I keep buying NVIDIA, Eli Lilly, and Johnson & Johnson, and if a fire took my brokerage statement to zero tomorrow, those are the three tickers I would start typing in again on day one. They each do something I cannot replicate by being clever.

Why the buy button stays active on NVIDIA

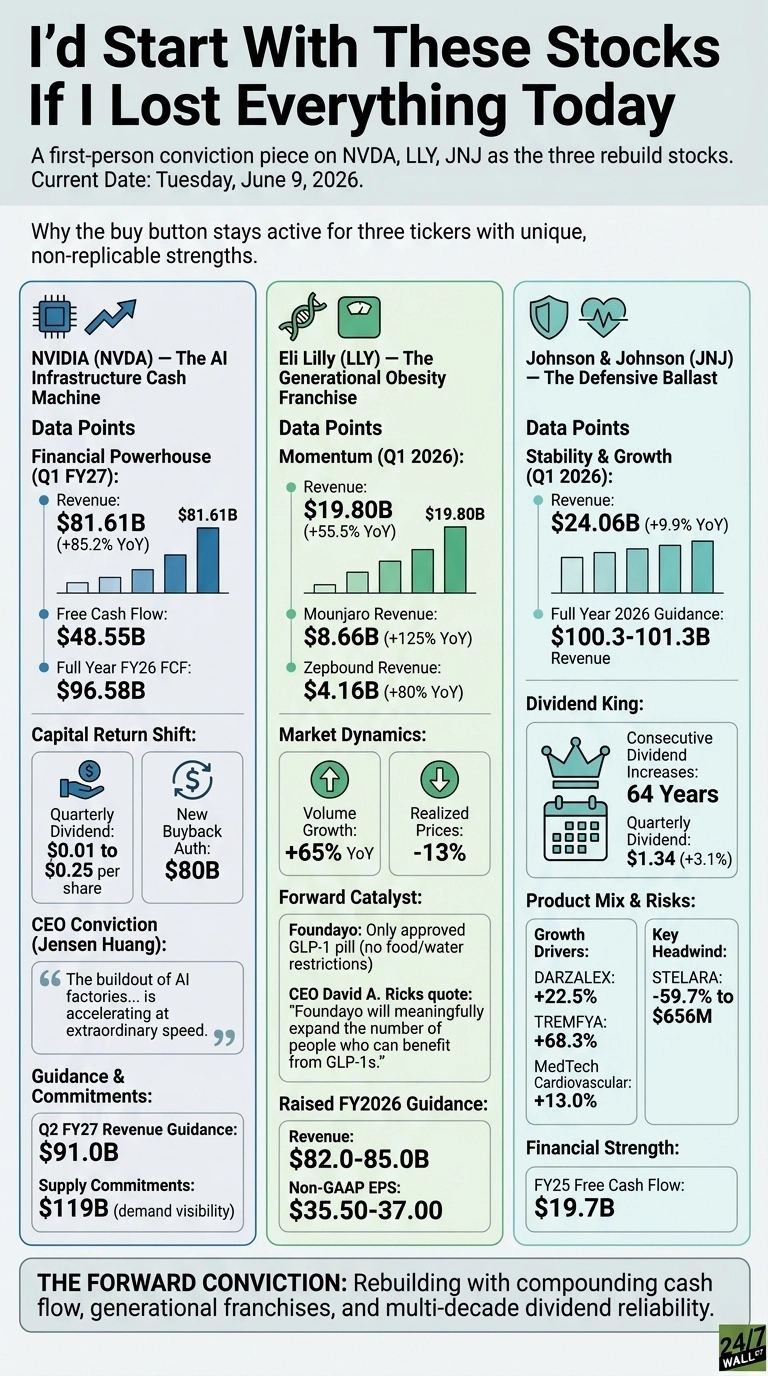

NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) is the one position where I have stopped pretending I can time it. Q1 FY27 revenue came in at $81.61 billion, up 85.23% year over year, with non-GAAP EPS of $1.87 against a $1.7738 estimate. Free cash flow alone was $48.55 billion in a single quarter. Full year FY26 free cash flow reached $96.58 billion. That is the cash machine I am buying.

The capital return shift sealed it for me. The quarterly dividend went from $0.01 to $0.25, a fresh $80 billion buyback authorization landed on top of $38.5 billion remaining, and roughly $20 billion came back to shareholders in Q1.

Jensen Huang framed the cycle plainly: “The buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.” Supply commitments of $119 billion tell me management sees the demand the same way I do.

The honest risk is China. The Q2 guide assumes zero Data Center compute revenue from China, and no H20 shipped last quarter. I respect it. I also note that the company is guiding $91 billion for Q2 anyway. The shares are up 12.01% year to date and 47.42% over one year, and the earnings power is growing faster than the multiple.

Eli Lilly is the franchise I keep underestimating

Eli Lilly (NYSE:LLY) keeps proving me too cautious. Q1 2026 revenue was $19.80 billion, up 55.5% YoY, with EPS of $8.55 against a $6.79 estimate. Mounjaro alone delivered $8.66 billion (125% YoY growth) and Zepbound added $4.16 billion (80% YoY). Full year guidance was raised to $82 to $85 billion in revenue and $35.5 to $37 in non-GAAP EPS.

Foundayo, the first oral GLP-1 that can be taken any time of day without food or water restrictions, is the catalyst I keep coming back to. CEO David Ricks said “Foundayo will meaningfully expand the number of people who can benefit from GLP-1s.”

The honest risk is pricing: realized prices fell 13% in the quarter, with China’s NRDL inclusion adding pressure. Volume grew 65%, which is the answer to that risk.

Johnson & Johnson is the ballast

Johnson & Johnson (NYSE:JNJ) is the one I would buy first, because it is the position that lets me sleep. The quarterly dividend was raised 3.1% to $1.34 per share, the 64th consecutive year of increases.

Q1 2026 revenue rose 9.9% YoY to $24.062 billion, adjusted EPS was $2.70, and full year 2026 guidance was lifted to $100.3 to $101.3 billion in revenue and $11.45 to $11.65 in adjusted EPS. DARZALEX grew 22.5%, TREMFYA grew 68.3%, and 2025 free cash flow was $19.7 billion.

The honest risk is STELARA, which fell 59.7% to $656 million on biosimilar erosion. TREMFYA and the oncology stack are absorbing that hit in real time, and the dividend record speaks louder to me than the biosimilar headline.

The forward conviction

Compounding cash flow at NVIDIA, a generational franchise at Lilly, and 64 years of paid dividends at Johnson & Johnson: that is how I would rebuild a portfolio, and that is why my buy button is still warm.

Contact [email protected] for any questions or corrections.