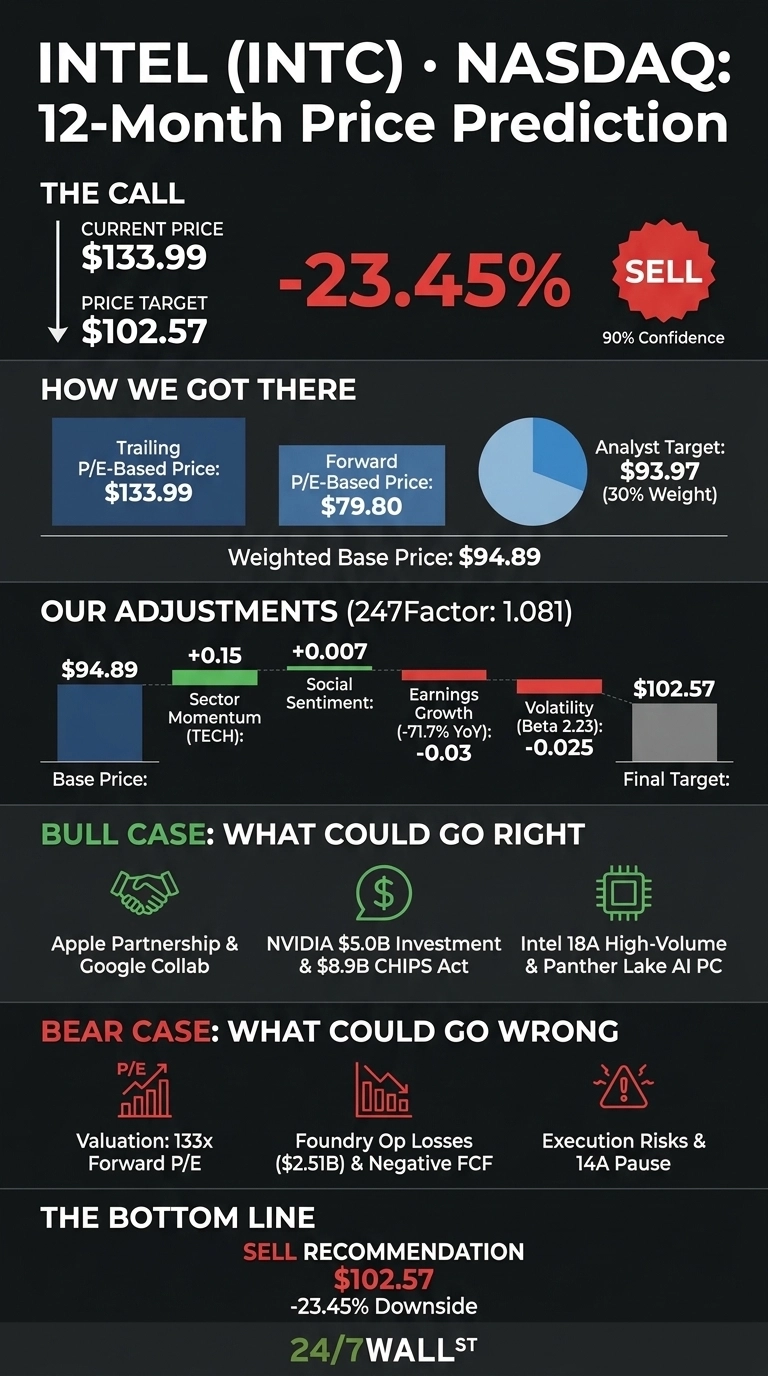

Intel (NASDAQ:INTC | INTC Price Prediction) has been one of the most explosive turnaround stories of 2026, with shares up 263.12% year to date through June 18. After a 12% single-day surge on news of an Apple (NASDAQ:AAPL) manufacturing partnership, the chipmaker trades at $133.99.

Our 24/7 Wall St. price target for Intel is $102.57, implying a 12-month return of -23.45%. The model rates the stock a sell at current levels with 90% confidence.

| Metric | Value |

|---|---|

| Current Price | $133.99 |

| 24/7 Wall St. Price Target | $102.57 |

| Upside/Downside | -23.45% |

| Model Rating | SELL |

| Confidence | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target sits well below current levels. The Apple foundry deal, the 10% U.S. government stake, and a confirmed role producing host CPUs for NVIDIA (NASDAQ:NVDA)’s DGX Rubin NVL8 systems carry potential to push earnings well above our model. A full bull case appears below.

A 523% Rally Reset the Setup

Intel gained 523.5% over the past year and 20.93% in the past month. Trump’s June 18 announcement that Apple would partner with Intel on U.S. chip production sent shares up 10.64% in one session.

Q1 2026 non-GAAP EPS came in at $0.29 against $0.0127 consensus, revenue grew 7.18% to $13.577 billion, and Data Center and AI revenue jumped 22%. CEO Lip-Bu Tan flagged a “sixth consecutive quarter of revenue above our expectations.”

The Case for $150+

If the bull case plays out, Intel’s foundry strategy resembles a second TSMC. The Apple partnership, the multiyear Google (NASDAQ:GOOGL) collaboration on custom ASIC IPUs, and the $5 billion NVIDIA equity investment represent the external customer flywheel Tan has promised.

Combined with $8.9 billion in CHIPS Act funding, Intel 18A entering high-volume manufacturing, and a Panther Lake AI PC platform spanning 200-plus OEM designs, the foundry segment could swing from a $2.51 billion quarterly operating loss to breakeven faster than consensus. Forward EPS could reset toward $1.50, and a 100x multiple gets Intel to $150.

Where the Math Breaks

The bear case rests on valuation. Intel trades at a forward P/E of 133x against TTM EPS of -$0.60. The Q1 GAAP net loss of $3.728 billion reflected a $4.07 billion Mobileye goodwill impairment, so the underlying business is operationally profitable, with non-GAAP gross margin reaching 41.0%. F

ree cash flow remains weak at -$3.867 billion on $4.963 billion in capex. If foundry losses persist or Intel 14A pauses on weak customer commitments, shares could fall to $76.56.

Intel Price Prediction 2026-2030

The 24/7 Wall St. price target stays at $102.57 with 90% model confidence. Forward earnings of $0.60 cannot support a $134 share price under any reasonable multiple.

Revisit the bull case if Intel signs a second flagship foundry customer and forward EPS estimates rise above $1.20. The setup weakens if foundry losses widen or 2026 free cash flow remains negative through year-end.

Our model projects Intel could trade at these levels, assuming current growth trajectories and foundry ramp progress on schedule.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 (year-end) | $119.17 |

| 2027 | $102.57 |

| 2028 | $96.00 |

| 2029 | $90.00 |

| 2030 | $87.00 |

These projections assume Intel executes on its foundry strategy. Significant upside could come from sustained external customer wins, while a 14A pause or prolonged free cash flow burn would skew toward our $62.81 five-year bear case.