Few stocks have whipsawed investors in 2026 quite like DraftKings (NASDAQ:DKNG | DKNG Price Prediction). After hitting $48.78 last summer, shares fell to a 52-week low in February 2026 on guidance concerns and prediction-market competition fears. With the stock stabilizing, our model sees limited remaining upside from current levels.

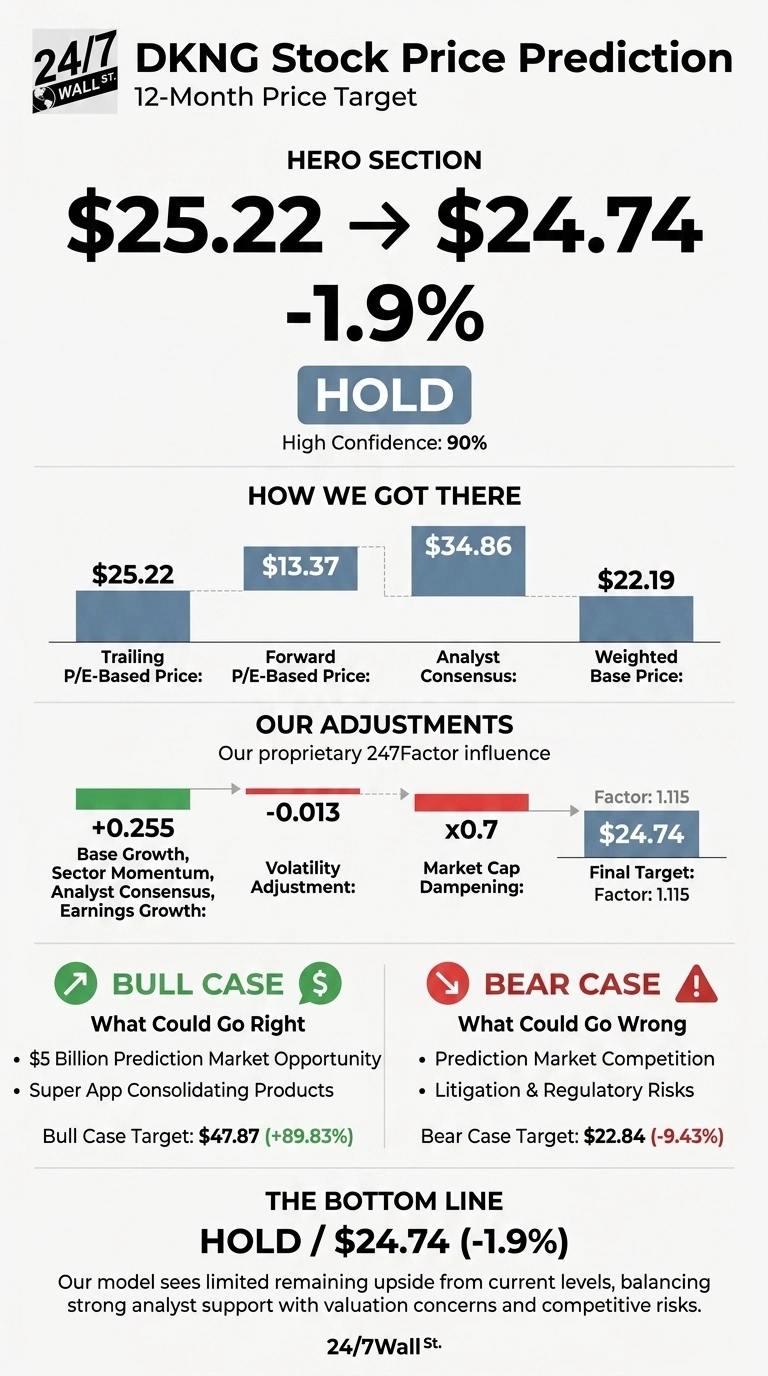

Our 24/7 Wall St. price target for DraftKings is $24.74 over the next 12 months, implying -1.9% downside from the current price of $25.22. Our recommendation is hold, with 90% confidence reflecting strong analyst data and clear earnings visibility.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $25.22 |

| 24/7 Wall St. Price Target | $24.74 |

| Upside/Downside | -1.9% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target sits just below where DraftKings trades today. DKNG is one of the most divisive consumer names in the market, and meaningful upside could come from the $5 billion prediction-markets opportunity Macquarie analyst Chad Beynon flagged, or from the recently launched Super App consolidating Sportsbook, Predictions, Casino and Lottery. A full bull case follows below.

A Volatile Year and a Soft Q1 2026

DKNG has rallied 8.15% in the past week and 9.89% over the past month, but remains down 26.81% year to date and 27.26% over one year. The slide accelerated after February’s 20.1% post-earnings drop, despite posting its first full-year GAAP profit of $3.71 million on $6.05 billion in 2025 revenue, up 26.99% YoY.

Q1 2026 confirmed the choppy backdrop. DraftKings reported revenue of $1.65 billion, up 16.8% YoY, with EPS of $0.20 versus $0.12 a year ago, missing the $0.22 consensus by 6.98%. Sportsbook revenue hit $1.09 billion while Monthly Unique Payers came in at 4.2 million, below the 4.63 million estimate.

The Case for $35+

Bulls point to Wall Street’s consensus target of $34.86 implying 38.22% upside, supported by 28 Buy ratings versus 7 Holds and zero Sells. CEO Jason Robins called the Predictions opportunity “a massive, incremental opportunity”, and 2026 guidance of $6.5 billion to $6.9 billion in revenue with $700 million to $900 million in adjusted EBITDA still implies expansion.

Independent Vice Chairman Harry Sloan bought 100,000 shares for $2.18 million in February, a constructive signal. The bull-case scenario points to $47.87 within 12 months, an 89.83% return.

What Could Go Wrong

The bear case starts with prediction-market competition. ClearBridge Investments exited DKNG in January 2026, citing rising competition from Kalshi and Polymarket. Litigation risk is mounting, including a PHAI product liability suit alleging “unreasonably dangerous” addictive design, and a New York Fed study linking online sports betting to debt delinquency.

Bulls counter that DKNG was dismissed from a Pennsylvania class action in March, and aggressive Predictions investment, while pressuring near-term margins, built the Sportsbook moat. The bear-case scenario lands at $22.84.

Hold for Now

Our price target is $24.74, a hold with 90% confidence. A forward P/E near 42x leaves no margin for execution slips while litigation and prediction-market disruption play out. The bull catalyst would be Predictions showing clear cross-sell economics in the March 2026 Investor Day follow-through, or DKNG reclaiming double-digit Sportsbook handle growth with stable hold. The bear catalyst is MUPs continuing to trend below estimates, as they did in Q1.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $24.74 |

| 2027 | $25.50 |

| 2028 | $26.25 |

| 2029 | $26.90 |

| 2030 | $27.56 |

These projections assume DraftKings executes on the Sportsbook and iGaming flywheel while ramping Predictions responsibly. Significant upside could come from federal CFTC clarity unlocking nationwide Predictions reach, while downside risk centers on adverse litigation outcomes or escalating state tax rates.

Contact [email protected] for any questions or corrections.