Apple is back at the top of every watchlist after the latest quarter showed iPhone revenue rebounding and CEO Tim Cook touting “extraordinary demand for iPhone 17 lineup”. The setup beneath the headline numbers is more interesting.

Nintendo just raised hardware prices to offset rising memory chip costs, and memory can constitute 10% to 15% of the total bill of materials for high-end smartphones. That is the canary. Apple still derives roughly half of revenue from one device, and the market is paying a software-grade multiple for a hardware business about to absorb component inflation the supply chain has already telegraphed.

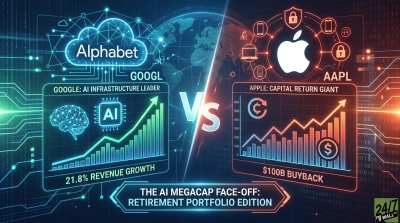

Apple (NASDAQ:AAPL | AAPL Price Prediction) trades at a P/E near 38x with a price-to-book of 58.30 and a free cash flow yield of just 2.30%. The most recent quarter delivered EPS of $2.01 on revenue of $111.18B, up 16.6% YoY, with iPhone contributing $56.99B and Greater China another $20.50B of geopolitical exposure. A $100B buyback authorization and a 4% dividend hike are pleasant, and they also signal management cannot find a better use for the cash.

Insiders are walking. Director Arthur Levinson disposed of roughly 255,000 shares on May 6 near $285, and Cook, the CFO, the COO, and SVP O’Brien all sold in early April. Shares have run 12.47% in the past month and 48.19% over the last year, yet Polymarket gives Apple only a 20.5% probability of finishing May above $300. That is a crowded trade staring down a memory-chip cost shock.

The Redirect: Alphabet Is Cheaper, Faster, and Less Exposed

Alphabet (NASDAQ:GOOGL) is the stock the headlines keep missing. Three reasons it deserves a closer look from investors weighing Apple’s current setup.

1. The valuation gap is absurd. Google trades at roughly 17x earnings with a 5.84% earnings yield and debt-to-equity of 0.14 against Apple’s 1.52. Net margin runs 32.80%, return on equity 35.70%, and return on invested capital 29.60%. You pay less than half Apple’s multiple for a cleaner balance sheet and superior returns on capital.

2. The growth is accelerating. Q1 26 revenue grew 21.8% to $109.90B, well ahead of Apple’s pace. EPS came in at $5.11 against a $2.63 estimate, a 94.10% beat. Google Cloud grew 63% to $20.03B with backlog nearly doubling QoQ to $460B. Gemini is processing 16 billion tokens per minute via API, up 60% QoQ, while enterprise paid monthly active users rose 40% QoQ.

3. Optionality without hardware exposure. Search revenue rose 19% to $60.40B with AI experiences driving usage, 350 million paid consumer subscriptions generate recurring cash, and Waymo is running 500,000+ autonomous rides per week. Memory chip inflation touches none of it. Capex of $175B to $185B in 2026 funds the AI infrastructure competitors rent from Google.

The market has begun voting. Alphabet is up 24.25% year-to-date and 155.31% over twelve months, while Apple sits at 7.86% YTD. Google still trades at less than half Apple’s P/E. That dislocation closes one way.

The takeaway: Alphabet’s valuation and growth profile warrant closer research alongside Apple as the memory-cost cycle plays out.

Contact [email protected] for any questions or corrections.