SpaceX (NASDAQ:SPCX | SPCX Price Prediction) has given back its post-IPO gains, but the round trip toward the offering price is exactly why I’m sharpening my pencil. The stock priced at $135 on June 12, 2026, popped to an intraday peak of $225.64, and now trades near where it started.

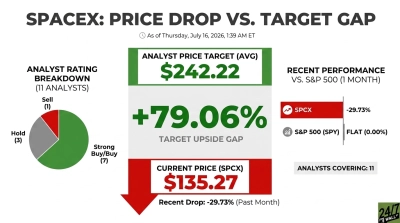

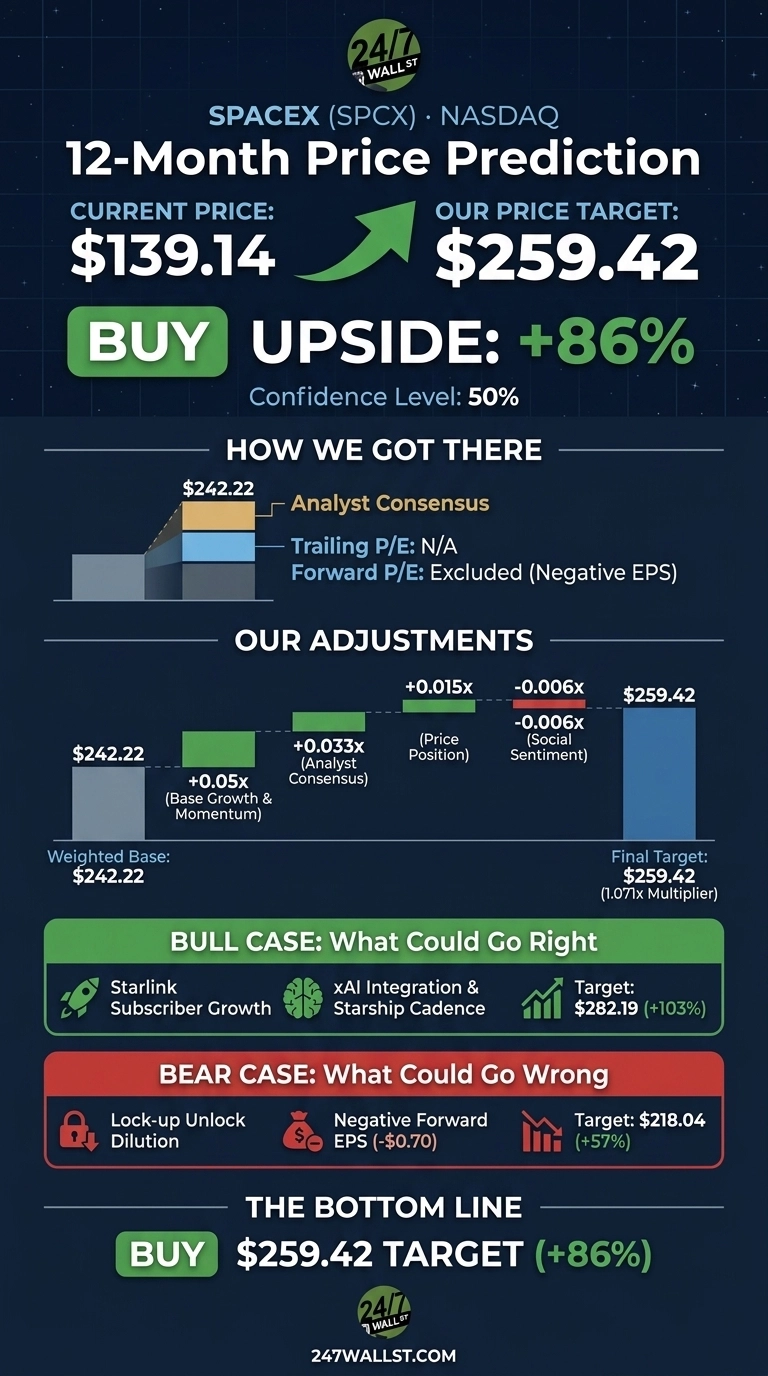

Our 24/7 Wall St. price target for SpaceX is $259.42, implying roughly 86% upside over the next 12 months. The model’s rating carries moderate confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $139.14 |

| 24/7 Wall St. Price Target | $259.42 |

| Upside | 86.4% |

| Recommendation | BUY |

| Confidence Level | 50% |

From $225 to $139 in Four Weeks

SPCX has fallen 13.55% in the past month and 13.27% in the past week, closing Monday at $139.14 after a 4.24% single-day slide. That puts the stock near the $135 IPO price and roughly 38% below its intraday high.

The Reddit thread “SPCX first major unlock is bigger than the entire IPO float” captures the near-term overhang. Retail is also focused on Japan’s successful rocket landing, which challenged the “competition is years away” thesis. SpaceX pulled in $18.7 billion in 2025 revenue, and the $75 billion raise at a $1.75 trillion valuation left the float thin.

The Case for $282+

Bulls have plenty to work with. Starlink is scaling toward millions of customers across 164 countries from a constellation of roughly 9,600 satellites. The xAI acquisition in early 2026 layered a frontier AI model onto the platform, giving SPCX a seat in the hyperscaler conversation. Jim Cramer noted the combined entity “could be seeking a valuation of over $2 trillion.”

Our bull case points to $282.19 over 12 months, driven by Starlink subscriber growth, Starship cadence, and monetization of satellite-to-mobile coverage across roughly 30 countries. Analyst consensus alone at $242.22 implies 74% upside.

What Could Go Wrong

The biggest near-term worry is dilution. Reddit flagged that the first major lockup unlock is “bigger than the entire IPO float,”. Forward EPS of -$0.70 means the market is paying up for a business still spending more than it earns.

Cramer argued it is “very difficult to justify giving SpaceX a $2 trillion valuation” for a money-losing company. Our bear case pegs downside at $218.04. Bulls counter that those losses reflect heavy capex on Starship, xAI compute, and satellite manufacturing, all of which underpin the multi-year growth story.

How SpaceX Compares to Rocket Lab and AST SpaceMobile

Rocket Lab (NASDAQ:RKLB) is the cleanest US-listed launch peer. Rocket Lab posted Q1 2026 revenue of $200.35 million (up 63.5% year over year) with backlog at $2.20 billion and a market cap near $44 billion. The stock trades at roughly 55x trailing sales, while SpaceX at $259 would sit closer to 19x its $18.7 billion 2025 revenue. Our target looks conservative on a price-to-sales basis.

AST SpaceMobile (NASDAQ:ASTS) is the direct-to-device satellite counterpoint to Starlink. ASTS carries a $21 billion market cap on 2026 revenue guidance of $150 million to $200 million, a triple-digit sales multiple for a pre-commercial network. Starlink already generates a large share of SPCX’s revenue at scale, framing the 24/7 Wall St. price target as reasonable.

Where the Setup Gets Interesting: $135

My line in the sand is the IPO price. At $135, buyers get in flat to the largest institutional book of 2026 with an analyst target implying 74% upside and a 24/7 Wall St. price target of $259.42 pointing higher.

The setup looks constructive if SPCX holds the IPO floor through the lockup window. It looks risky if the stock breaks $130 on heavy volume, signaling the unlock is overwhelming demand. Confidence is moderate at 50%, but the risk/reward at these levels is finally interesting.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $182 |

| 2027 | $256 |

| 2028 | $359 |

| 2029 | $504 |

| 2030 | $708 |

These projections assume SpaceX continues scaling Starlink subscribers, executes on Starship cadence, and monetizes xAI. Significant upside or downside could result from lockup dynamics, a Starship setback, or step-change in launch competition.

Contact [email protected] for any questions or corrections.