The headline question has a clean answer. DraftKings (NASDAQ:DKNG | DKNG Price Prediction) would need to roughly double from $28.79 to clear $57 by year-end 2026, and our proprietary model does not see it happening in that window. That said, we are still constructive on the stock from here.

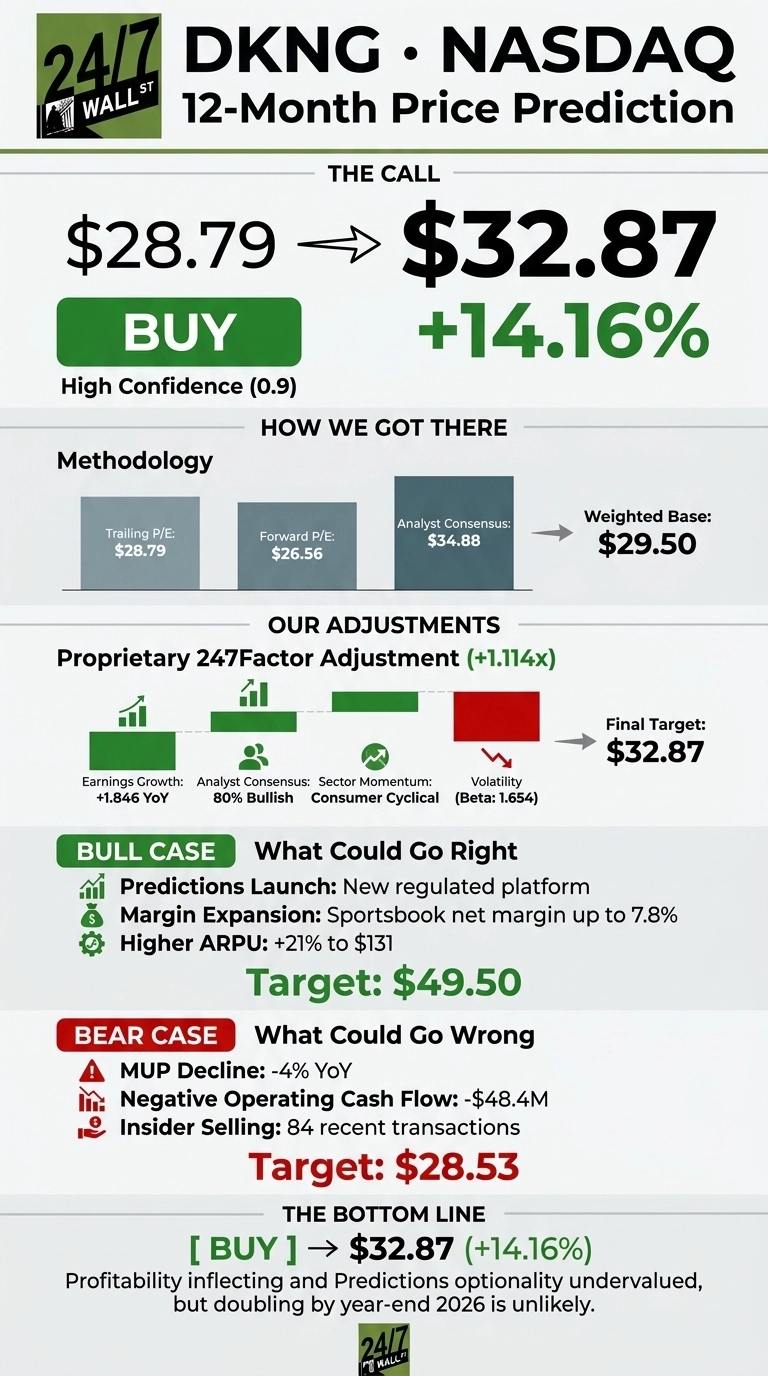

Our 24/7 Wall St. price target for DraftKings is $32.87, implying 14.16% upside over the next 12 months. The recommendation is buy, with high confidence at 0.9.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $28.79 |

| 24/7 Wall St. Price Target | $32.87 |

| Upside | 14.16% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Volatile Year That Reset Expectations

DKNG has rallied 16.18% in the past week and 15.16% over the past month, but the stock is still down 16.45% year-to-date and 21.12% over the trailing year. Shares sit roughly 28% below the 52-week high of $48.78, after bottoming near $20.46.

Q1 2026 results reframed the story. Revenue of $1.65 billion beat consensus by 4.54%, sportsbook revenue rose 24.1%, and adjusted EBITDA jumped 64% to $167.85 million. EPS of $0.20 missed the $0.36 estimate, but management reaffirmed full-year revenue guidance of $6.50 billion to $6.90 billion.

Why Bulls See a Breakout Ahead

Our 1-year bull scenario lands at $49.50, a 71.94% return that gets close to doubling without quite touching it. Drivers include the launch of DraftKings Predictions, the CFTC-regulated event-contracts platform CEO Jason Robins says will deliver a “leadership position in Sports Predictions before year-end.”

Sportsbook net revenue margin expanded to 7.8% from 6.4%, and average revenue per user climbed 21% to $131. Wall Street agrees: 23 Buy ratings, 5 Strong Buys, and a consensus target of $34.88.

What Could Go Wrong

Monthly Unique Payers fell 4% YoY, operating cash flow turned negative at -$48.4 million, and DKNG carries a stretched trailing P/E of 322. Bulls would counter that the MUP drop reflects a deliberate shift toward higher-value users (ARPU up 21%) and that the cash-flow dip reflects heavy Predictions investment, not deteriorating economics.

Still, insiders have been net sellers across 84 recent transactions, including director Matthew Kalish’s 1.9 million-share forward sale contract. Our bear case lands at $28.53, essentially flat.

DraftKings Price Prediction 2026-2030

The 24/7 Wall St. price target of $32.87 and buy rating reflect a real but bounded thesis. Profitability is inflecting, the Predictions optionality is undervalued at current levels, and Wall Street’s $34.88 consensus backs us up.

The setup looks more attractive if DKNG holds the 50-day moving average near $24.44 and Predictions launches on schedule. The thesis weakens if MUPs decline another quarter or sportsbook hold percentage compresses on unfavorable outcomes. The stock can rally meaningfully from $28.79, but doubling to $57 by December is not our base case.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $32.87 |

| 2027 | $36.50 |

| 2028 | $39.75 |

| 2029 | $42.10 |

| 2030 | $44.69 |

These projections assume DraftKings continues executing on margin expansion and Predictions ramps as guided. Material upside or downside could come from iGaming legalization in major states like New York or California, or from regulatory friction around CFTC event contracts.

Contact [email protected] for any questions or corrections.