Procter & Gamble (NYSE:PG | PG Price Prediction) and Colgate-Palmolive (NYSE:CL) both just reported, and the earnings reports sharpened a debate dividend investors have been having for years.

P&G posted its fiscal Q3 2026 with core EPS of $1.59 on net sales of $21.235 billion. Colgate followed with Q1 2026 adjusted EPS of $0.97 on revenue of $5.324 billion. Both lean on staples brands. Only one runs the bigger dividend machine.

Tide and Pampers Carry P&G. Hill’s and Latin America Carry Colgate.

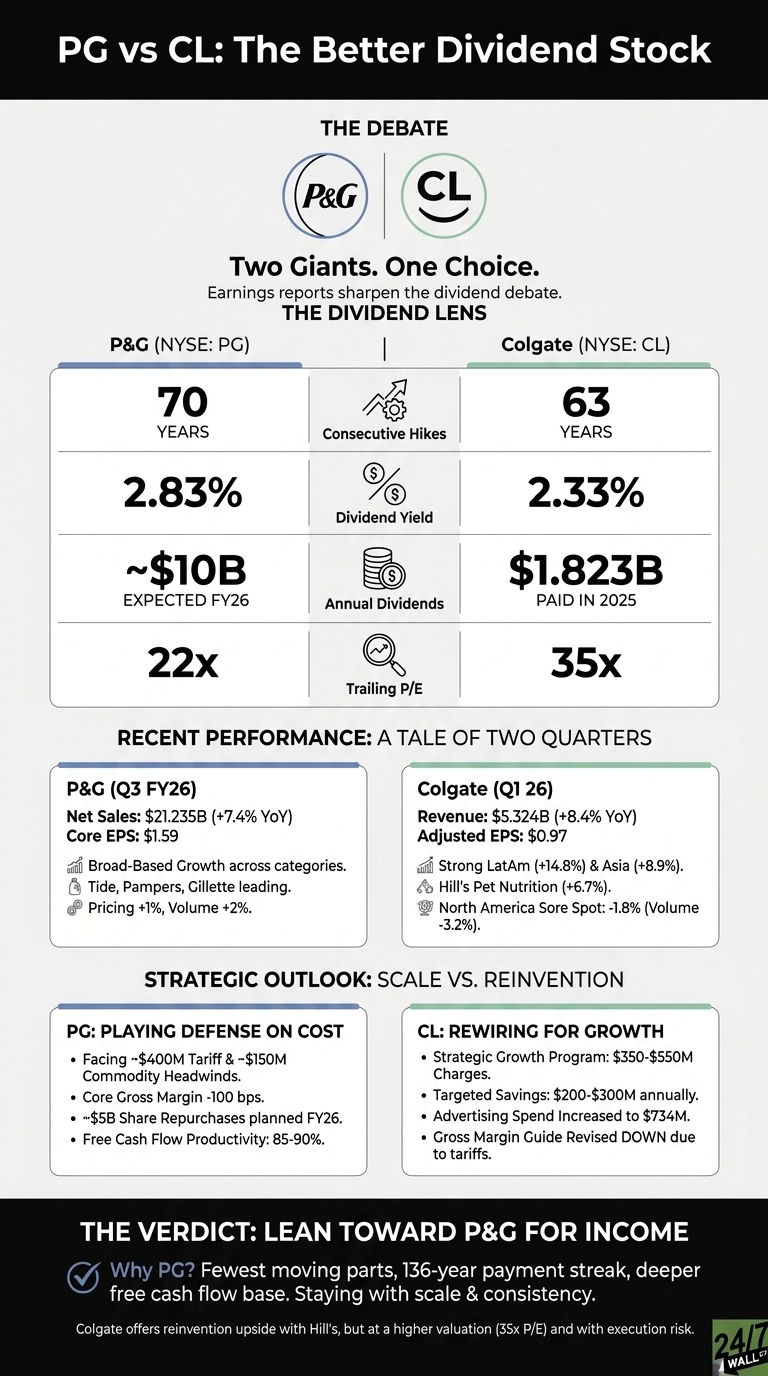

P&G’s quarter looked broad. Beauty grew 11% reported, Grooming added 7%, and Fabric & Home Care delivered $7.403 billion in sales. CEO Shailesh Jejurikar called it “a solid acceleration in top-line results… with broad-based growth across product categories and regions.”

Tide, Pampers, and Gillette did the heavy lifting, and pricing only contributed one point of organic growth, which tells me volume is finally pulling its weight again.

| Dividend Lens | P&G | Colgate |

| Consecutive annual hikes | 70 | 63 |

| Indicated yield | 2.83% | 2.33% |

| FY dividends to shareholders | ~$10B expected FY26 | $1.823B paid in 2025 |

| Trailing P/E | 22x | 35x |

Colgate’s mix was lumpier. Oral, Personal and Home Care rose 8.9% to $4.131 billion, and Hill’s Pet Nutrition added $1.194 billion. Latin America organic sales jumped 5.4% and Asia Pacific led at 5.6%.

North America was the sore spot, down 1.8% with volume off 3.2%. Noel Wallace leaned on resilience language, noting the team is “able to execute against our long-term strategy while delivering strong results in a difficult operating environment.”

Scale Versus Reinvention

P&G is playing defense on cost. Management flagged roughly $400 million in after-tax tariff drag plus $150 million in commodity headwinds, and core gross margin slipped 100 basis points. The buyback is still real, with over $600 million repurchased in Q3 and roughly $5 billion planned for FY26. Free cash flow productivity sits in the 85% to 90% range.

Colgate is rewiring itself. The expanded Strategic Growth and Productivity Program now carries pretax charges of $350 million to $550 million with targeted annual savings of $200 million to $300 million.

Gross margin guidance was revised lower because of tariffs, while advertising rose to $734 million from $668 million. The most recent dividend ticked up to $0.53 per share. Growth is real, but the restructuring bill is climbing.

The Next Test Is Margin Recovery

I want to see whether P&G can hold its $6.83 to $7.09 core EPS guide as tariffs bite. Colgate needs a North America turn, where Speed Stick, Tom’s of Maine, and the core Colgate brand have been ceding shelf to private label. Hill’s matters too. Pet food is still the cleanest growth lane in this comparison, and any volume slowdown would dent the bullish case.

Why I Lean Toward P&G for the Income Sleeve

If you want a dividend with the fewest moving parts, I would lean toward P&G. The 136-year payment streak, deeper free cash flow, and a 10-year total price return of 141.11% all argue for staying with scale.

Colgate is the more interesting setup if you believe the SGPP cuts work and Hill’s keeps compounding. At 35x trailing earnings, though, the stock is paying you the lower yield for the harder turnaround. For me, the better dividend stock right now is P&G, and I would only switch if Colgate’s North America volumes inflected positively for two straight quarters.

Contact [email protected] for any questions or corrections.