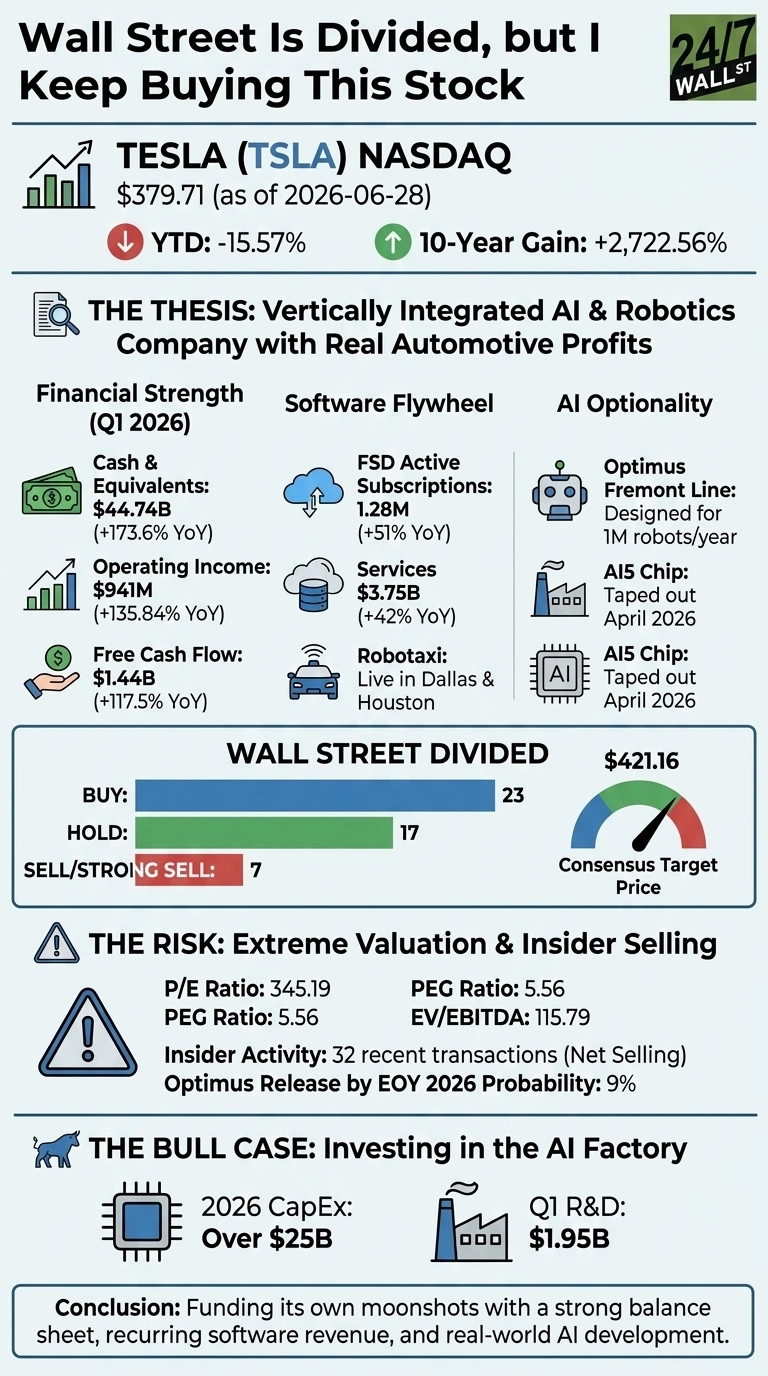

I bought Tesla (NASDAQ:TSLA | TSLA Price Prediction) again last Friday, and I will probably buy it again next month. The bears on Reddit and the seven analysts carrying Sell or Strong Sell ratings have not talked me out of it, and neither has a year-to-date drawdown of -15.57%.

I keep coming back to the buy button because Tesla is the rare company where the cash flow statement and the science fiction roadmap are now pointing the same direction, and I want to own that before the market decides it agrees.

The Thesis I Keep Coming Back To

The simple version: Tesla is turning into a vertically integrated AI and robotics company that still happens to print real automotive profits. In Q1, automotive gross margin expanded to 21.1% from 16.2% a year earlier, revenue grew 15.78% YoY to $22.387 billion, and operating income jumped 135.84% to $941 million. The core business is widening.

Three Reasons The Conviction Holds

First, the balance sheet. Tesla closed Q1 with $44.743 billion in cash and equivalents, up 173.62% YoY, against a debt-to-equity ratio of 0.10 and net cash on the books. Free cash flow climbed 117.47% to $1.44 billion, and full-year 2025 FCF rose 73.69% to $6.22 billion. A company with that much cash funds its own moonshots.

Second, the software flywheel. Active FSD subscriptions hit 1.28 million, up 51% YoY, and the Services and Other segment grew 42% to $3.745 billion. Unsupervised Robotaxi rides are already live in Dallas and Houston, and FSD just cleared regulators in the Netherlands. Recurring software revenue at automotive scale is a different business than building cars.

Third, the optionality. Elon Musk told investors on the Q1 call that “Optimus will be our biggest product, not just Tesla’s biggest product ever, but probably the biggest product ever.” The Fremont line is designed for 1 million robots a year and the Gigafactory Texas line for 10 million. I just need those numbers to be non-zero.

The Risk I Will Not Pretend Away

The valuation is the real problem. A trailing P/E of 345, a PEG of 5.56, and EV/EBITDA of 116 leave no margin for error. Insiders have logged 32 recent transactions with net selling, and Polymarket traders give the Optimus release just a 9% probability by year-end. If FSD takes another year and Optimus slips into 2027, this stock can hurt.

What keeps me buying anyway is that the multiple is pricing the AI factory, and that AI factory is being built with real capex. CapEx is running at over $25 billion for 2026, R&D was $1.95 billion in Q1, and the AI5 chip taped out in April 2026. Every dollar of that spend is visible in the filings.

Why The Buy Button Stays Active

Wall Street is split for a reason. 23 analysts rate Tesla a Buy and 24 do not, with a consensus target of $421.16 against today’s $379.71.

Ten-year holders are sitting on a 2,722.56% gain through every cycle of doubt. I am buying the company that funds its own future in cash, sells its software to over a million paying drivers, and has already built the line for the robot. The next decade just has to rhyme with the last.