The three most valuable companies in the world, NVIDIA (NASDAQ:NVDA | NVDA Price Prediction), Apple (NASDAQ:AAPL), and Google parent Alphabet (NASDAQ:GOOG), collectively command a combined market cap north of $13 trillion and sit at the center of the AI capex boom. Each enters the second half of 2026 with a very different risk/reward setup. Here is a Buy, Sell, or Hold verdict on all three at current prices.

NVIDIA at $194.83: Buy the Multiple Compression

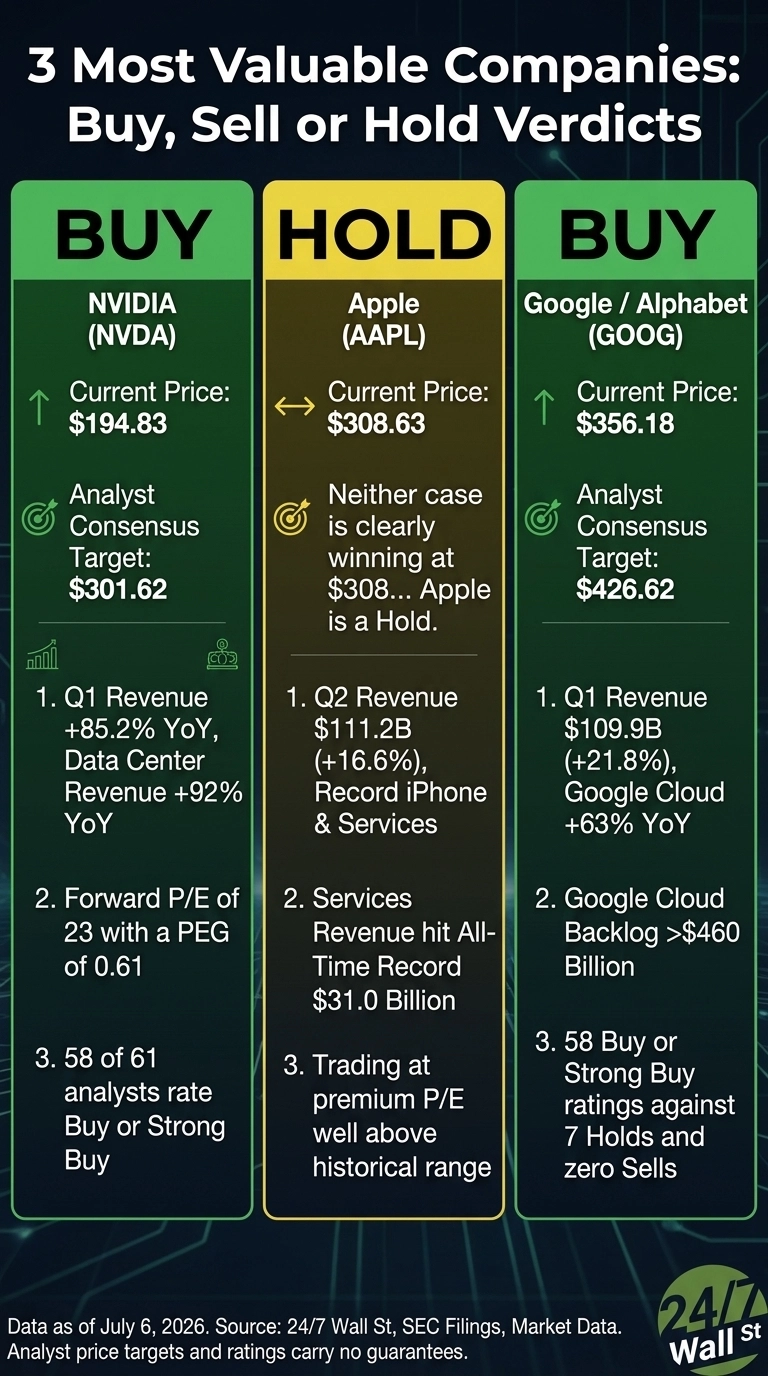

NVIDIA trades at $194.83, down 12.46% over the past month and up only 4.59% year to date, a striking pause after a 854% five-year run. The fundamentals kept moving. Q1 FY2027 revenue hit $81.6 billion (+85.2% YoY), data center revenue reached $75.2 billion (+92%), and networking exploded 199%. Non-GAAP gross margin held at 75% and free cash flow reached $48.6 billion.

The valuation is arguably its cleanest setup in years. Forward P/E sits at 23 with a PEG of 0.61. Consensus target is $301.62, and 58 of 61 analysts rate it Buy or Strong Buy. A market leader with accelerating revenue and a compressed multiple is a rare combination, even acknowledging that targets carry no guarantees. At $194.83, NVIDIA is a Buy.

Apple at $308.63: Hold the Premium

Apple trades at $308.63, up 13.74% YTD and 45.86% over the past year. Q2 FY2026 delivered $111.2 billion in revenue (+16.6%), a March-quarter iPhone record on the iPhone 17 lineup, and a Services all-time high of $31.0 billion. Management raised the dividend 4% and authorized a fresh $100 billion buyback. CEO Tim Cook called it “our best March quarter ever”.

The rub is valuation. Apple trades at a premium P/E well above its historical range, at a moment when growth is strong yet not extraordinary. Bulls point to Services, buybacks, and 2.5 billion active devices.

Bears counter with China exposure, hardware cyclicality, and an AI narrative gap versus NVIDIA and Alphabet. Neither case is clearly winning at $308. The September quarter and next iPhone cycle will likely settle the argument. Apple is a Hold.

Alphabet at $356.18: Buy the Full Stack

Alphabet trades at $356.18, up 98.71% over the past year. Q1 2026 revenue reached $109.9 billion (+21.8%), with Google Cloud growing 63% to $20 billion and backlog nearly doubling to over $460 billion. Search revenue still grew 19%, defusing the “AI kills Search” thesis, and Gemini’s paid enterprise monthly active users climbed 40% QoQ.

The cost is a punishing capex program: $35.7 billion in Q1 and guided $175 to $185 billion for 2026, which cut Q1 free cash flow 46.6%. Even so, Alphabet trades at a forward P/E of 25, cheaper than Apple, with a consensus target of $426.62 and 58 Buy or Strong Buy ratings against 7 Holds and zero Sells. At $356, Alphabet is a Buy.

The Bottom Line

Analyst price targets remain one data point among many, and each of these names carries real risk: NVIDIA’s China exposure and $119 billion in supply commitments, Apple’s premium valuation, and Alphabet’s ballooning capex. The story across the trio is straightforward.

NVIDIA offers the cleanest AI-infrastructure exposure at the most reasonable multiple in years. Alphabet bundles Cloud acceleration with a resilient Search franchise at a mid-20s P/E. Apple asks investors to pay a premium for stability rather than acceleration. That produces two Buys and a Hold.

Contact [email protected] for any questions or corrections.