Savita Subramanian, Bank of America Securities’ head of US equity and quantitative strategy, took to CNBC this week with a simple message. Corporate earnings are “gangbusters”, and the trade you actually want is the one no one is memeing about. Her pitch is that cyclicals are cheap, capex is accelerating, and the boring stuff has room to run for years, not quarters.

Her framing: “Corporate earnings are actually gangbusters this year. I mean, we started the year above consensus at 15%. We’re now tracking something like 20% earnings growth, which is basically a multiple on the average earnings growth.”

The macro tape backs her up. Total US corporate profits hit $4.4 trillion in Q1 2026, up 12.8% year over year. Manufacturing profits ran to $773.3 billion from $591.1 billion a year earlier. Mining value added exploded 22.8% in the quarter, the strongest number of any sector. And gross private investment contributed 7.9% to Q1 GDP.

Why she says skip the index

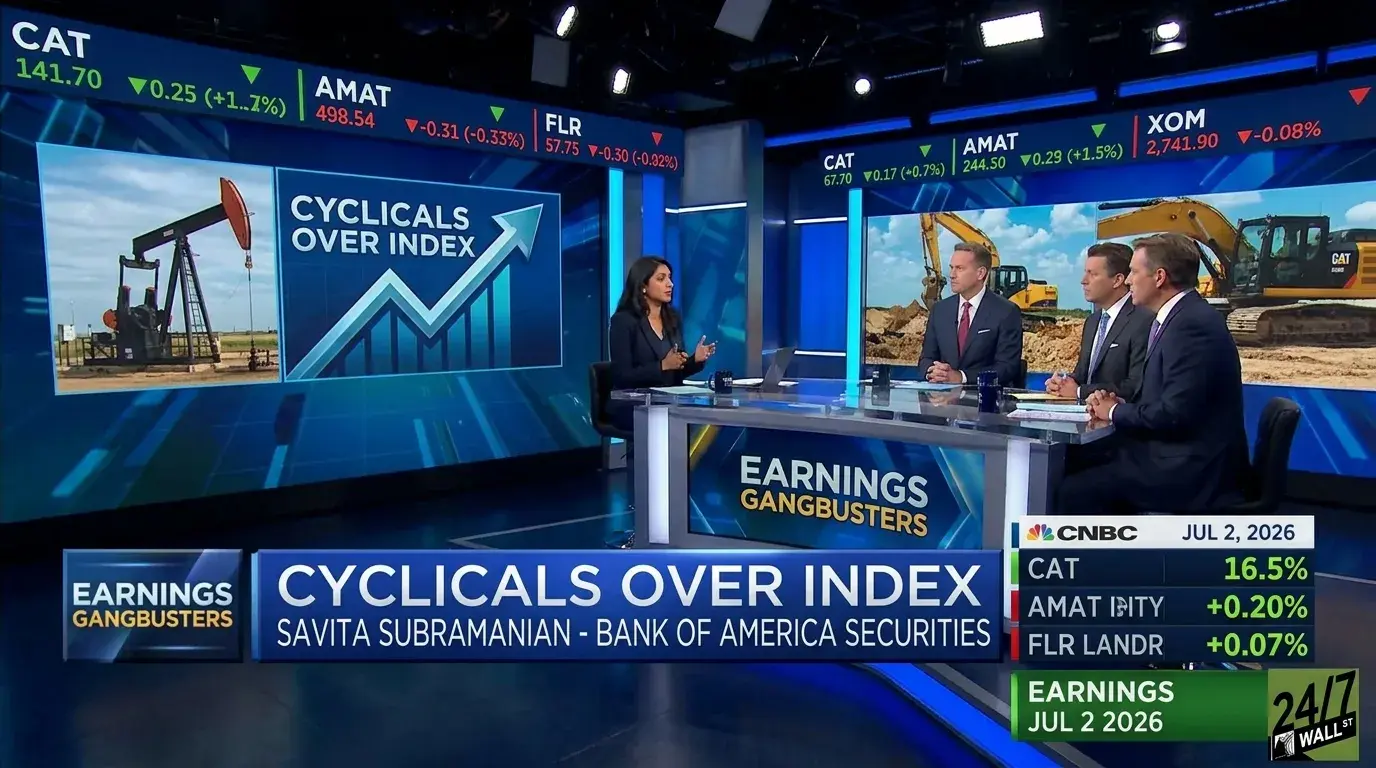

Subramanian’s argument is that the S&P 500 you buy through a cap-weighted ETF has quietly become a handful of mega-cap tech names with a decorative fringe. She wants the fringe. “Our view is go for cyclical companies that benefit from GDP growth. We’re in a great nominal GDP environment. And that’s the one area of the market that’s still trading pretty cheap.”

Check the tape. The SPDR S&P 500 ETF is up 9.63% year to date. Meanwhile Caterpillar (NYSE:CAT | CAT Price Prediction) is up 59%, Applied Materials (NASDAQ:AMAT) is up 117%, and Fluor (NYSE:FLR) is up 18%. Cyclicals are winning already, and yet forward multiples remain unassuming. Exxon Mobil (NYSE:XOM) trades at a forward P/E of 12x. Barrick Mining (NYSE:B) trades at 9x, and is actually down 14.6% YTD despite posting a record $2.73 billion in operating cash flow last quarter. The dispersion is the opportunity.

The sectors she’s actually betting on

Her list. “That would be industrials energy materials… if you build stuff you need the widgets… machinery engineering, construction, oil, metals, these are the areas that I think could do really well over the next not just 12 months, but maybe the next few years.” On energy specifically. “Oil just looks like it’s undervalued. These energy companies have capital discipline.”

Exxon fits the discipline story. Q1 adjusted EPS of $1.16 beat the $1.01 consensus, underlying earnings ran to $8.77 billion, and the company is executing a $20 billion repurchase program in 2026 with structural cost savings pushing toward a $20 billion cumulative target by 2030 (see the Q1 8-K). WTI at $73.59 is off April’s $105.67 peak, which is part of why the group still screens cheap.

Caterpillar is the machinery-plus-AI story. Q1 revenue climbed 22.2% to $17.41 billion, and Power Generation, powered by hyperscaler data center demand, ran up 41%. Fluor is the picks-and-shovels engineering play, snagging FEED work on Centrus uranium enrichment and gas power, with 98% of new awards reimbursable. Vulcan Materials is aggregates, boring rock for boring highways, and Q1 EBITDA margin still expanded to 25.5%. Barrick just hiked its base dividend 40% and is prepping a North American gold spin by late 2026.

Then there’s the semi angle. Subramanian flagged the recent chip-equipment selloff as puzzling given the setup, and Applied Materials just guided calendar 2026 equipment growth to more than 30%, with Q2 FY26 EPS of $2.86 versus $2.66 expected.

One caveat worth holding in your head. If nominal GDP really is this hot, the Fed gets a reason to stay tighter for longer, and that pressures multiples across everything. Subramanian’s bet is that cyclical earnings power outruns the discount rate. Whether it does is the question you should actually be asking before you rotate.

Contact [email protected] for any questions or corrections.