Our DraftKings (NASDAQ:DKNG | DKNG Price Prediction) price prediction lands within striking distance of where the stock trades today. After a brutal twelve months for shareholders, the question is whether the prediction markets pivot and Sportsbook margin expansion can outrun the litigation overhang and softer engagement metrics. My read: the risk/reward is balanced, with a slight tilt toward patient accumulation.

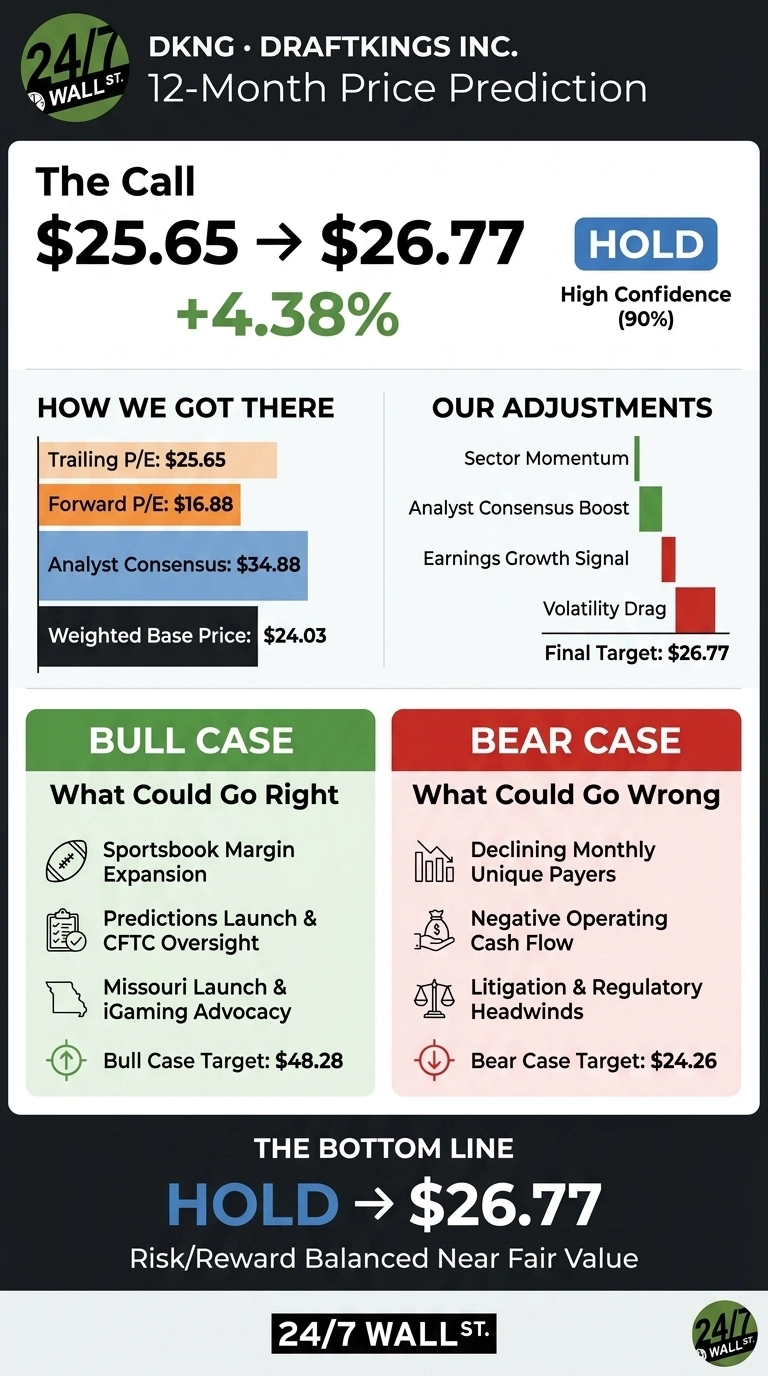

The 24/7 Wall St. price target for DraftKings is $26.77 over the next 12 months, implying 4.38% upside from $25.65. Our recommendation is hold, with a confidence level of 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $25.65 |

| 24/7 Wall St. Price Target | $26.77 |

| Upside | 4.38% |

| Recommendation | HOLD |

| Confidence Level | 90% |

A Year of Pain, A Quarter of Hope

DKNG has fallen 36.68% over the past year and 25.57% year-to-date, with the stock sliding 10.91% in just the past week. Shares now sit 28% below their 52-week high of $48.78, though comfortably above the low of $20.46.

The Q1 2026 earnings report was a genuine bright spot. Revenue rose 8.83% to $1.65 billion, EPS of $0.20 beat by 16.41%, and Adjusted EBITDA jumped 64% to $167.85 million.

Still, the stock has been weighed down by a class action lawsuit filed April 29, 2026 alleging deceptive interface design, a Federal Reserve study linking sportsbook activity to consumer debt delinquency, and steady insider selling, including 62,500 shares from the Chief Legal Officer on June 11.

Why Bulls See a Breakout Ahead

The bull case rests on three pillars. First, Sportsbook net revenue margin expanded to 7.8% from 6.4%, with average revenue per Monthly Unique Payer up 21% to $131.

Second, the DraftKings Predictions launch under CFTC oversight, paired with the Crypto.com Derivatives partnership, opens a federally regulated event-contract market that could lift the entire valuation framework.

Third, the Missouri mobile launch and iGaming advocacy spend offer state-level optionality.

Morningstar has reiterated bullish commentary on the prediction-market expansion, and the consensus analyst target of $34.88 implies meaningful upside if execution holds. Our internal bull-case path projects DKNG reaching $48.28 within twelve months, a 88.23% total return.

The Risks Worth Watching

Bears point to a 4% YoY decline in Monthly Unique Payers to 4.2 million, negative Q1 operating cash flow of $48.4 million, and stock-based compensation of $65.2 million. State tax hikes in New Jersey, Louisiana, and Illinois compress structural margins.

To be fair, the cash-flow softness reflects $26.4 million in legalization advocacy and aggressive Predictions investment, both of which management frames as growth capex rather than recurring drag.

Litigation is the bigger swing factor. The PHAI product-liability suit and a Fed paper tying betting to delinquencies could pressure multiple expansion. Average analyst targets have already drifted from $44.58 to $38.80. Our bear-case scenario lands at $24.26 over twelve months.

DraftKings Price Prediction 2026-2030

The 24/7 Wall St. price target of $26.77 sits just above the current quote, and our hold rating carries 90% confidence. The constructive scenario hinges on MUP stabilization in Q2 and meaningful Predictions volume by year-end.

The cautious scenario is one where litigation expands or state tax increases spread further. The setup is balanced, and patience is the right posture.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $26.77 |

| 2027 | $27.08 |

| 2028 | $27.21 |

| 2029 | $29.53 |

| 2030 | $31.70 |

These projections assume DraftKings continues scaling Sportsbook margins and successfully establishes a defensible Predictions footprint. Significant upside or downside could result from federal prediction-market rulings, state iGaming legalization waves, or escalating product-liability litigation.

Contact [email protected] for any questions or corrections.