Alphabet (NASDAQ:GOOG | GOOG Price Prediction) has gone from AI laggard to AI leader in roughly twelve months, and the market is finally paying attention. Yet at $371.10, the stock still trades at a fraction of the multiple investors hand to other Magnificent Seven names. That gap is the foundation of our call.

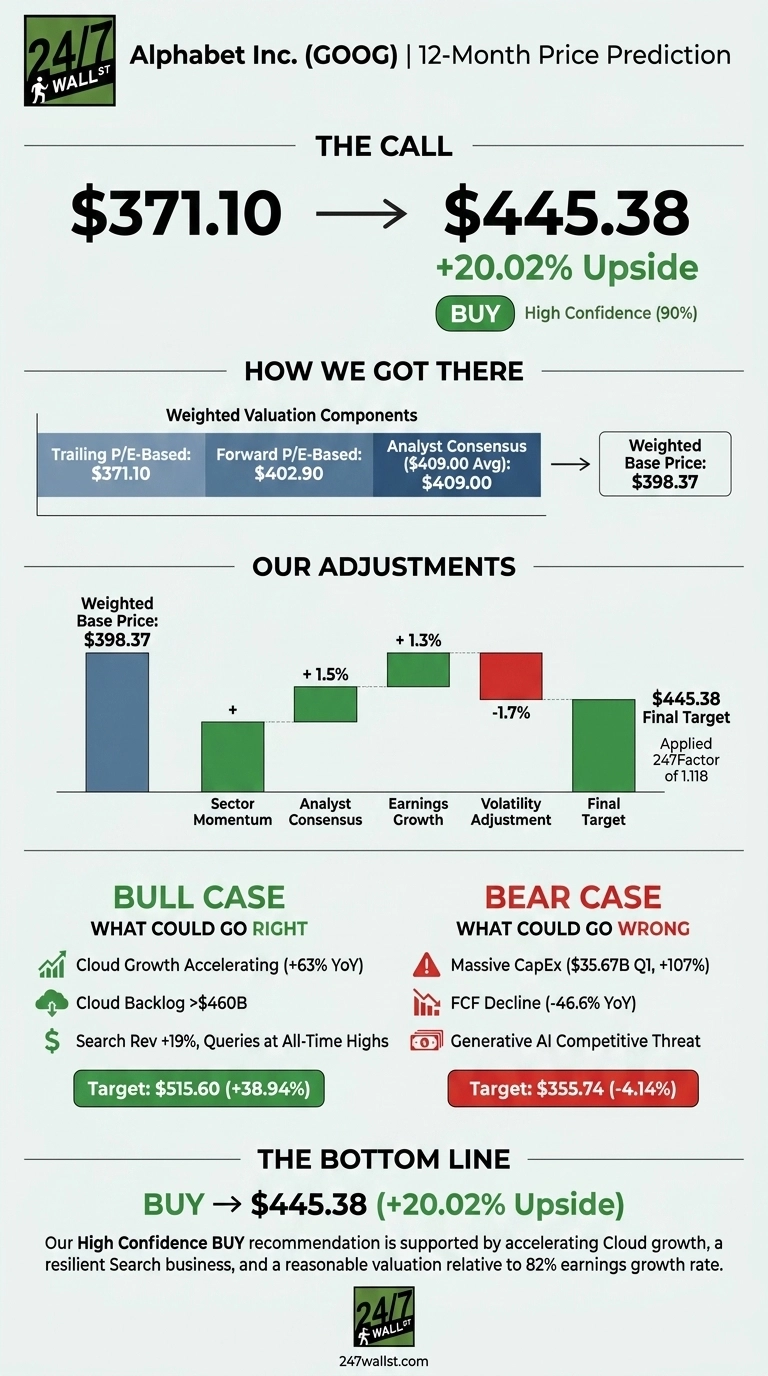

Alphabet screens as one of the cleanest large-cap AI setups in the market today. Our 24/7 Wall St. price target for Alphabet is $445.38, implying 20.02% upside over the next twelve months.

Our recommendation is buy with a high 90% confidence level, supported by accelerating Cloud growth, a Search business that refuses to break, and a forward P/E of 26 that looks reasonable against an 82% earnings growth rate.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $371.10 |

| 24/7 Wall St. Price Target | $445.38 |

| Upside | 20.02% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $177 to $371: A Year Most Investors Will Not Forget

Alphabet is up 109.15% over the past year and 18.41% year to date, with shares now sitting just 1% below the 52-week high of $404.23.

The catalyst was Q1 2026, reported April 29, 2026, when GOOG delivered $109.90 billion in revenue (up 21.8%) and EPS of $5.11 against a $2.63 estimate. Google Cloud grew 63% to $20.03 billion, with backlog nearly doubling to over $460 billion. A $80 billion equity offering announced June 1-2 drove a brief pullback, leaving shares down 5.59% over the past month.

The Case for $515 and Higher

The bull scenario takes Alphabet to $515.60, a 38.94% annual return. Cloud is the engine. Growth accelerated from 32% to 34% to 48% to 63% across four quarters, and the $460 billion backlog gives years of revenue visibility.

Cloud operating margin already expanded from 17.8% to 32.9%. Search is also accelerating, with AI Overviews driving 19% growth and 58 Buy ratings versus zero Sells. Add 500,000 Waymo rides per week and 350 million paid subscriptions, and the bull case writes itself.

What Could Go Wrong

The bear case puts GOOG at $355.74, a -4.14% twelve-month return. The first risk is capital intensity. Q1 CapEx hit $35.67 billion (up 107.4%), free cash flow fell 46.6%, and 2026 guidance was raised to $180 billion to $190 billion. Bulls would counter that backlog growth more than justifies the spend.

Other risks: regulatory pressure (a $3.5 billion EC fine last fall), generative AI competition from OpenAI and Perplexity, and Google Network revenue declining to $6.97 billion. The counterpoint is that queries hit all-time highs despite AI competition, undermining the disruption thesis.

Alphabet Price Prediction 2026-2030

I am a buyer of Alphabet at $371. The 24/7 Wall St. price target of $445.38 reflects a stock trading at a forward P/E of 26 while delivering 63% Cloud growth and 21.8% top-line growth.

The key factor tipping the scale is the $460 billion Cloud backlog, which de-risks the revenue story for years. I would add aggressively if shares revisit the low $300s on CapEx fears. I would step aside if free cash flow continues to deteriorate without a corresponding acceleration in Cloud or Search monetization.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $445 |

| 2027 | $495 |

| 2028 | $545 |

| 2029 | $595 |

| 2030 | $649 |

These projections assume Alphabet continues converting Cloud backlog into reported revenue while protecting Search economics. Meaningful upside or downside could come from a regulatory breakup outcome, a Waymo IPO, or a step-change in agentic commerce monetization through the new Universal Commerce Protocol.

Contact [email protected] for any questions or corrections.