Nuclear stocks have been the surprise story of this cycle, and few names carry a bigger swing factor than Oklo. After a violent run to nearly $200 last October and an equally sharp reset this year, the setup is unusually asymmetric. Our proprietary model says the reset went too far.

Our 24/7 Wall St. Price Target for Oklo

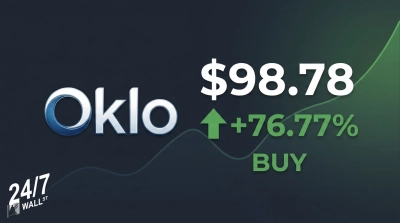

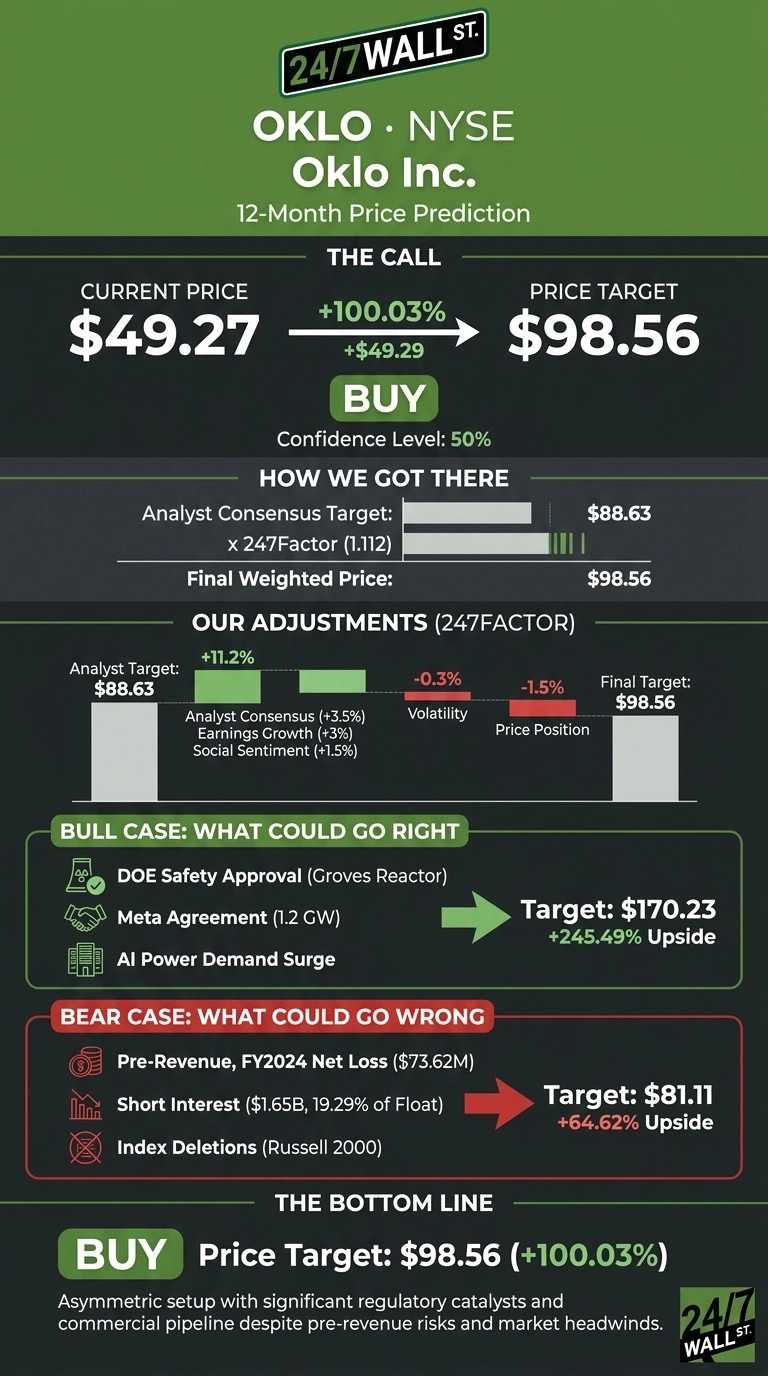

Oklo (NYSE:OKLO | OKLO Price Prediction) trades at $49.27 as of July 9, 2026. Our 24/7 Wall St. price target for Oklo is $98.56 over the next 12 months, implying 100.03% upside from here. The recommendation is buy, with a 50% confidence level. That confidence reads as moderate, appropriate for a pre-revenue name with a wide outcome cone but real regulatory traction.

| Metric | Value |

|---|---|

| Current Price | $49.27 |

| 24/7 Wall St. Price Target | $98.56 |

| Upside | 100.03% |

| Recommendation | BUY |

| Confidence Level | 50% |

From $193 Peak To $49 Reset

Oklo peaked at $193.84 and has since ground down to a 52-week low of $44.88. Shares are down 31.34% year to date and 12.77% in the past month, pressured by the DOE’s $17.5 billion loan program tilting toward large reactors and index deletions from Russell benchmarks in late June.

Yet the operating story improves: the DOE approved the Documented Safety Analysis for the Groves Isotope Test Reactor on July 1, 2026, targeting first criticality this month, and a $67 million institutional bullish options bet drew CNBC coverage on July 9.

Why Bulls See A Breakout Ahead

The bull case is straightforward: Oklo has a 14 GW customer pipeline, a binding 1.2 gigawatt Meta agreement in Ohio, a Centrus Energy HALEU LOI, and the Creative Engineers acquisition that internalizes sodium-cooled reactor expertise.

Aurora at Idaho National Laboratory targets commercial power by late 2027. The bull scenario points to $170.23, a 245.49% return, if AI power demand and NRC velocity hold.

What Could Go Wrong

The bear case is real. Oklo remains pre-revenue with a $73.62 million FY2024 net loss, and Guggenheim initiated coverage in June with a Hold and a $54.06 target, projecting EBITDA positive only by 2030. Short interest sits at $1.65 billion, or 19.29% of float.

Reported losses are inflated by roughly $12.5 million in stock-based compensation, and R&D spend nearly tripled year over year, reflecting deliberate investment in the platform. The bear case still lands at $81.11, above the current quote.

How Oklo Compares To NuScale And Nano Nuclear

The two cleanest US-listed comps are both pre-commercial SMR pure-plays. NuScale Power (NYSE:SMR) is the only SMR with NRC design certification and carries a market cap of roughly $3.1 billion. Its Q1 2026 revenue collapsed 95.8% to just $565,000 as one-time contracts rolled off, and it trades at a Price-to-Book near 3x.

Nano Nuclear Energy (NASDAQ:NNE) is a smaller microreactor developer at a $1 billion market cap with fewer commercial anchors than Oklo. Against that field, Oklo’s $8.3 billion market cap looks premium, but so does its execution: binding hyperscaler agreements, DOE safety approval, and a defined 2027 delivery target. Our $98.56 target looks reasonable relative to peers still searching for their first binding customer.

Oklo Price Prediction 2026-2030

Buy, target $98.56, confidence 50%. The tipping factor is the divergence between price action and operational milestones. The setup fits investors who can tolerate 30% drawdowns while regulatory catalysts play out into 2027. Readers who require earnings visibility inside 12 months will not find it in Oklo, which remains pre-revenue.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $98.56 |

| 2027 | $143.90 |

| 2028 | $210.09 |

| 2029 | $306.73 |

| 2030 | $327.39 |

These projections assume Oklo brings Aurora online near its late-2027 target and converts non-binding LOIs into revenue-generating PPAs. Significant upside or downside could result from NRC licensing pace, HALEU fuel access, and AI data center power demand trajectory.

Contact [email protected] for any questions or corrections.