$2.13 trillion. That is what public markets say SpaceX (NASDAQ:SPCX | SPCX Price Prediction) is worth as of this morning, a valuation the company reached less than a month after its June IPO and just ahead of confirmed entry into the Nasdaq-100. The stock trades at $160.46 after slipping 0.95% today, but zoom out and shares are up 5.88% over the past week.

Is this a rocket ship or bubble?

What a $2.13 trillion price tag buys

SpaceX launches more than 80% of the world’s mass to orbit each year, operates roughly 9,600 Starlink satellites, delivers broadband to millions of customers across 164 countries, territories, and other markets, and now owns xAI (acquired in early 2026), giving it a frontier AI model in Grok. Falcon rockets run a mission success rate above 99%. Starship keeps flying. That is the operational base underneath the number.

A $2.13 trillion price tag prices a bet that Starlink becomes a global telecom utility, xAI becomes a core AI franchise, and Starship becomes the freight rail of Earth-to-orbit compute. No public P/E to argue with as it remains loss-making until the Anthropic and Google deals start bringing in money, so the debate is about narrative, cash flow trajectory, and how much index-fund money is about to be forced through the door.

The bull case is substantial

Nasdaq-100 inclusion is the mechanical part. When SPCX joins the index, every fund tracking it has to buy, whether the manager likes the valuation or not. That is non-discretionary demand hitting a float that is already tight after a June IPO. The retail crowd has been chewing on this for weeks.

Then there is the AI-compute optionality. Reports linking SpaceX to Google, Anthropic, and the Starmind orbital AI-infrastructure concept reframe the company as more than launch and broadband. Sylvia Jablonski, CIO of Defiance ETFs, put it plainly. “SpaceX is a multi-platform infrastructure company involved in launch, communications, defense, and AI connectivity, with Starlink poised to exceed expectations.”

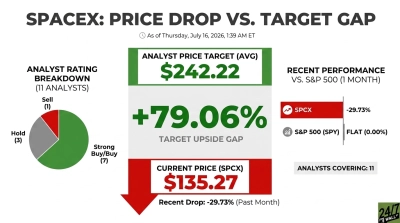

The Street is starting to underwrite that view. Analyst coverage skews to 7 buys, 3 holds, 1 sell, with a consensus target of $188.57, implying 17.52% upside from the current price. Reddit’s 7-day sentiment score has climbed to 65.21 (bullish), while the 30-day composite sentiment trend has moved up +8.68 points.

The bear signals worth respecting

$2.13 trillion demands near-perfection. Post-IPO price action has been ugly at times. CNBC reported the average buyer was almost underwater after a two-day slide, shares fell 3.6% to $184.98 and a five-day volume-weighted average of $181.71, after peaking above $225. Musk lost trillionaire status inside two weeks. His paper fortune fell from a peak of $1.32 trillion to $957 billion in a broader tech rout. The Atlantic’s James Surowiecki argued SpaceX and peers are going public “primarily to raise an unprecedented amount of capital needed for the extremely expensive artificial intelligence race,” a framing that reads as bubble kindling more than bull thesis.

Polymarket’s crowd is skeptical of the ceiling. End-of-July contracts price only a 20% probability that SPCX closes above $210, and just 27% above $180. Today’s daily direction market leans down at 63%. Prediction markets are negotiating with themselves.

What the setup says

The forced index bid is a real catalyst you can point to on a calendar. Starlink’s cash generation is real. The AI-compute story, whether or not Starmind ships on time, is a call option the market has clearly decided to price. Analyst consensus, Reddit sentiment at 65.21, and prediction-market crowd accuracy running at 66.7% on recent directional calls all lean the same way. The bear case is about discipline, whether execution can justify $2.13 trillion.

For long-term holders weighing exposure, the next real tests are Nasdaq-100 inclusion mechanics and the eventual insider lock-up expiration.

Contact [email protected] for any questions or corrections.