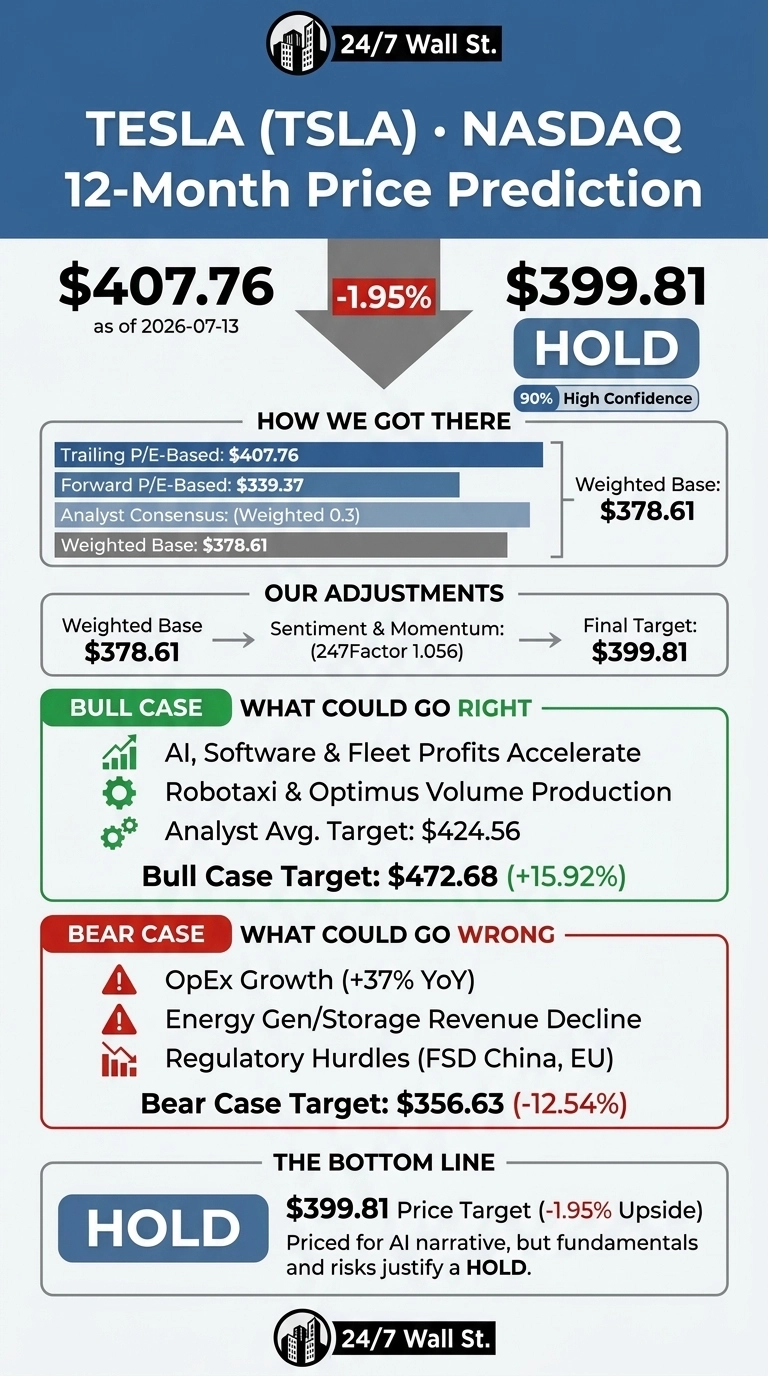

The verdict on Tesla is closer to a coin flip than the stock’s history of extreme moves suggests. Our 24/7 Wall St. price target for Tesla (NASDAQ:TSLA | TSLA Price Prediction) is $399.81, roughly 1.95% below the current $407.76 quote. That fractional gap, combined with a proprietary confidence score of 90%, drives our hold rating. Tesla is priced for the AI narrative to keep working.

| Metric | Value |

|---|---|

| Current Price | $407.76 |

| 24/7 Wall St. Price Target | $399.81 |

| Upside/Downside | -1.95% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our price target sits below current levels, and Tesla is arguably the most divisive large-cap in the market. Real value could come from faster Robotaxi rollout across seven US metros or Optimus reaching volume production ahead of schedule at the 1 million robots per year Fremont line. Consider our target one datapoint among many.

A Choppy Year to Date Masks a Strong Rebound

Tesla shares are up 3.64% over the past week and 6.86% over the past month, yet down 9.33% year to date after starting 2026 at $449.72. Over 12 months, the stock has gained 31.59%. Current price sits 15% below the 52-week high of $498.83.

Q1 FY26, reported April 22, marked a genuine inflection. Revenue of $22.39 billion grew 15.8% year over year, non-GAAP EPS of $0.41 beat by 14.14% beat expectations, and GAAP operating income surged 136% to $941 million. FSD active subscriptions hit 1.28 million, up 51%, and unsupervised Robotaxi rides launched in Dallas and Houston during the quarter.

Why Bulls See a Breakout Ahead

The bull case rests on Tesla as a physical AI company. Cybercab, Tesla Semi, and Megapack 3 are all on schedule for volume production starting in 2026, with an acceleration of AI, software, and fleet-based profits to follow. Services and Other revenue grew 42% year over year to $3.75 billion in Q1, powered by FSD monetization.

Analyst consensus target sits at $424.56, and our bull-case scenario models a one-year path to $472.68, a 15.92% return. If Optimus hits its 10 million robots per year Gen 2 line target in Texas, that ceiling likely gives way.

What Could Go Wrong

Tesla trades at 404x trailing earnings and a 4% net margin. Operating expenses grew 37% year over year in Q1 on AI R&D and stock-based compensation. Global inventory rose to 27 days of supply from 22, and Energy revenue declined 12% year over year. Prediction markets model an AI-implied downside of 19.11%, and Polymarket puts odds of Optimus shipping by year-end at 14%.

Bulls counter that OpEx growth is investment, not deterioration, and Q1’s FCF of $1.44 billion (+117%) supports that view. Our bear-case scenario points to $356.63, a 12.54% decline.

How Tesla Compares to Rivian and General Motors

Two US-listed peers frame the valuation debate. Rivian (NASDAQ:RIVN) is the pure-play EV growth comparable, with R2 mass-market launch underway and a Volkswagen software partnership. Rivian’s Q1 FY26 revenue of $1.38 billion grew 11.4% carries a market cap of $25.2 billion, but net margin of negative 68% makes Tesla’s profitability formidable by contrast.

General Motors (NYSE:GM) is the valuation counterweight: P/E of 26x, 2026 EPS guidance of $11.50 to $13.50, and EV segment realignment underway. On classical metrics Tesla screens rich against GM, which is why our target does not rerate the multiple lower. The bull thesis must carry the extra weight, and the peer set makes our 24/7 Wall St. price target reasonable rather than aggressive.

Hold, but Keep Your Finger on the Trigger

The 24/7 Wall St. price target of $399.81 with 90% confidence supports a hold. The tipping factor is the gap between fundamentals and option value on Robotaxi, Optimus, and Cybercab.

The bull trigger to watch is Robotaxi expanding to all seven planned metros with clean safety data by year-end, or Optimus entering paid customer deployment. A red flag would be Q2 FY26 showing further OpEx acceleration without matching auto gross margin expansion. For now, hold.

Extending the 24/7 Wall St. price target model outward, here is where Tesla could trade assuming current growth trajectories and market conditions hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $399.81 |

| 2027 | $400.31 |

| 2028 | $411.11 |

| 2029 | $401.88 |

| 2030 | $429.08 |

These projections assume Tesla continues executing its AI, software, and autonomy roadmap. Meaningful upside or downside could result from Optimus commercialization timing, FSD regulatory approvals in China and the EU, or mega-cap growth multiple compression.

Contact [email protected] for any questions or corrections.