NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) and Micron Technology (NASDAQ:MU) both posted blockbuster AI infrastructure quarters, but the market reacted in opposite directions. NVIDIA sells the compute. Micron sells the memory that keeps those GPUs fed.

Comparing them now makes sense because each just told investors something different about where AI hardware spending actually lands in 2026.

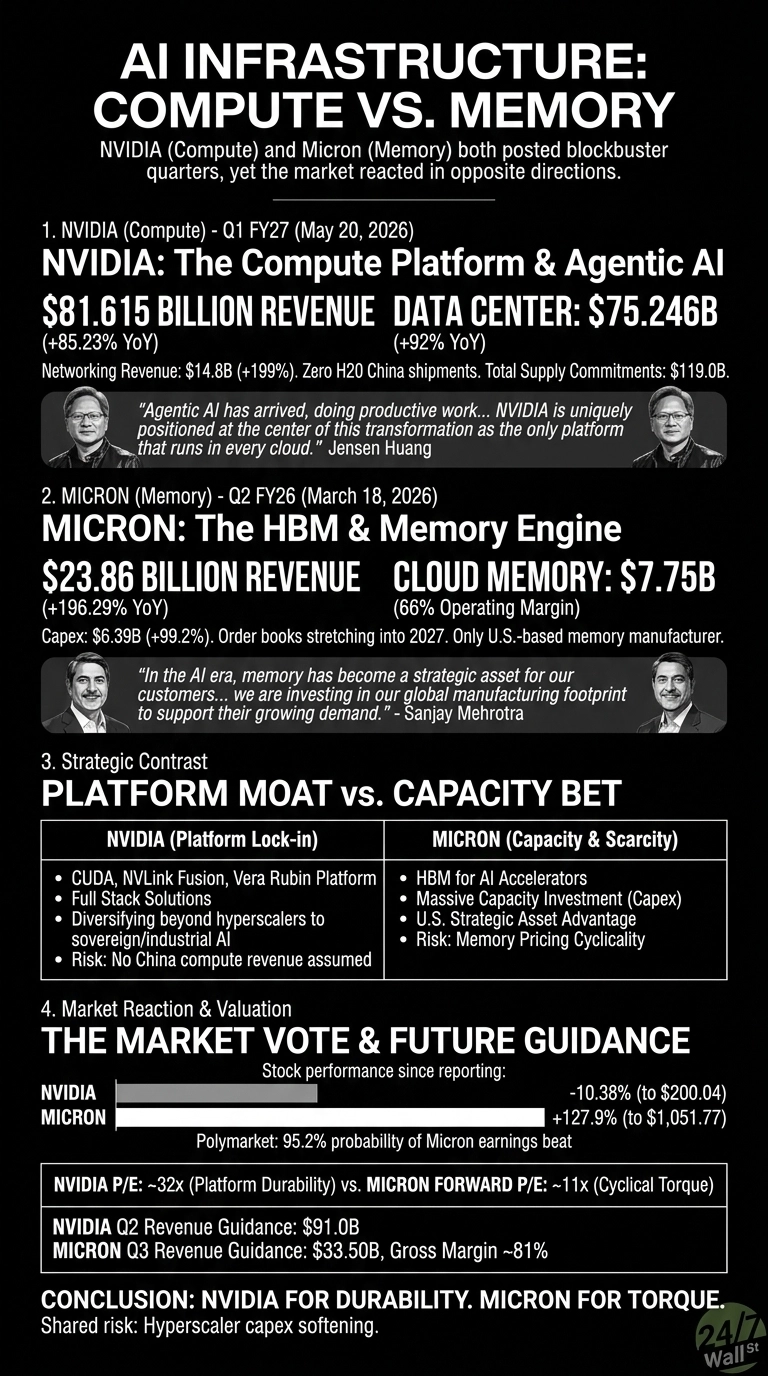

Blackwell Carries NVIDIA. HBM Carries Micron.

NVIDIA’s Q1 FY27 report on May 20, 2026 showed revenue of $81.615 billion, up 85.23% year over year, with Data Center alone at $75.246 billion. Networking inside that segment grew 199%, a number that says NVLink and Spectrum-X are pulling weight, not just GPUs. Non-GAAP EPS landed at $1.87.

Jensen Huang framed the moment bluntly: “The buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.”

Micron’s Q2 FY26 earnings report on March 18, 2026 told a wilder cyclical story. Revenue hit $23.86 billion, up 196.29%, with non-GAAP EPS of $12.20 against a $8.73 estimate. Cloud Memory revenue alone reached $7.75 billion at a 66% operating margin.

CEO Sanjay Mehrotra said memory has become “a strategic asset” for hyperscale customers, and the board approved a 30% dividend hike to back that view.

Platform Moat vs. Capacity Bet

NVIDIA leans on CUDA, NVLink Fusion, and the announced Vera Rubin platform to lock customers into a full stack. Roughly half of Data Center revenue still comes from hyperscalers, and management is pushing into sovereign and industrial AI to diversify. The catch is China: zero H20 Data Center shipments this quarter, and forward guidance assumes that stays at zero.

| Business Driver | NVIDIA | Micron |

| Main growth engine | Blackwell GPUs, NVLink networking | HBM and DRAM for AI accelerators |

| Guidance | $91.0B Q2 revenue | $33.50B Q3 revenue |

| Gross margin | 75.0% non-GAAP | 74.4% GAAP, guiding to ~81% |

Micron’s bet is physical. Capex of $6.39 billion in a single quarter funds HBM capacity that order books reportedly stretch into 2027. Being the only U.S.-based memory manufacturer matters for sovereign AI buyers, and a forward P/E of 11 suggests the market still treats this as cyclical. NVIDIA’s P/E sits near 32, which is hardly cheap but reflects platform durability.

The Market Already Voted Differently

Since reporting, NVIDIA shares are down 10.38% to $200.04. Micron is up 127.9% to $1,051.77, although it dropped 13.18% on June 23 ahead of its next earnings report.

Polymarket traders give Micron a 95.2% probability of beating quarterly earnings, while NVDA’s near-term crowd consensus clusters at $195 to $210. I will be watching whether Micron’s gross margin actually reaches the guided 81% and whether NVIDIA’s $119 billion in supply commitments converts cleanly.

NVIDIA for Durability, Micron for Torque

For investors researching AI exposure that survives a memory price reset, NVIDIA’s profile stands out. The software moat and networking growth give the platform a second leg the bears keep underrating, even with China at zero.

For investors comfortable with cyclicality, Micron offers more torque, because HBM scarcity is real and the forward multiple still leaves room. The shared risk on both theses is a softening in hyperscaler capex guidance later this year, the one variable that pressures both stories at once.