Jim Cramer says a single AI product decision at Meta Platforms (NASDAQ:META | META Price Prediction) just moved the stock roughly $100 per share, and he is using it as Exhibit A for why big tech is nearly impossible to trim.

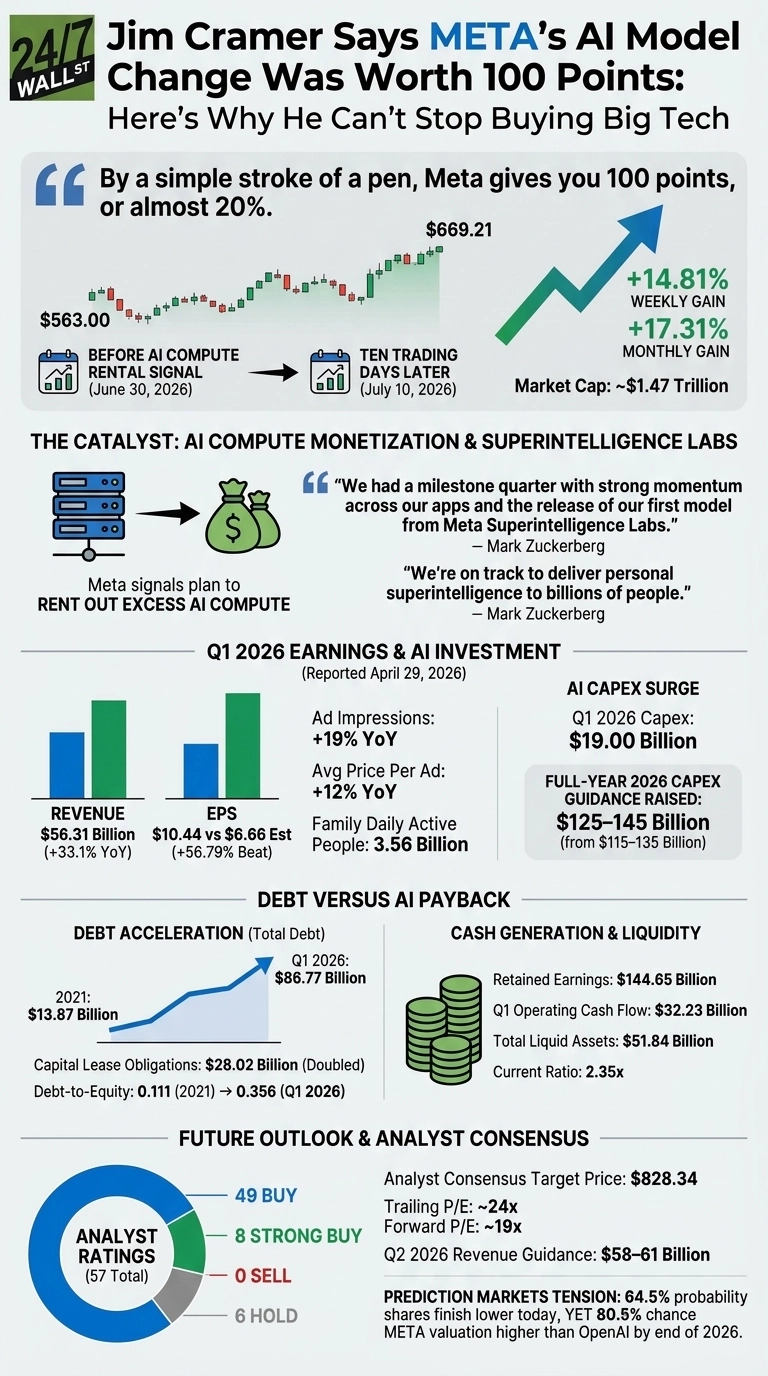

In his Sunday column, Cramer wrote that on the June 30 episode of Mad Money he argued a cloud business announcement from Meta would be “worth an easy 100 points, or $100 per share, for the stock,” back when shares closed at $563. Ten trading days later, they closed at $669.21.

That is a 14.81% move in a single week and a 17.31% move in a month on a company with a $1.7 trillion market cap. Cramer’s takeaway, published on CNBC: “By a simple stroke of a pen, Meta gives you 100 points, or almost 20%.”

The Catalyst Cramer Called

The specific event was Meta signaling it would rent out excess AI compute. Zuckerberg told Bloomberg last week that “the offers that you get for using the compute are so high that it may make sense, in some cases, to rent out or consider those kind of deals instead of your own internal uses.” Meta jumped 5.97% on Friday, July 10, closing at $669.21.

The compute-monetization pivot lands on top of Meta Superintelligence Labs, the new AI research entity Zuckerberg introduced on the Q1 2026 call. He described it as a “milestone quarter” that included “the release of our first model from Meta Superintelligence Labs” and reiterated the goal of “personal superintelligence to billions of people.”

The Numbers Under the Rally

Meta’s Q1 2026 report, filed with the SEC on April 29, showed revenue of $56.31 billion, up 33.08% year over year, and EPS of $10.44 against a $6.66 estimate. The advertising engine grew 33%, with ad impressions +19% and average price per ad +12%. Family daily active people reached 3.56 billion.

The catch: capex. Meta raised full-year 2026 capital expenditure guidance to $125–145 billion, up from a prior $115–135 billion range. Q1 capex alone hit $19 billion. Cramer’s argument is that the compute-rental pivot changes how investors should think about that spend, because dormant infrastructure suddenly becomes a revenue line rather than a capex sinkhole.

Debt Versus AI Payback

The bear case Cramer is answering is leverage. Total debt has climbed from $13.87 billion at year-end 2021 to $86.77 billion at the end of Q1 2026. Capital lease obligations tied to AI data centers doubled to $28.02 billion. Debt-to-equity has moved from 0.111 to 0.356.

The offset is cash generation. Retained earnings reached $144.65 billion. Operating cash flow in Q1 was $32.23 billion. Liquid assets total $51.84 billion, and the current ratio sits at 2.35x.

Investors sorting the AI winners from the also-rans may find useful context in our 7 Stocks Powering the AI Boom (That Aren’t Chipmakers) report, which frames why hyperscalers with in-house monetization paths get valued differently than pure infrastructure plays.

What to Watch Next

At 24x trailing earnings and 19x forward, Meta is not cheap on a growth-adjusted basis, but the analyst consensus target of $828.34 implies room above current levels, backed by 49 Buy and 8 Strong Buy ratings against zero Sell calls. Q2 revenue guidance is $58–61 billion.

Prediction markets are notably split on tempo. Polymarket traders assign a 64.5% probability that shares finish today lower, yet give Meta an 80.5% chance of ending 2026 with a higher valuation than OpenAI. That is the exact tension Cramer’s column captures: near-term digestion is possible, but the AI optionality is the reason he says these names are so hard to leave.

Contact [email protected] for any questions or corrections.