Veteran energy analyst Paul Sankey, president of Sankey Research, said in a July 9, 2026, CNBC interview that he believes crude oil is no longer the biggest constraint on the energy system. Instead, the real bottleneck sits in U.S. refining capacity, where limited supply continues to keep gasoline prices elevated even as crude prices remain well below recent highs. That distinction, he says, has major implications for energy investors.

His framing came as oil rose 5% the prior session, with Sankey warning that geopolitics remain unresolved: “The situation obviously has gone rotten again. We never really resolved it. There’s three huge issues here. Control of the Strait of Hormuz, the whole issue of nuclear, and the whole issue of Israel, Lebanon.”

Sankey Says Crude Oil Isn’t the Real Story

Sankey’s core point: policymakers have levers on crude but almost none on refined product. “Crude oil is not the problem. Nobody’s burning crude oil in their car. The problem is US gasoline in many ways. Yesterday, by contrast, what we saw was a new low in US gasoline inventories,” he said. He notes that Japan has released over a million barrels a day from strategic reserves, and that the Houthis have cut Suez throughput by 50% for the last three years, while China has cut crude imports by as much as 8 million barrels a day and begun exporting products. Governments can shuffle crude around, but they cannot conjure up refining units.

“Refining margins have gone through the top of the range here. It costs between $5 and $10 per barrel to refine for someone like Valero. And we’re at $60,” Sankey said, versus a historical cost of about $15 per barrel. For context, WTI crude itself sat at just $69.60 per barrel on July 6, 2026, down 26.2% over the prior month. Crude is cheap while gasoline stays expensive.

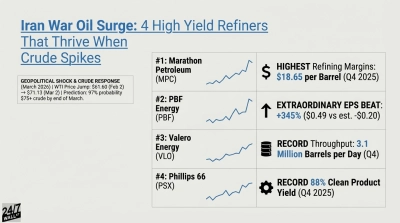

Valero Is the Purest Way to Play the Refining Boom

Valero Energy (NYSE:VLO | VLO Price Prediction) is the cleanest expression of what Sankey describes. In Q1 2026, Valero posted EPS of $4.22 against a $3.16 estimate, with refining segment operating income of $1.81 billion on a $14.90 per barrel refining margin. Gulf Coast distillate margins ran at $27.60 per barrel. The stock has climbed 75.71% year-to-date and 95.27% over the past year to $281.81.

Valero embodies the capacity shrinkage that keeps margins fat. The company is idling its Benicia Refinery in California and evaluating strategic alternatives for its remaining West Coast footprint, a $1.1 billion impairment already booked in FY2025. Every closure tightens the domestic bottleneck Sankey warns about. Wall Street’s consensus price target of $266.94 now sits below the stock’s current price, and shares trade at a forward P/E near 10.

Marathon Petroleum Is Also Benefiting From the Bottleneck

Marathon Petroleum (NYSE:MPC) tells the same story at a bigger scale. Q1 2026 adjusted EPS of $1.65 crushed the $0.75 estimate, refining and marketing adjusted EBITDA hit $1.38 billion, and blended refining margins reached $17.74 per barrel, with the West Coast region at $25.71 per barrel.

Management authorized an incremental $5.0 billion buyback, bringing total authorization to $8.6 billion. Shares have climbed 74.12% year-to-date to $280.38.

The Political Wildcard

Sankey’s warning leans on policy risk. “I would urge the Trump Administration to stay out of this and let the market sort it out. What’s made us so strong here in oil and gas has been the free market. Because once the government starts messing with it, as they have in Europe, it ends up as a disaster.”

Marathon has already flagged tariff uncertainty on crude imports and potential windfall-profit taxes or maximum-refining-margin penalties in California as active risks. With U.S. regular gasoline at $3.78 per gallon, off a 52-week high of $4.50 in May 2026, the political temptation to intervene will not disappear. For investors, Sankey’s message is that the refining trade is real and structural, but the biggest threat may come from Washington rather than the Strait of Hormuz.

Contact [email protected] for any questions or corrections.