Alphabet (NASDAQ:GOOGL | GOOGL Price Prediction) has been one of the loudest AI winners of the past 12 months, but a sharp June pullback has reset the setup heading into the second half of 2026.

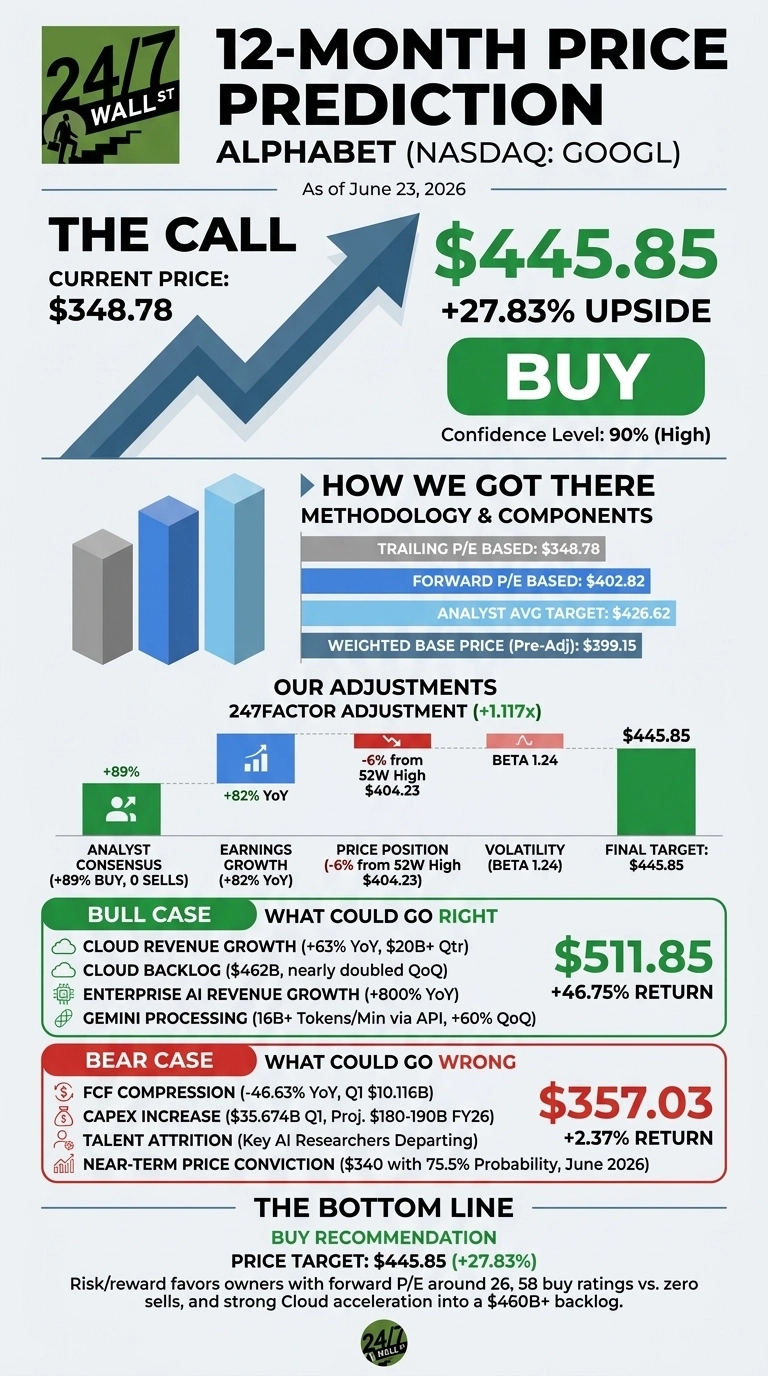

Our 24/7 Wall St. price target for Alphabet is $445.85, implying 27.83% upside from the current $348.78. Confidence is high at 90%, and the recommendation is buy.

| Metric | Value |

|---|---|

| Current Price | $348.78 |

| 24/7 Wall St. Price Target | $445.85 |

| Upside | 27.83% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Pullback Inside a Massive Rally

Alphabet is down 4.99% over the past week and 8.01% over the past month, but the stock is still up 11.29% year to date and 108.54% over the past year.

The recent slide is tied to news that two senior Gemini researchers, including co-lead Noam Shazeer, are leaving for OpenAI and Anthropic, a story that dominated r/stocks over the weekend before retail sentiment rebounded to 62 (bullish) on Monday.

The fundamentals behind the rally are intact. Q1 FY26 delivered EPS of $5.11 against a $2.632 estimate, a 94.1% beat, on revenue of $109.89 billion, up 21.79% YoY. Google Cloud crossed $20 billion in quarterly revenue for the first time, growing 63% with backlog nearly doubling sequentially to $462 billion.

Why Bulls See a Breakout Ahead

The bull case rests on AI monetization compounding faster than expected. Gemini is now processing more than 16 billion tokens per minute via direct API, a 60% sequential jump.

Cloud operating income tripled YoY to $6.6 billion at a 32.9% margin, and enterprise AI revenue grew 800% YoY. Sundar Pichai noted that “our cloud revenue would have been higher if you were able to meet the demand,” a constraint that resolves as 2026 CapEx of $180-190 billion hits the ground.

Search is also expanding monetizable surface area. More than 30% of search advertisers now use AI MAX or Performance Max, and Philipp Schindler argued “there is upside in that coverage number” beyond the historical 20%. If the 247Factor’s bull scenario plays out, the stock reaches $511.85, a 46.75% return.

The Risks Worth Watching

Free cash flow fell 46.63% YoY in Q1 as CapEx more than doubled to $35.674 billion, and management has signaled 2027 spending will “significantly increase”. Bulls would argue this is exactly the kind of build-out that delivered the $462 billion Cloud backlog, but the FCF compression is real.

Add talent attrition at Gemini, ongoing EU competition fines, and Polymarket’s near-term clustering at $340 (75.5% probability) for end-of-June, and the path higher will be choppy. The bear scenario lands at $357.03, essentially flat from here.

Alphabet Price Prediction 2026-2030

The 24/7 Wall St. price target is $445.85, the recommendation is buy, and confidence is 90%. With a forward P/E around 26, 58 buy ratings versus zero sells, and Cloud accelerating into a $460B+ backlog, the risk/reward favors owners.

The bull thesis holds for investors comfortable sitting through CapEx-driven FCF noise. The bear thesis gains traction if the Gemini talent exits signal a deeper competitive crack rather than a normal mega-cap shuffle.

Looking further ahead, here is where our model projects Alphabet could trade, assuming current growth and AI monetization hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $445.85 |

| 2027 | $515 |

| 2028 | $590 |

| 2029 | $650 |

| 2030 | $711.11 |

These projections assume Alphabet continues converting its AI lead into Cloud and Search revenue. Significant upside could come from TPU hardware sales scaling in 2027, while a regulatory forced breakup remains the largest single downside risk.

Contact [email protected] for any questions or corrections.