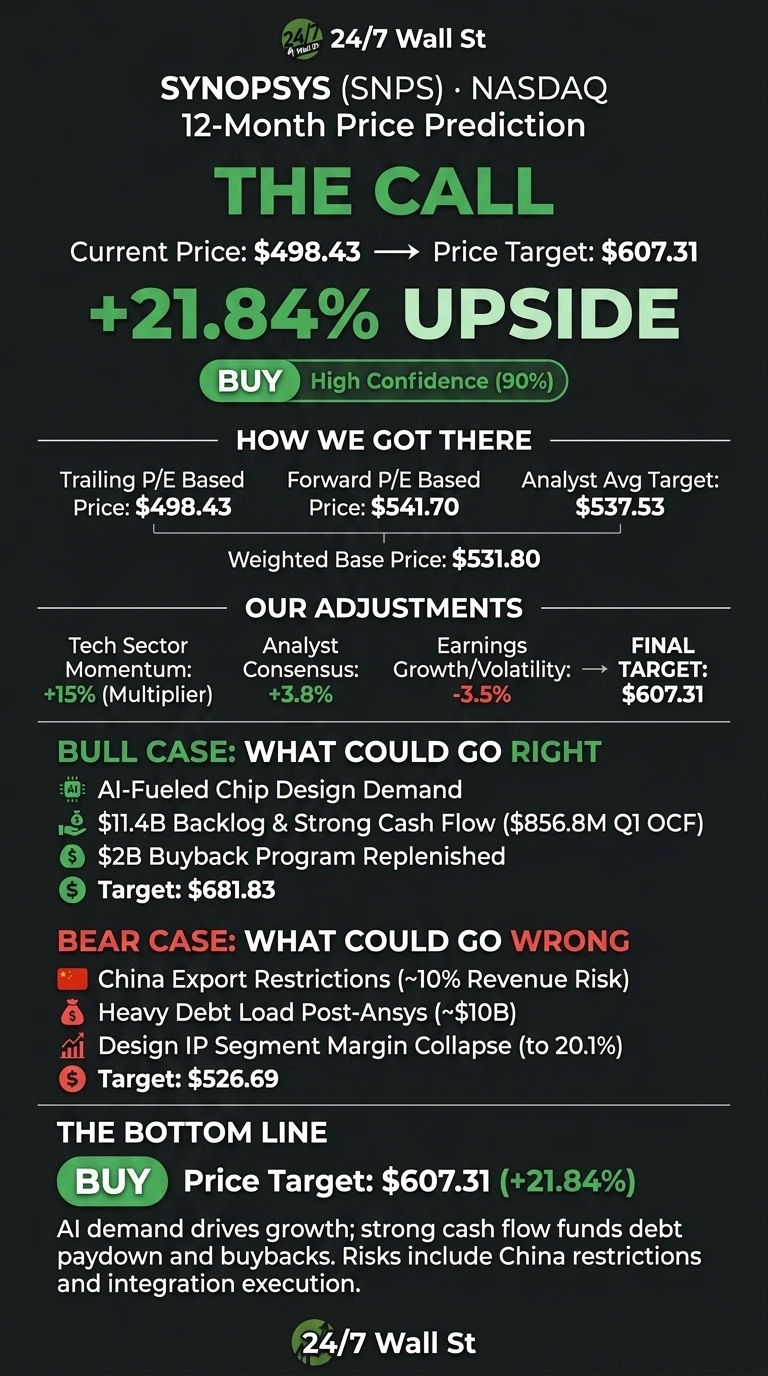

Synopsys (NASDAQ:SNPS | SNPS Price Prediction) has whipsawed investors over the past year, from an August 2025 peak near $617.91 to a November low of $389.83, before settling at $498.43. With the Ansys integration now fully reflected in results and AI-driven chip design demand intact, our model sees room to run.

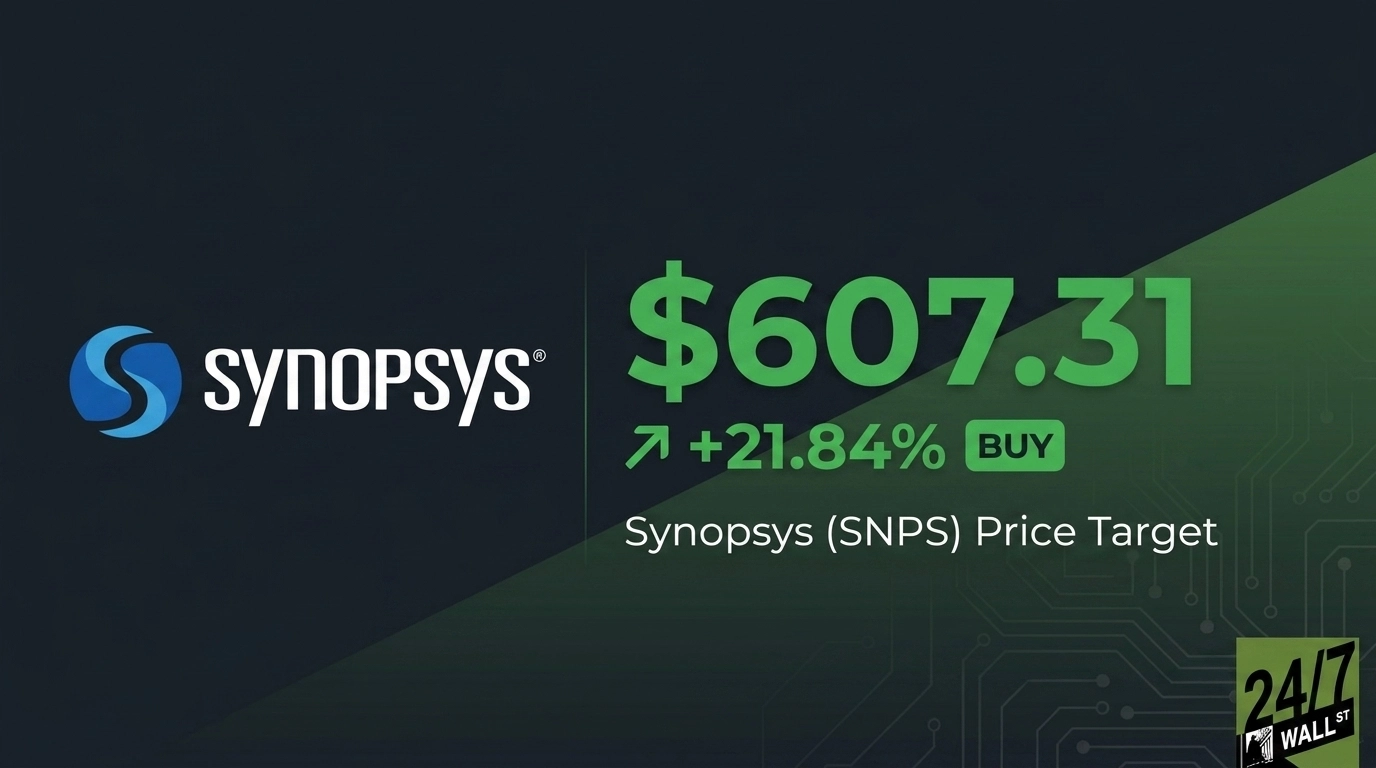

Our 24/7 Wall St. price target for Synopsys is $607.31, implying 21.84% upside over the next 12 months. The recommendation is buy, with a confidence score of 90%, which we consider high.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $498.43 |

| 24/7 Wall St. Price Target | $607.31 |

| Upside | 21.84% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Volatile Path Back to $500

Synopsys is up 10.87% over the past month and 6.11% year to date, though shares slipped 3.44% in the last week. The stock trades 18% below its 52-week high of $651.73 and well above the $376.18 low.

Q1 FY2026, reported February 25, delivered revenue of $2.41 billion, up 65.4% YoY, and non-GAAP EPS of $3.77, beating consensus by 5.98%. Management reiterated FY2026 guidance of $9.56B to $9.66B in revenue and non-GAAP EPS of $14.38 to $14.46. Memorable for shareholders: the Q3 FY2025 miss triggered a 35.84% single-day drop before a recovery began.

The Case for $680+

Bulls have plenty to point to. CEO Sassine Ghazi said “Synopsys enters 2026 with an expanded portfolio, leadership positions across the business, and the most compelling roadmap in our history.” AI-fueled chip design demand is accelerating R&D spend at customers, and Synopsys carries a $11.4B backlog.

Operating cash flow swung to $856.8M in Q1 FY2026 from negative $67M, funding aggressive debt paydown of $3.45B in a single quarter and a replenished $2B buyback.

Wall Street is constructive: 15 Buy and 2 Strong Buy ratings versus 1 Strong Sell, with an average target of $537.53. Our bull case scenario sees Synopsys reaching $681.83 by May 2027, a 36.8% return, if Ansys synergies and AI tailwinds compound.

The Risks Worth Watching

The bear case starts with China. U.S. export restrictions touched roughly 10% of revenue and forced a guidance withdrawal in mid-2025. Debt remains heavy at $10B long-term, GAAP profitability is depressed by $404M in acquired intangible amortization, and the Design IP segment showed margin collapse from 36.7% to 20.1% in Q3 FY2025. Trailing P/E sits at 77, which leaves little room for error.

GAAP weakness stems from acquisition accounting and intangible amortization rather than core operating performance. Non-GAAP EPS guidance of $14.42 at the midpoint implies a forward P/E near 36, far more reasonable. The bear scenario takes SNPS to $526.69, still slightly positive.

Our Take: BUY Rated With High Confidence

The 24/7 Wall St. price target of $607.31 with 90% confidence earns a buy. The tipping factor is cash generation: $2.2B in operating cash flow funds buybacks and debt paydown while AI demand carries the topline. The bull thesis strengthens if Design IP stabilizes and China headwinds don’t worsen. It weakens if export restrictions broaden or Ansys synergies slip past 2027.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $607 |

| 2027 | $682 |

| 2028 | $770 |

| 2029 | $845 |

| 2030 | $904 |

These projections assume Synopsys executes on Ansys synergies and AI-fueled design demand persists. Significant upside or downside could result from China export policy shifts or material changes to the EDA competitive landscape.

Contact [email protected] for any questions or corrections.