Johnson & Johnson (NYSE:JNJ | JNJ Price Prediction) has rallied 13.73% year to date and 55.27% over the past year, fueled by oncology blockbusters and a MedTech franchise hitting on every cylinder. CEO Joaquin Duato told investors that “Johnson & Johnson had a strong start to 2026 and is delivering on its promise for a year of accelerated growth and impact.”

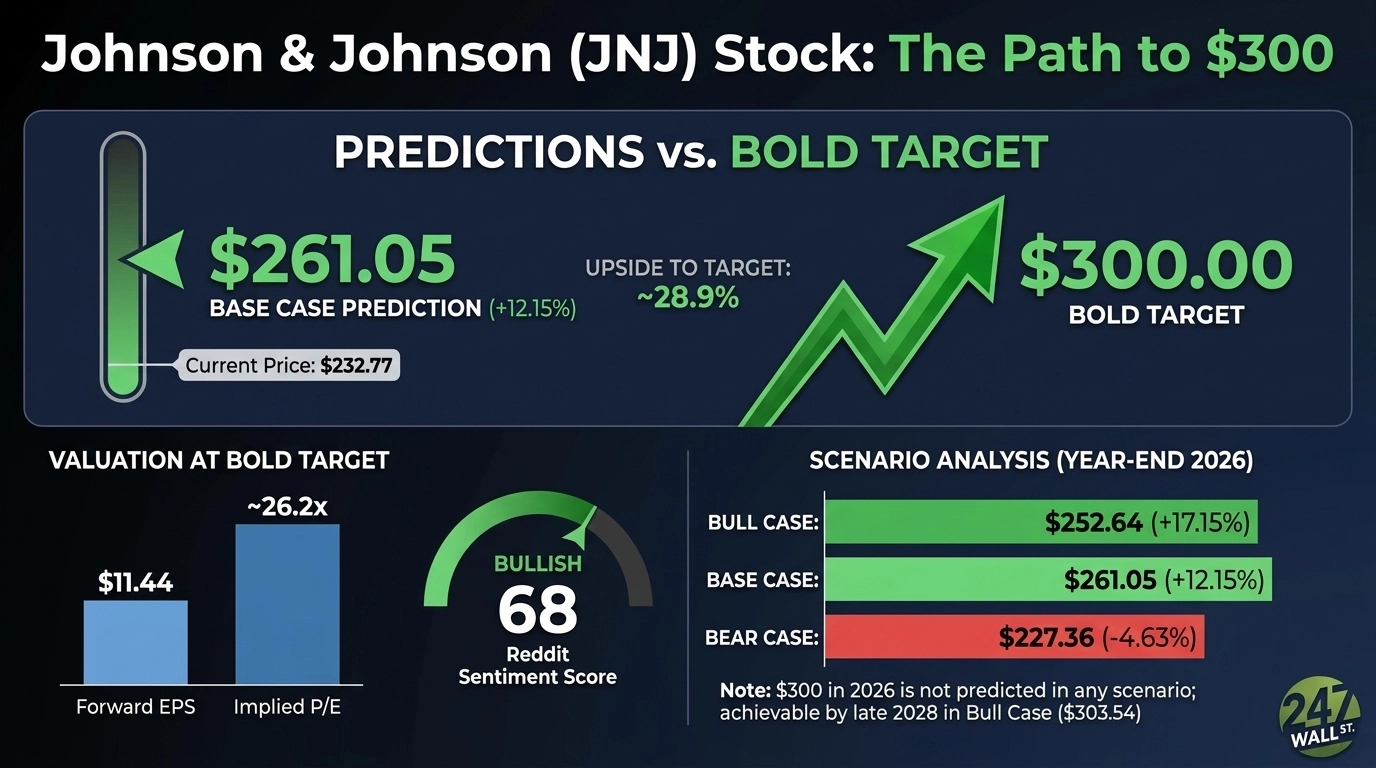

The stock sits at $232.77. Can it push to $300 before year-end?

What’s Holding JNJ Back Right Now

Despite strong gains, JNJ has cooled. Shares are up just 3.3% over the past week and 4.23% over the past month after a May pullback. Q1 2026 net income fell 52.4% YoY, hammered by $330 million in litigation charges and 59.7% STELARA biosimilar erosion.

An FDA Early Alert on Abiomed catheter kits and ongoing talc litigation testimony create overhang. With a beta of just 0.256, JNJ rarely moves fast, so reaching $300 requires a clear catalyst to re-rate the multiple higher.

Wall Street Sees 8.6% Upside. Our Model Says 12.2%

Consensus target sits at $252.87, with 5 Strong Buy, 10 Buy, 8 Hold, and 1 Strong Sell ratings. Our base case lands at $261.05, for 12.15% upside, with a bull case at $252.64 and bear case at $227.36. Confidence on that base case is 90%.

With 63% of analysts bullish and a portfolio firing on oncology and cell therapy, the Street anchors on the earnings dip rather than pipeline torque. Consensus is too cautious.

The Path to $300 Per Share

Reaching $300 from today’s price of $232.77 would require a gain of 28.9%. With forward EPS of $11.44, a price of $300 implies a forward P/E of 26x. Our base case of $261.05 already implies 22x, meaning the bold target requires roughly 4.5x additional multiple expansion.

Is that achievable? Yes, with conditions. The 1.099 247Factor already reflects defensive sector momentum, low volatility, and trading near the 52-week high. Bullish catalysts are stacking up: DARZALEX grew 22.5%, TREMFYA jumped 68.3%, and RYBREVANT/LAZCLUZE surged 82.7% in Q1.

Duato highlighted that “The depth and strength of our portfolio and pipeline is unrivaled,” citing the ICOTYDE and VARIPULSE Pro approvals. Add in positive Phase 2 nipocalimab data in lupus and a TIKR model targeting $325 by 2030, and the multiple expansion story has legs. Main risk: another step-up in talc litigation costs could freeze the re-rate.

Where JNJ Trades Today vs Its Earnings Power

At $232.77, JNJ trades at roughly 20x forward EPS of $11.44. That is reasonable for a healthcare mega-cap raising FY2026 guidance to a midpoint of $11.55 EPS on $100.8 billion in revenue.

Shares sit just 1% from the 52-week high of $250.24, well above the low of $145.39. Over 10 years, JNJ has returned 164.38%. The earnings power keeps compounding, and a Simply Wall St DCF puts intrinsic value at $374.05.

$300 Is a Stretch, But Here’s Why It’s Possible

$300 by year-end is a stretch. It demands a 28.9% gain in roughly seven months from a low-beta defensive name.

The bull case depends on three things: continued double-digit growth from DARZALEX, TREMFYA, and CARVYKTI; another guidance raise on new launches; and a quiet resolution path on talc litigation. One escalating verdict could derail it. We’ve outlined the blueprint for how Johnson & Johnson could reach $300 in 2026.

Contact [email protected] for any questions or corrections.