Two Very Different Decades

Microsoft (NASDAQ:MSFT | MSFT Price Prediction) and Chipotle Mexican Grill (NYSE:CMG) both rewarded long-term holders through the 2010s, but their recent chapters have diverged sharply.

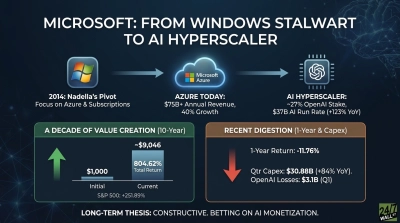

Under Satya Nadella, Microsoft pivoted from a Windows and Office licensing shop into a cloud-and-AI platform anchored by Azure, which crossed $75 billion in FY2025 revenue, up 34%. A restructured OpenAI partnership left Microsoft with a roughly 27% stake valued near $135 billion and an AI business running at a $37 billion annualized revenue run rate, up 123% year over year. Acquisitions of LinkedIn, GitHub, and Activision Blizzard reshaped the mix.

Chipotle’s trajectory is more complicated. Brian Niccol’s turnaround introduced Chipotlanes, digital ordering, and a loyalty program, then a 50-for-1 split in June 2024 followed his exit to Starbucks. New CEO Scott Boatwright inherited a brand that just posted its first full year of negative comparable sales, with FY2025 comps sliding and Q4 transactions down 3.2%.

What $1,000 Actually Did

Using split-adjusted total returns through the most recent close, here is what a $1,000 investment in either stock became over the past decade, compared to the S&P 500 gain:

| Period | Microsoft | Chipotle | S&P 500 |

|---|---|---|---|

| 1 Year | $802 (−19.85%) | $623 (−37.66%) | $1,200 (+20.04%) |

| 5 Year | $1,466 (+46.56%) | $1,130 (+12.97%) | $1,717 (+71.72%) |

| 10 Year | $8,633 (+763.30%) | $4,492 (+349.21%) | $3,548 (+254.79%) |

A $1,000 stake in Microsoft a decade ago outpaced the index, roughly tripling the S&P’s return. Chipotle also beat the market over 10 years, but nearly the entire lead was banked before 2022. Both stocks have lagged badly in the past year, with Microsoft caught in an AI capex hangover (Q3 FY26 capex hit $30.88 billion, up 84.39%) and Chipotle punished for declining traffic.

Looking Ahead

Where to put $1,000 today? Into Microsoft if you believe the $627 billion commercial RPO backlog converts into durable operating leverage as AI capex normalizes. Analysts have a consensus price target of $561.11, and the forward P/E near 20x looks reasonable. On the other hand, avoid it if OpenAI-related losses keep compounding and Azure growth decelerates below 30%.

The bull case for Chipotle is if Boatwright’s “Recipe for Growth” restores positive transactions and the runway toward 7,000 restaurants holds. But beware the 32x trailing earnings multiple while comps stay flat and margins compress.

The question is whether the AI infrastructure story and backlog are more attractive than a potential burrito turnaround.

Contact [email protected] for any questions or corrections.