Starbucks (NASDAQ:SBUX | SBUX Price Prediction) and Chipotle Mexican Grill (NYSE:CMG) just delivered two of the most instructive turnaround updates in restaurants.

Starbucks posted its clearest inflection yet under Brian Niccol. Chipotle, still working through a full year of negative comps, leaned harder on unit growth and menu innovation. Same sector, two very different scoreboards.

Coffee Traffic Comes Back. Burrito Traffic Still Hasn’t.

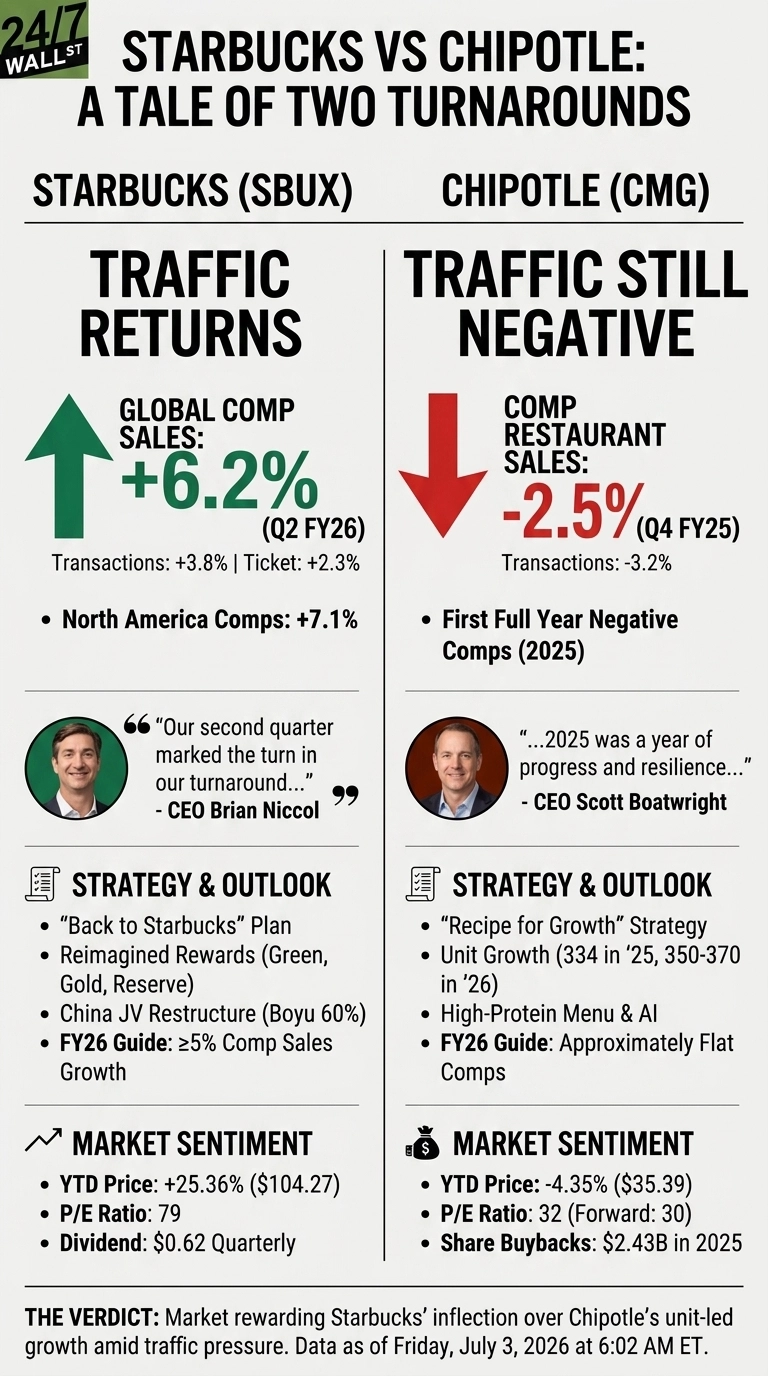

Starbucks’ Q2 FY2026 report showed global comparable store sales up 6.2%, with transactions up 3.8% and ticket up 2.3%. North America comps ran 7.1%, driven by real foot traffic rather than pricing. Revenue landed at $9.53 billion, up 8.79% year over year, and non-GAAP EPS of $0.50 beat the $0.44 estimate.

Niccol called it plainly: “Our second quarter marked the turn in our turnaround as our Back to Starbucks plan drove both top and bottom line growth.”

Chipotle’s Q4 2025 print told a rougher story. Comparable restaurant sales fell 2.5% on a 3.2% transaction decline, and restaurant-level operating margin compressed to 23.4% from 24.8%. EPS of $0.25 squeaked past the $0.24 consensus, but 2025 was Chipotle’s first full year of negative comp sales.

CEO Scott Boatwright framed it as resilience, pointing to “the early success of our high-protein menu and benefits from our high-efficiency equipment package.”

Back to Starbucks vs. Recipe for Growth

The strategic playbooks diverge more than the branding suggests. Starbucks is defending traffic with a reimagined three-tier Rewards program (Green, Gold, Reserve), a restructured China joint venture where Boyu Capital holds 60%, and plans for 600 to 650 net new coffeehouses in FY26.

Chipotle is buying growth with concrete: 334 openings in 2025 and 350 to 370 planned for 2026, roughly 80% with a Chipotlane.

| Lens | Starbucks | Chipotle |

| Comp trend | +6.2% global | -2.5% |

| Traffic | +3.8% transactions | -3.2% transactions |

| Growth engine | Rewards, China JV, ticket mix | New units, high-protein menu, AI |

| Capital return | $0.62 quarterly dividend | $2.43B buybacks in 2025 |

| FY26 comp guide | ≥5% | Approximately flat |

Valuations reflect the mood. Starbucks trades at a P/E of 79, priced like the turnaround is confirmed. Chipotle sits at 32, with a forward multiple of 30, cheaper but attached to shrinking traffic. Consumer spending on Food Services keeps rising, hitting $1,538.3 billion in May 2026, so this is not a macro problem. It is a share problem.

The Next Test Is Whether Chipotle Can Fix Traffic

Watch three things. First, whether Starbucks holds North America transaction momentum against a 170 bps margin contraction from labor investments, tariffs, and coffee pricing.

Second, whether Chipotle’s high-protein menu and equipment rollout can flip transactions positive after four straight negative quarters.

Third, capital allocation. Starbucks is protecting its 64th consecutive quarter of dividends despite negative shareholders’ equity of $8.5 billion. Chipotle is buying back stock aggressively, with $1.7 billion remaining on the authorization.

Why I Lean Toward Starbucks Today, But Keep Chipotle on the Bench

I lean Starbucks right now. The data actually supports the story Niccol is telling, and shares are up 25.36% year to date at $104.27. That said, a 79 P/E leaves little room for a stumble, and insiders have been net sellers.

Chipotle looks more interesting for turnaround investors comfortable with volatility. The stock is down 37.66% over the past year to $35.39, yet analysts still carry a $42.88 target and 26 buy or strong-buy ratings. If Boatwright gets transactions positive by mid-2026, that gap closes fast. Until then, I want to see one clean quarter of positive traffic before I would step in.

Contact [email protected] for any questions or corrections.