Seagate Technology (NASDAQ:STX | STX Price Prediction) has delivered one of the market’s most remarkable runs of 2026, with the stock up 297.98% year to date as AI-driven storage demand rewrites the narrative around legacy hard drive makers. After a parabolic move from $274.90 on December 31, 2025 to $1,094.04 on June 22, 2026, the question is how much higher this can go.

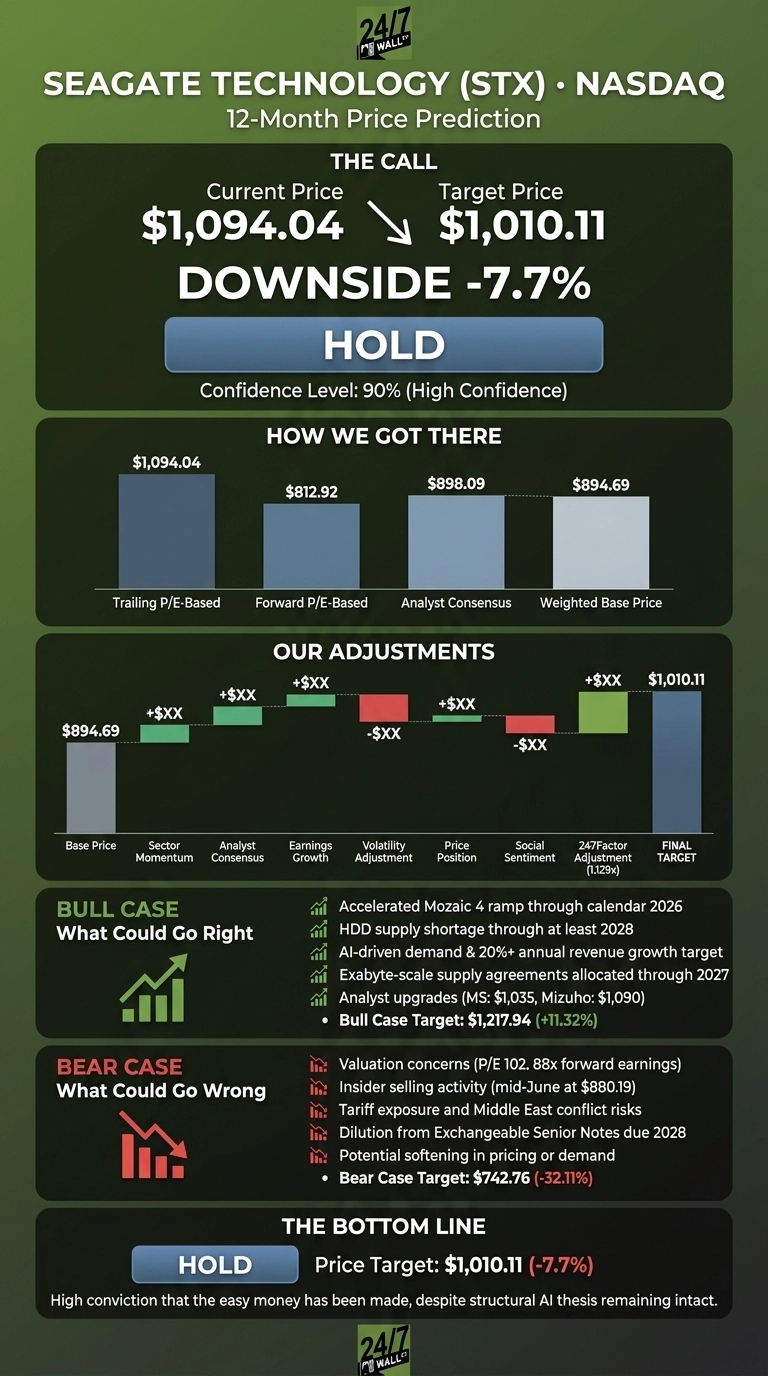

Our 24/7 Wall St. price target for Seagate is $1,010.11 over the next 12 months, implying roughly 7.7% downside from current levels. Our recommendation is hold, with a 90% confidence level, reflecting high conviction in the model output even as fundamentals remain intact.

| Metric | Value |

|---|---|

| Current Price | $1,094.04 |

| 24/7 Wall St. Price Target | $1,010.11 |

| Upside/Downside | -7.7% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target sits below where Seagate trades today. STX is one of the most dynamic AI infrastructure stories in the market, and real upside could come from accelerated Mozaic 4 ramp through calendar 2026 or from HDD pricing power lasting deeper into 2028 than the model assumes. The bull case below explains why Seagate could keep rallying past our number.

From $131 to $1,094 in 12 Months

Seagate has gained 746% over the past year and 34.61% in the past month alone.

The catalyst was Q3 FY26 earnings on April 28, 2026, where Seagate posted adjusted EPS of $4.10 versus $3.50 expected on revenue of $3.11 billion, up 44.07% year over year. Non-GAAP gross margin expanded to 47.0% from 36.2%, and free cash flow reached $953 million. Management guided Q4 to $3.45 billion in revenue and $5.00 EPS, fueling the move.

The Case for $1,200+

Bulls have real ammunition. Morgan Stanley raised its target to $1,035 from $767 citing HDD shortages through at least 2028. Mizuho raised its target to $1,090 from $875, JPMorgan to $920, and Wells Fargo to $900.

CEO Dave Mosley said Seagate has “exabyte-scale supply agreements in place with nearly all major cloud and hyperscale customers, with nearline capacity almost fully allocated through calendar 2027”, and management raised its annual revenue growth target to a minimum of 20% over the next few years. Our bull case scenario points to $1,217.94, an 11.32% return.

What Could Go Wrong

The risk centers on valuation. STX trades at a P/E of 102 and roughly 88x forward earnings, well above the $898.09 analyst consensus target.

Insiders, including CFO Gianluca Romano and CEO Dave Mosley, sold shares in mid-June at $880.19, though bulls note these were pre-planned 10b5-1 transactions and Mosley still holds over 327,000 shares. Other risks include tariff exposure, Middle East conflict, and dilution from Exchangeable Senior Notes due 2028. Our bear case lands at $742.76, a 32.11% drawdown.

Seagate Price Prediction 2026-2030

A pullback to the $850 to $900 range would look more attractive on a risk/reward basis if HAMR qualification with remaining hyperscalers closes on schedule. The setup looks less compelling if Q4 results show softening in pricing or if exabyte shipments miss the mid-20% growth bar.

My 24/7 Wall St. price target of $1,010.11 and hold rating reflect high confidence that the easy money has been made, even though the structural AI thesis remains intact.

Here is where our model projects Seagate could trade, assuming current growth trajectories and pricing discipline hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,010 |

| 2027 | $1,045 |

| 2028 | $1,080 |

| 2029 | $1,055 |

| 2030 | $1,044 |

These projections assume Seagate executes the Mozaic roadmap and captures share of AI storage spend. Significant upside or downside could result from HAMR adoption pace, hyperscaler capex cycles, or competitive pressure from NAND on the storage tier.

Contact [email protected] for any questions or corrections.