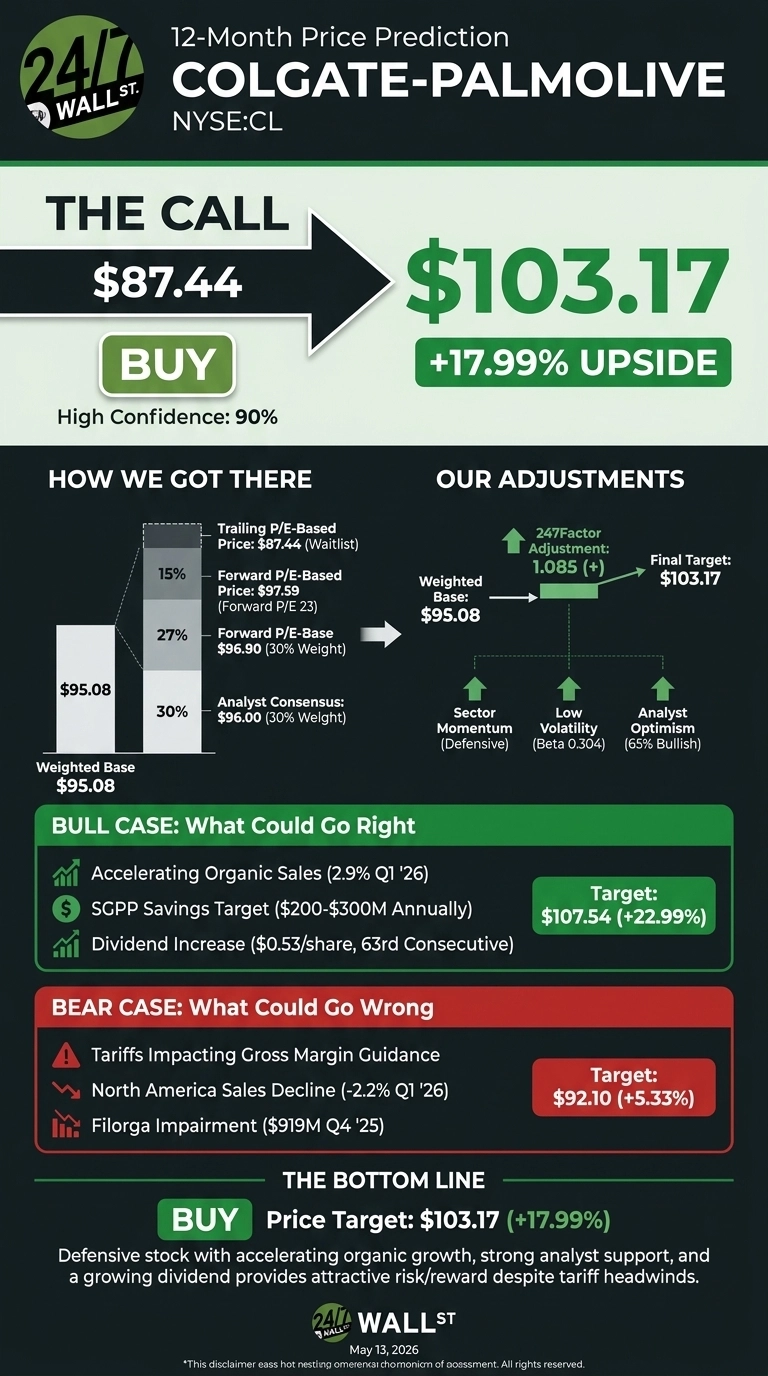

Colgate-Palmolive (NYSE:CL | CL Price Prediction) is exactly the kind of name investors hunt for when the macro picture gets murky. Low beta, a 63-year dividend streak, and a portfolio of brands that sell whether the economy expands or contracts. With shares at $87.44 and tariffs creating fresh margin pressure, the question is whether the defensive premium is already in the price.

Our 24/7 Wall St. price target for Colgate-Palmolive is $103.17 over the next 12 months, implying 17.99% upside. We rate the stock a buy with 90% confidence.

| Metric | Value |

|---|---|

| Current Price | $87.44 |

| 24/7 Wall St. Price Target | $103.17 |

| Upside | 17.99% |

| Recommendation | BUY |

| Confidence Level | 90% |

The Recovery From the October Lows

Colgate has been a quiet winner in 2026. The stock is up 12.04% year to date and 4.33% over the past month, recovering from an October 2025 low of $77.63. Shares sit roughly 3% below the 52-week high of $98.72.

The May 1 Q1 2026 earnings report reinforced the defensive thesis. Colgate reported adjusted EPS of $0.97 versus the $0.9445 consensus, extending the beat streak to four straight quarters. Revenue of $5.324 billion grew 8.4% YoY, with Latin America up 14.8% and Europe up 11.9%. North America declined -1.8%. Free cash flow jumped 27.94% to $609 million.

Why Bulls See a Breakout to $107

The bull case rests on three pillars. First, organic sales growth is accelerating: from 0.4% in Q3 2025 to 2.9% in Q1 2026, with emerging markets organic sales up 6.2%.

Second, the expanded SGPP restructuring program targets $200-$300 million in annual pretax savings, which could fund advertising and margin recovery once tariff headwinds ease.

Third, the dividend stepped up to $0.53 per quarter, the 63rd consecutive annual increase.

Wall Street consensus sits at $96.00 with 13 buy or strong buy ratings and zero sells. Our bull-case scenario lands at $107.54, a 22.99% total return.

What Could Go Wrong

The bear case starts with tariffs. Management revised 2026 GAAP gross margin guidance from up to down, citing the evolving tariff environment. North America organic sales declined 2.2% in Q1, and the Filorga skin health business triggered a $919 million goodwill impairment in Q4 2025 tied to China weakness. A trailing P/E of 34 leaves little room for execution slippage.

Bulls counter that the trailing multiple is distorted by the Filorga charge. Forward P/E of 23 tells a different story, and operating cash flow grew 24.5% in Q1. Our bear case still delivers $92.10, a 5.33% return, which underscores the downside protection a 0.3 beta provides.

The Setup From Here

Our 24/7 Wall St. price target of $103.17 and buy rating reflect a stock that earns its defensive label. The tipping factor is accelerating organic growth and a bear-case floor that still pays. The setup favors low-volatility compounding with a growing dividend. Key risks to monitor include tariff escalation broadening beyond consumer staples and further deterioration in North America volumes.

Here is where the model projects Colgate could trade, assuming current growth and margin trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $103.17 |

| 2027 | $114.00 |

| 2028 | $124.50 |

| 2029 | $135.50 |

| 2030 | $146.79 |

These projections assume Colgate executes on its 2030 strategy and SGPP savings reach the high end of guidance. Significant upside or downside could result from tariff resolution, faster pet nutrition growth via Prime100, or a deeper China skin-health reset.

Contact [email protected] for any questions or corrections.