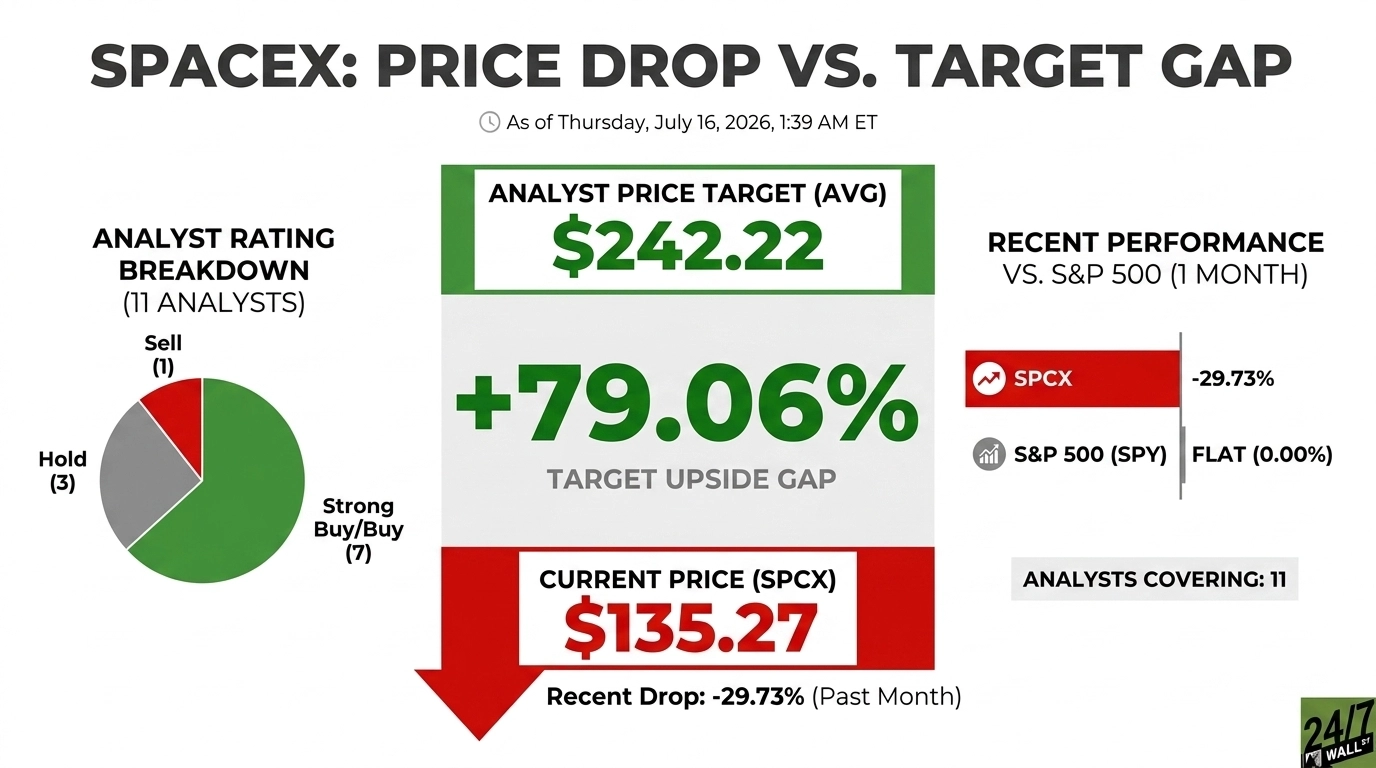

SpaceX (NASDAQ:SPCX | SPCX Price Prediction) trades at $135.27, sitting right on its $135 IPO price from June. The average Wall Street price target sits at $242.22, implying 79.06% upside from current levels.

That gap widens when you notice the outlier. Raymond James analyst Brian Gesuale carries an $800 price target, implying roughly 491% upside from current levels. His thesis reframes SpaceX from a rocket company into a generational industrial platform, with a $10.5 trillion implied valuation tied to Starship economics and decentralized AI compute sold from orbit.

SpaceX went public on NASDAQ on June 12, 2026 in the largest capital raise in history, raising $75 billion at a $1.75 trillion valuation. The stock opened at $150, ripped past $225, and has since given all of it back.

A Round Trip Back to the IPO Price in Five Weeks

SPCX has fallen 29.73% over the past month, wiping out every dollar of post-IPO gains and sending the newly minted mega cap back to its offering price. That qualifies as a violent unwind for a company that briefly carried a $2 trillion-plus valuation.

The selloff stemmed from profit-taking after retail piled in (over $70 billion in demand chased a limited float), broader tech-sector weakness, and growing valuation skepticism as the market chewed through what The Atlantic called a company “untethered from traditional corporate finance metrics.” A muted reaction to NASDAQ-100 inclusion confirmed the mood had shifted.

The bear case has real substance. CFRA opened coverage at $115, sitting below where the stock trades today. Reddit’s biggest recent SPCX post is titled “The math isn’t mathing on the SpaceX IPO.”

Why the Sell Side Is Sticking With the Bull Case

Coverage skews decisively bullish, with 7 Buy ratings, 3 Holds, and 1 Sell. The pitch rests on Starlink, Starship, and the newly bolted-on xAI compute business as three distinct S-curves that public markets have never underwritten together.

With implied upside above 40%, the analyst thesis deserves careful reading. Raymond James’s Gesuale is the most aggressive voice, modeling $837 billion in company revenue by 2031 if Starship reaches full reusability. That math depends on a second stage that lands and reflies, which SpaceX plans to attempt in the back half of 2026.

The near-term bridge is compute. Sell-side revenue models now flex from $18 billion in the S-1 toward roughly $62 billion next year on Colossus GPU rental deals with Anthropic ($1.25 billion per month) and Google ($920 million per month). If SpaceX’s first post-listing quarterly report (due late this month) validates the run rate, the $242 average target moves within range.

The Peer Group Sold Off Together, but SPCX Fell Hardest

Every US-listed space peer sold off with SPCX, though none matched the drawdown.

Rocket Lab (NASDAQ:RKLB) trades at $76.20, down 30.25% over the past month. Its consensus target sits at $116.57, implying 52.98% upside, with 14 Buys and 3 Holds. Analysts view Rocket Lab as the cleaner Neutron and defense story.

AST SpaceMobile (NASDAQ:ASTS) sits at $67.58, off 24.28% over a month, with a $81.47 target and 20.55% upside. Coverage is more balanced at 2 Buys, 7 Holds, and 2 Sells after a nasty Q1 double miss.

The largest analyst-implied upside in the group belongs to SPCX. Wall Street treats the primary name as the most dislocated stock in a dislocated sector.

What the Numbers Actually Show

SPCX trades at $135.27 against a consensus target of $242.22, for 79.06% implied upside across the 11 analysts covering it. The stock is down 29.73% over the past month and 8.79% in the past week.

Over the same one-month window, the S&P 500 ETF (SPY) was essentially flat, and it has posted a 10.69% year-to-date gain. SPCX-specific pressure drove the move while the broader market stayed roughly flat.

The Rocket Company vs. the Space Data Center

The case for SpaceX here rests on whether Starlink and Starship execution alone justify a return to $200-plus. That path is credible: reusable second-stage progress, index buying, and a first earnings report showing the Anthropic and Google run rates would rebuild momentum quickly.

The more cautious view questions the Raymond James thesis. The $800 target depends on space-based data centers requiring roughly 200 Starship launches per gigawatt, unproven repair economics, and pricing power that CoreWeave-style comps at $63 billion do not obviously support. Ninety-day cancellation clauses on the biggest GPU contracts add fragility to the boldest case.

The balanced read is cautiously constructive at the IPO price, skeptical of the moonshot target. A $242 consensus with a hard Starship catalyst on the calendar is reasonable risk/reward. Underwriting $800 requires believing SpaceX becomes the internet’s power grid. That’s a story that warrants seeing the second-stage recovery test before paying for.

Contact [email protected] for any questions or corrections.