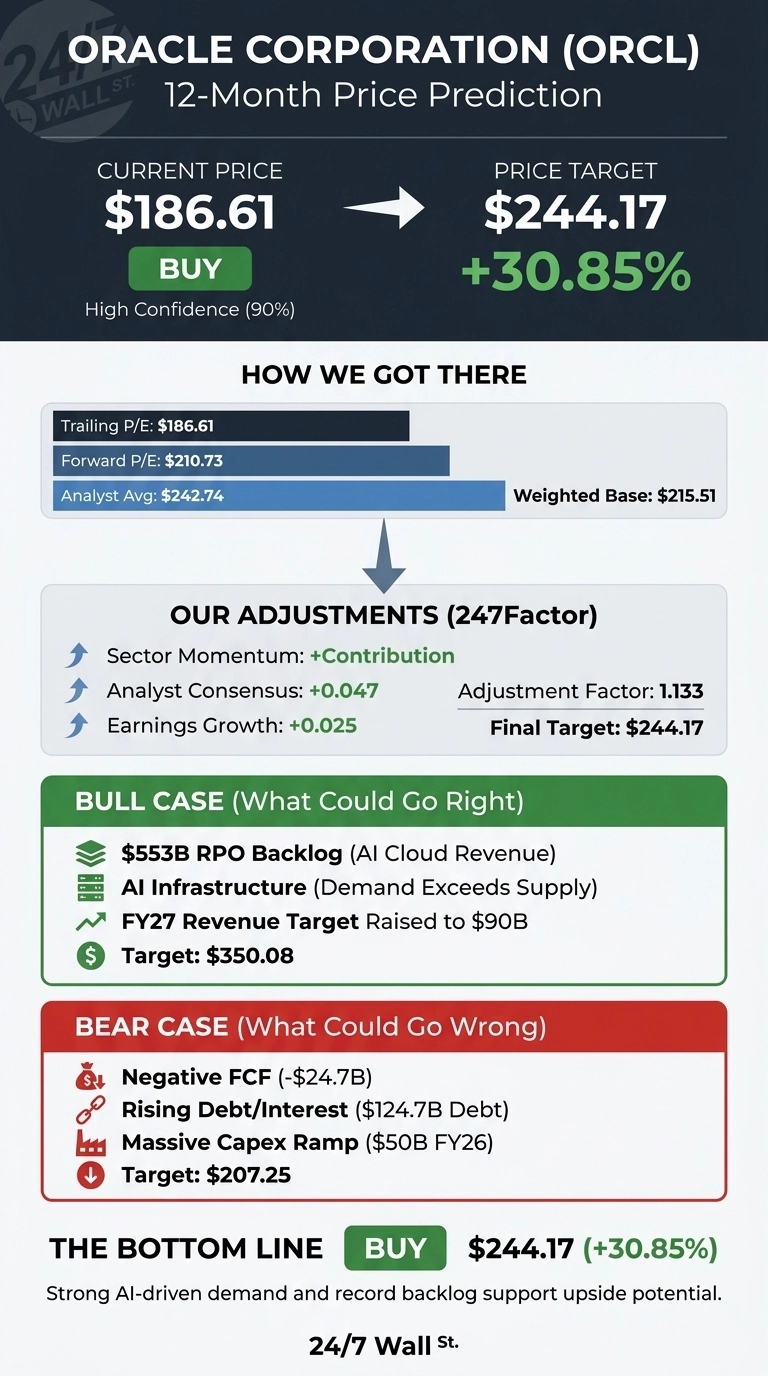

ORCL stock trades at $186.61 as of the May 18, 2026 close. Our 24/7 Wall St. price target is $244.17, implying 30.85% upside over the next twelve months. The recommendation is buy with a 90% confidence score.

| Metric | Value |

|---|---|

| Current Price | $186.61 |

| 24/7 Wall St. Price Target | $244.17 |

| Upside | 30.85% |

| Recommendation | BUY |

| Confidence Level | 90% |

From a $343 Peak to a Mid-Range Reset

Oracle is 29% below its 52-week high of $343.01 and well off the February low of $153.97. Shares are down 3.67% YTD but up 17.44% over the trailing year and up 6.6% over the past month.

The reset came after Q2 FY26 in December, when revenue missed by 5% and shares fell 13% despite a 32.43% EPS beat. Q3 FY26, reported March 10, reset the narrative. Revenue hit $17.19 billion, EPS came in at $1.79, and Cloud Infrastructure grew 84% to $4.89 billion. Remaining performance obligations jumped 325% to $553 billion, and management raised the FY27 revenue target to $90 billion.

The Case for $300+

The bull case starts with the backlog. CFO Safra Catz outlined a path for Oracle Cloud Infrastructure to grow from $18 billion in FY26 to $32 billion, $73 billion, $114 billion, and $144 billion over four years, with “Most of the revenue in this 5-year forecast is already booked in our reported RPO.” Multicloud database revenue is growing 531%, and co-CEO Mike Sicilia noted “All of the top five AI Models are in the Oracle Cloud.”

Wall Street agrees. The analyst tally shows 7 Strong Buy, 28 Buy, 8 Hold, 1 Sell with a consensus target of $242.74. Our internal bull case projects $350.08 within twelve months, an 87.6% return if capacity delivery accelerates and AI demand outpaces supply.

What Could Go Wrong

The bear case centers on capital intensity. Trailing free cash flow is negative $24.74 billion, capex runs at a $50 billion FY26 pace, non-current debt has climbed to $124.7 billion, and interest expense is up 32%. Customer concentration in hyperscale AI buyers is real, and concerns about OpenAI missing revenue and user targets pose a pipeline risk.

The counter is that capex is contracted revenue waiting to happen. Co-CEO Clay Magouyrk told analysts “A combination of bring-your-own-hardware and upfront customer payments enables us to continue expanding without any negative cash flow from Oracle Corporation” on new contracts. Our bear scenario still lands at $207.25, an 11.06% gain from here.

Our Take at Current Levels

The 24/7 Wall St. price target of $244.17 and buy rating reflect 90% confidence on a stock trading at a reasonable 26x forward earnings against a backlog growing triple digits.

The bull thesis holds if Oracle converts even half its $553 billion RPO on schedule. The bear thesis takes over if hyperscale AI capex rolls over in 2027. Insider activity skews toward buying and trailing 30-day sentiment is up 17.67 points, favoring the bulls.

Oracle Price Prediction 2026-2030

Our model projects Oracle could trade as follows, assuming current growth trajectories and the OCI ramp hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $244 |

| 2027 | $285 |

| 2028 | $334 |

| 2029 | $388 |

| 2030 | $403 |

Significant upside or downside could come from faster-than-expected datacenter delivery, GPU supply normalization, or a slowdown in hyperscale AI spending.

Contact [email protected] for any questions or corrections.