The biggest story in AI this week is a personnel move. Noam Shazeer, Google DeepMind’s VP of Engineering and a Gemini co-lead, is leaving for OpenAI in what the hosts of the TBPN podcast called “the most significant AI talent move of the year.” The day after, policy expert Dean Ball followed him to OpenAI. The question now circulating among investors: does this justify selling Alphabet (NASDAQ:GOOGL | GOOGL Price Prediction) stock?

The short answer, grounded in the data: probably not.

Why Shazeer Leaving Matters

TBPN host John Coogan described Shazeer as a “co-author of Transformer, T5, Switch Transformer papers” and one of the pioneers of sparse mixture-of-experts models. A guest on the show said the departure “makes you wonder what’s going on at Google.” On Ball, the same guest said “The main thing is he really cares about getting this right as a country” and noted Ball has been “critical of almost every company in the space.” Even Jim Cramer weighed in around 3:00 AM, referring to OpenAI simply as “AI,” a shorthand the hosts found notable.

The substantive risk is narrative and retention. If a researcher of Shazeer’s stature walks, others may follow. That is a real consideration for any forward thesis on Google DeepMind’s competitive position against OpenAI.

What the Fundamentals Actually Say

Alphabet’s most recent quarter does not look like a company losing the AI race. In Q1 FY2026, Alphabet posted EPS of $13.10 (TTM) and revenue of $422.5 billion (TTM), with quarterly revenue growth of 21.8% YoY and earnings growth of 82% YoY. Google Cloud revenue grew 63% YoY to $20.03B, with backlog nearly doubling to over $460B. CEO Sundar Pichai noted that Gemini API usage was processing more than 16 billion tokens per minute, up 60% sequentially, with Gemini Enterprise growing paid monthly active users 40% quarter over quarter. The full Q1 release is available via the SEC filing and on Alphabet’s investor relations page.

Operating margin came in at 36.1%, return on equity at 38.9%, and Waymo crossed 500,000 fully autonomous rides per week.

Valuation and Sentiment

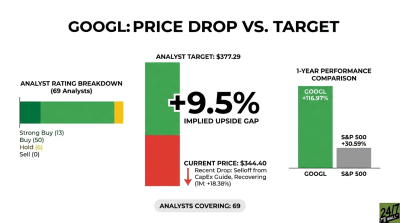

GOOGL trades around $368.03, up 17.73% year to date and 112.95% over the past year. Forward P/E sits at 26, with a trailing P/E of 28. Analyst consensus skews heavily bullish: 14 strong buy, 43 buy, 7 hold, and zero sell ratings, with a consensus target of $432.83. Our internal model puts the 1-year target near $450, implying roughly +22% upside.

Reddit sentiment confirms the lack of panic. Across the news cycle this week, scores held in the 60 to 78 range, predominantly bullish. The popular thread “Is the market underpricing GOOGL search again?” suggests retail is treating the Shazeer headline as a discussion point worth debating. Prediction markets concur: traders price an 80% probability of GOOGL closing above $350 by month end.

The Microsoft Angle

For investors who want indirect exposure to OpenAI’s talent gains, Microsoft (NASDAQ:MSFT) is the public proxy through its restructured partnership. Microsoft’s AI business reached a $37 billion annual run rate, up 123% YoY, in its most recent quarter. The catch: MSFT trades at $379.40, down 21.2% YTD and 20.36% over one year, as retail flags capital intensity. A trending wallstreetbets post titled “Satya and Zuckerberg are incinerating capital” captures the mood.

The Takeaway

Losing a foundational researcher is a real morale and narrative risk for Alphabet. The talent war is now the central competitive variable in AI. But Cloud growth, search resilience, Gemini adoption, Waymo scale, an unbroken bullish analyst consensus, and a forward multiple of 26 do not align with a panic-sell thesis.

Still, most experts in the field deeply respect Shazeer and believe he was instrumental in Gemini catching up with rivals OpenAI and Anthropic. If Gemini’s benchmarks begin trailing Anthropic and OpenAI, it could be a singal this talent loss was substantial. However, we believe Alphabet’s current valuation is supported by continued strength in search, sharge gains at Google Cloud, and the continuing value of YouTube in the video space.

Contact [email protected] for any questions or corrections.