I keep hitting the buy button on Johnson & Johnson (NYSE:JNJ | JNJ Price Prediction) because I have stopped trying to find a more reliable income engine for the back half of my life. Every time I look at the rest of my portfolio and feel the urge to do something clever, I add more JNJ instead. It is the position I never have to babysit.

The thesis is simple. I want a check that shows up, grows a little every year, and is backed by a business diversified enough that no single product failure can break the payout. JNJ has been doing exactly that for longer than I have been alive.

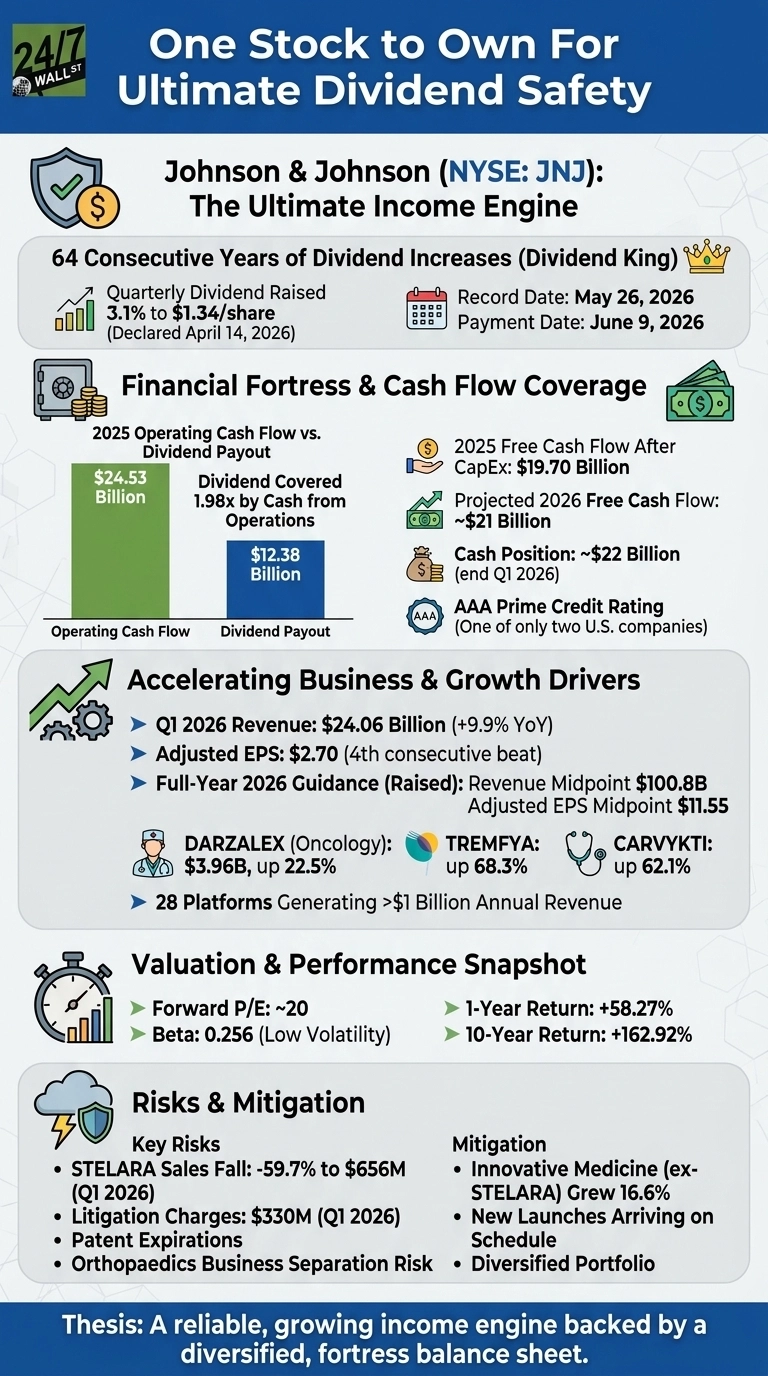

The board just authorized a 3.1% increase to the quarterly dividend, taking it from $1.30 to $1.34 per share, the company’s 64th consecutive year of dividend growth. That is an institution.

The receipts behind the conviction

The first thing I check, every time, is whether the cash is actually there. In 2025, operating cash flow came in at $24.53 billion against a dividend payout of $12.38 billion, leaving the dividend covered 1.98x by cash from operations. Free cash flow after capital expenditures landed at $19.70 billion, and management is guiding to roughly $21 billion in free cash flow for 2026.

Behind that sits about $22 billion in cash and marketable securities and one of only two AAA prime credit ratings among U.S. companies. The check is getting cut from a fortress.

The second piece is that the underlying business is accelerating, not coasting. Q1 2026 revenue was $24.06 billion, up 9.9% year over year, with adjusted EPS of $2.70 marking the fourth consecutive earnings beat. Management raised full-year guidance to a revenue midpoint of $100.8 billion and an adjusted EPS midpoint of $11.55.

DARZALEX did $3.96 billion in the quarter, up 22.5%. TREMFYA grew 68.3%. CARVYKTI grew 62.1%. The company now has 28 platforms generating more than $1 billion in annual revenue.

The third piece is what I pay for that durability. The forward P/E sits at about 20, the beta is 0.256, and the stock has still returned 58.27% over the past year and 162.92% over the past decade. I am not paying a growth multiple for a low-volatility compounder.

The risk I do not pretend away

STELARA is rolling off a cliff. Sales fell 59.7% to $656 million in Q1 2026, dragging Innovative Medicine by roughly 920 basis points. Layer on $330 million of litigation charges tied to ongoing talc exposure and you have real headwinds. I do not wave that away.

What I notice is that JNJ absorbed all of it and still grew revenue almost 10%, because 96% of Innovative Medicine ex-STELARA grew at 16.6%. The new launches, ICOTYDE among them, are arriving on schedule. The portfolio was built for exactly this kind of patent transition.

Why the buy button stays active

CFO Joseph Wolk said it plainly on the Q1 call: “we recognize our shareholders value a growing dividend.” That sentence, backed by 64 years of follow-through, is why I keep buying. I am buying decades of dividend checks from the most diversified healthcare balance sheet in the world, and I plan to keep doing it until the math stops working, which on this evidence is not happening anytime soon.

Contact [email protected] for any questions or corrections.