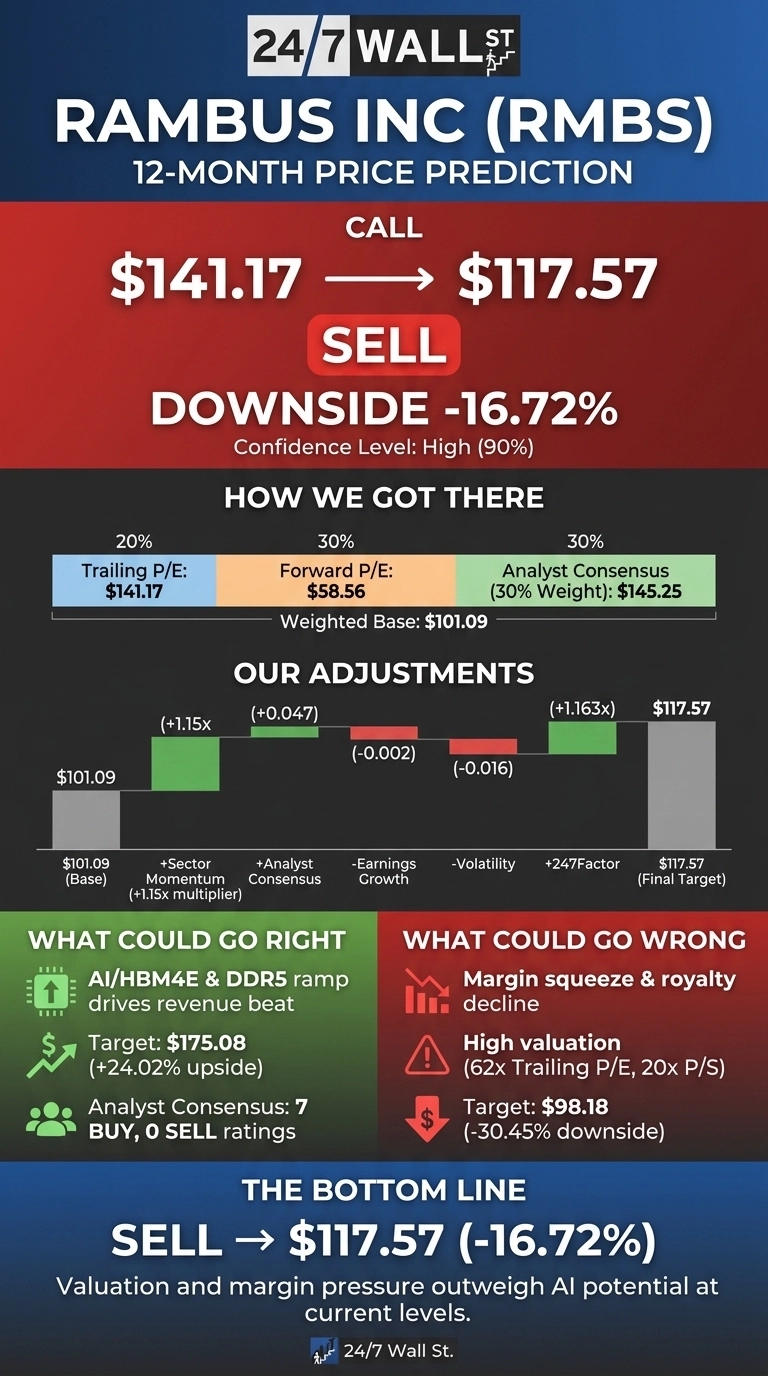

After a rally that has lifted Rambus (NASDAQ:RMBS | RMBS Price Prediction) 133.15% over the past year, the memory interface IP leader trades at $141.17. Our 24/7 Wall St. price target for Rambus is $117.57 over the next 12 months, implying 16.72% downside from current levels.

Our recommendation is sell, with high confidence at 90%. The shares are pricing in flawless execution against a backdrop of tightening DRAM supply and compressing margins.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $141.17 |

| 24/7 Wall St. Price Target | $117.57 |

| Upside/Downside | -16.72% |

| Recommendation | SELL |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target of $117.57 sits below where Rambus trades today, and the bull case is real. The HBM4E memory controller IP ramp and the AI inference data center cycle could push product revenue meaningfully above guidance.

Wall Street analysts carry a consensus target of $145.25 with 7 buy ratings and zero sells. Treat our target as one datapoint among many.

A Year-Long Rally Meets a Margin Squeeze

RMBS is up 53.63% year to date and 15.68% over the past month, though it pulled back 2.28% last week and sits 17% from its 52-week high of $174.10.

Q1 2026 revenue of $180.19 million beat slightly, but non-GAAP EPS of $0.63 missed the $0.6363 consensus. Non-GAAP operating margin compressed to 42% from 46%, R&D rose 18%, and royalty revenue declined year over year. An analyst downgrade citing tightening DRAM supply followed the report.

The Case for $175+

Bulls have catalysts. CEO Luc Seraphin said “The growth of AI inference and agentic workloads in the data center continues to drive demand for higher memory bandwidth, efficient data movement, and scalable connectivity.”

DDR5 RCD leadership, the LPDDR5X SOCAMM2 server module chipset, and the industry-fastest HBM4E memory controller IP position Rambus squarely inside the AI capex wave. Q2 2026 guidance calls for revenue of $186 million to $204 million. Our bull-case 12-month scenario reaches $175.08, a 24.02% gain.

The Risks Worth Watching

RMBS trades at 62 trailing earnings and a price-to-sales ratio of 20, leaving little margin for error. Royalty revenue declined to $69.64 million in Q1, the CFO transitioned in Q4 2025, and supply chain disruption was disclosed.

Bulls would counter that R&D spending is the kind of investment that funds the HBM4E and SOCAMM2 ramps, and the balance sheet shows $1.39 billion in equity. Still, our bear case lands at $98.18, a 30.45% decline.

Rambus Price Prediction 2026-2030

The 24/7 Wall St. price target of $117.57 reflects a sell call at 90% confidence. The tipping factor is valuation: a forward multiple of 24 is reasonable, but the stock trades far above that anchor.

The bull thesis strengthens if HBM4E design wins translate into a step-function ramp in product revenue. The bear thesis strengthens if royalty revenue keeps slipping and margins keep compressing. Today, the setup favors patience.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $117.57 |

| 2027 | $115.00 |

| 2028 | $110.50 |

| 2029 | $108.25 |

| 2030 | $107.71 |

These projections assume Rambus continues executing its current DDR5 and HBM roadmap. Significant upside could result from accelerated HBM4E adoption, while downside risk centers on prolonged DRAM supply tightness and royalty erosion.