NVIDIA (NASDAQ: NVDA | NVDA Price Prediction) and SanDisk (NASDAQ: SNDK) both delivered blowout AI infrastructure quarters. NVIDIA sells the compute and networking silicon that trains frontier models. SanDisk sells the NAND flash that feeds those models data.

One is the diversified platform king. The other is a freshly independent memory pure play riding a shortage cycle.

Data Center Compute Carries One. NAND Pricing Carries the Other.

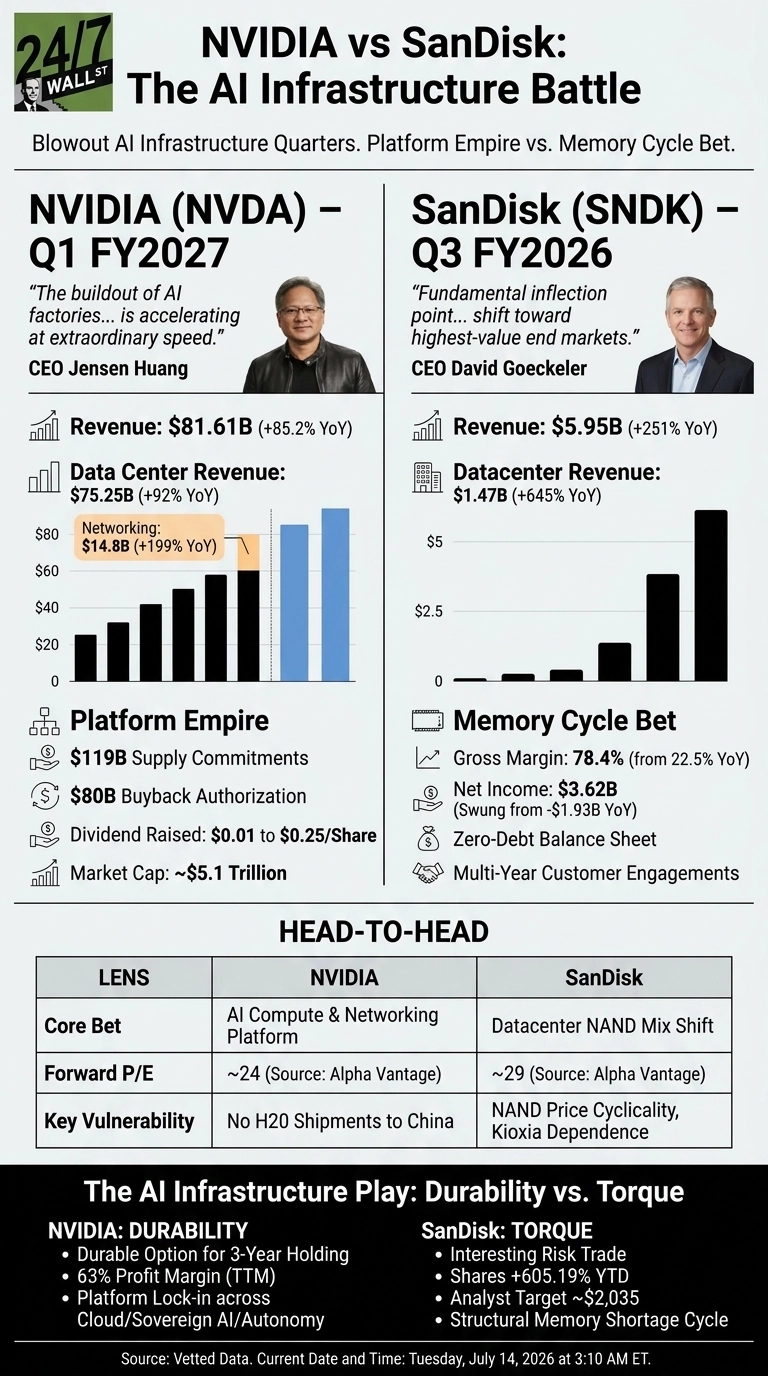

NVIDIA’s Q1 FY2027 print was a Data Center story. Revenue hit $81.615 billion, up 85.23% YoY, with Data Center alone contributing $75.246 billion (+92% YoY). Networking was the sleeper hit at $14.8 billion (+199% YoY), driven by InfiniBand, Spectrum-X, and NVLink.

Jensen Huang framed the moment bluntly: “The buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.” Non-GAAP EPS of $1.87 beat expectations.

SanDisk’s Q3 FY2026 was a different shock. Revenue of $5.95 billion came in 251% higher YoY, and EPS of $23.41 handily beat the $14.66 consensus. Gross margin swung from 22.5% to 78.4% in a year, largely on NAND pricing.

Datacenter revenue rocketed 645% YoY to $1.47 billion. CEO David Goeckeler called it “a fundamental inflection point” for the company’s mix shift toward Datacenter.

Platform Empire vs. Memory Cycle Bet

NVIDIA is spending like a company that already won, with $119 billion in supply commitments, an $80 billion buyback authorization, and a dividend hike from $0.01 to $0.25 per share. Its next act (Vera Rubin, Blackwell 300, DRIVE Hyperion with Hyundai, Kia, and Uber) reads like a diversified portfolio.

| Lens | NVIDIA | SanDisk |

| Core Bet | AI compute and networking platform | Datacenter NAND mix shift |

| Forward P/E | 24 | 29 |

| Key Vulnerability | No H20 shipments to China | NAND price cyclicality, Kioxia dependence |

SanDisk is playing a narrower hand. Goeckeler is anchoring the business to multi-year customer engagements backed by firm financial commitments, with five NBM agreements signed between Q3 and Q4. The zero long-term debt balance sheet after retiring $650 million is impressive, but the model leans on Kioxia manufacturing and structural NAND tightness.

The Next Test Is Whether Storage Keeps Up With Compute

NVIDIA guided Q2 to $91 billion in revenue, which assumes zero China Data Center compute. I will watch whether hyperscaler backlog absorbs that gap cleanly.

SanDisk’s Q4 guide of $7.75 to $8.25 billion in revenue and $30 to $33 EPS is aggressive; the question is how many more NBM contracts close before pricing normalizes. Reddit chatter has flagged put option gains and pullback anxiety around SanDisk after its parabolic run.

Why I Lean NVIDIA for Durability, SanDisk for Torque

For a three-year holding period, NVIDIA looks like the more durable option. The $5.1 trillion market cap and 63% profit margin feel unusual for a company still compounding revenue at 85%, and the platform lock-in across cloud, sovereign AI, and autonomy is hard to disrupt.

SanDisk is the more interesting risk trade. Shares are up 605.19% year to date, and analysts see a target around $2,035, but the thesis rides on a memory shortage analysts do not expect to ease before 2028. For a turnaround-hungry investor, that torque is the appeal. The platform durability argument favors NVIDIA, while SanDisk’s next two quarters warrant close attention before the thesis firms up.

Contact [email protected] for any questions or corrections.